DISCLAIMER: The person is speaking in a personal capacity and does not represent the institution that employs them.

The perfect heist you’ve never heard about: « Repo » derivatives and bankruptcy law

Summary:

– Changes to bankruptcy law relating to financial transactions known as « repos » (repurchase agreements) have created a « hold-up » phenomenon: even creditors who in principle enjoy the highest seniority are now vulnerable to default risk!

– Unnoticed by most non-institutional investors, these developments made the financial system more vulnerable before 2008 and also increased contagion in the early stages of the crisis.

– At the very least, any reform of the repo market must both clarify the ownership rights of these derivatives and, above all, introduce greater transparency in their use.

« The lack of transparency in the repo and collateralized loan markets makes it difficult to identify ownership rights (who owns what?) and monitor risk concentration, as well as to identify counterparties (who is exposed to whom?). »

European Commission, September 4, 2013.

The evolution of the legal status of repurchase agreements, or « repo » transactions, which went unnoticed, created a « hold-up » phenomenon. On the one hand, creditors who in principle enjoy the highest degree of seniority unwittingly saw their vulnerability increase in the event of bankruptcy. On the other hand, the super-guarantee offered by Repo to the detriment of creditors and its flexibility of use in accounting terms generated greater instability in 2008, as exemplified by its use by Lehman Brothers, with both greater vulnerability of the financial system and a strengthening of contagion phenomena. As a result, the development of Repo’s use has been detrimental not only to creditors (the « jump in the queue » phenomenon) in the event of bankruptcy, but also indirectly to all market participants via a second-round effect. The perfect « hold-up. »

Under these circumstances, the lack of transparency regarding ownership rights for repo-type derivatives prompted the European Commission to initiate a reform of ownership rights for collateralized assets after 2014.

What is a Repo?

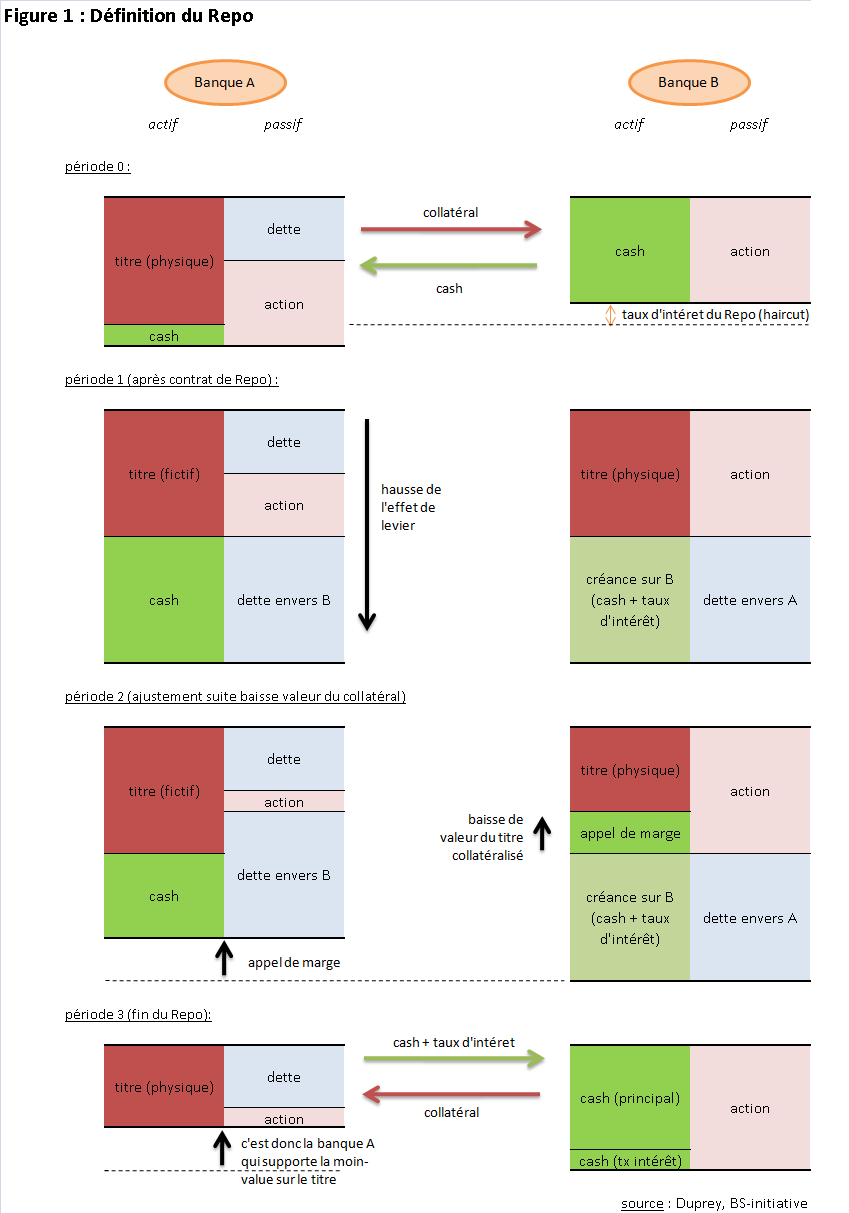

A repo (repurchase agreement) between two parties is a contract involving the sale of an asset followed by its repurchase at the end of the transaction at a predetermined price. Such a contract can be broken down into three stages (see Figure 1):

1- sale(see Figure 1, period 0 to 1): institution A transfers a security to institution B in order to obtain the corresponding value in cash, less a haircut; this rate reflects both (i) the interest rate corresponding to the provision of liquidity and (ii) the risk premium associated with the possible fluctuation in the price of the asset transferred in exchange and thus serving as collateral;

2- readjustment(see Figure 1, period 2): depending on changes in the market value of the asset now held by institution B, the terms of the contract are reassessed to ensure that the value of the exchanged asset is still greater than the amount of the initial loan; margin calls are made, for example, through additional cash transfers from A to B;

3- Repurchase(see Figure 1, period 3): at the end of the contract, institution A must repay its debt in cash to institution B, which in exchange must return the associated assets, the price having been continuously readjusted in line with margin calls.

The main advantage for the cash borrower/securities seller is the temporary transfer (typically a few days/weeks) of cash previously unused by B. Furthermore, the cash lender/securities buyer (bank B) does not become illiquid: the collateral thus received can always be resold in exchange for cash in another Repo contract, with Bank B responsible for returning collateral that is equivalent in all respects at the end of the Repo with Bank A.

The legal definition of a repo is problematic: is it a collateralized loan or a transfer of ownership?

The difficulty associated with Repo stems from its hybrid nature; on the one hand, such a transaction is similar to a collateralized loan, as the amount loaned must be less than the value of the collateral, which is adjusted during the transaction. On the other hand, a repo can be considered a sale because the buyer controls the collateral: there is a transfer of ownership, as the buyer can, for example, resell the collateral (« rehypothecation »), its only obligation being to replace the collateral with a similar asset once the repo contract has expired.

From an accounting perspective, there is no transfer of ownership: the repo remains a collateralized loan.

GAAP (US) accounting standards stipulate that the transfer of a financial asset is only considered a sale if control of the asset has been fully transferred [1]. However, the repo does not provide for a complete transfer of ownership of the asset, since the cash borrower/securities seller (bank A) is obligated to repurchase the transferred asset at the end of the contract. Even if the security initially used as collateral has been resold by the cash lender/security buyer (bank B), the fact of giving the liquidity borrower/security seller (bank A) another security, equivalent in all respects, is still not considered a sale for accounting purposes [2].Thus, from an accounting perspective, the collateral in a repo transaction remains on the balance sheet of the cash borrower/seller of the security (bank A), as do the cash received in exchange for the sale of the security and the repurchase obligation: therefore, the repo has the effect of increasing the leverage of the borrowing/selling institution (bank A) (see Figure 1, period 1).

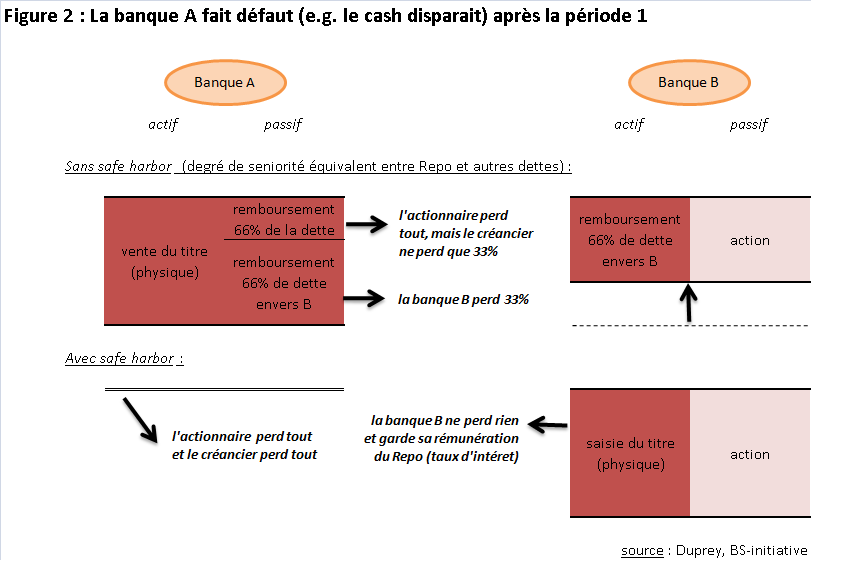

However, in the event of bankruptcy, the repo is now considered a sale, i.e., excluded from bankruptcy law: the « safe harbor » privilege.

Initially, repos in the US were considered more like collateralized loans. As such, repos were subject to counterparty risk, meaning that they could not be repaid if the borrower defaulted. More specifically, bankruptcy law thus consists of an orderly resolution of debts according to their degree of seniority, thereby avoiding liquidation on a « first come, first served » basis, which is subject to the phenomenon of liquidity runs. Therefore, in the best-case scenario, the lender in a repo contract would have had to wait for the bankruptcy to be resolved before being repaid.

However, the assets pledged by the lender via the repo, which are now illiquid in the event of bankruptcy, may lose some of their value without the possibility of compensation: the bankrupt institution can no longer meet margin calls. Repos therefore become much riskier, which effectively limits their use by financial intermediaries as a source of additional liquidity.

Since the 1980s, US (and European) legislation has gradually evolved to ultimately consider Repo as more akin to a sale (Garbade, 2006; Perotti, 2012). This has been achieved through the extension of « safe harbor » status to Repo.

The safe harbor principle allows a party whose financial transaction is secured to immediately dispose of the collateral in the event of counterparty default: if institution A goes bankrupt, B will have definitive and immediate access to the collateral (and any margin calls), i.e., well before other creditors (even the most senior ones) are repaid (see Figure 2).

Repos create a transfer of wealth to the detriment of uninformed lenders.

The exemption of Repo from traditional bankruptcy law rules potentially generates a transfer of wealth to the detriment of small, uninformed lenders by creating a distortion in the financial balance of other claims. In fact, the assets used as collateral for Repo transactions still appeared on the balance sheet of the financial institution that used them, with the equivalent debt appearing on the liabilities side (see Figure 1, period 1). However, a senior creditor who has invested in this institution has only very limited (or even no) information about the relative size of Repo transactions on the balance sheet: such a creditor, believing that they have sufficient seniority, could legitimately expect their claim to be repaid in the event of bankruptcy(see Figure 2, without safe harbor), whereas the significant presence of assets used in a repo transaction implicitly reduces the value of their claim (see Figure 2, with safe harbor); only assets not used for Repo will still appear on the institution’s balance sheet in the event of bankruptcy, which reduces the expected repayment to creditors, even senior ones.

The super-seniority of Repo as a source of instability during the 2008 crisis

The introduction of the « safe harbor » privilege has a negative impact both ex-ante on loan management and ex-post on the propagation of shocks between financial institutions.

On the one hand, the super-seniority of Repo provides full insurance against the risk of counterparty default; like deposit insurance, such a mechanism removes any incentive to control the use of funds by the borrowing institution. As a result, the US mortgage market was able to develop without consideration for credit risk: subprime loans, which are by definition illiquid with maturities of several years, were converted into financial products (mortgage-backed securities) through securitization and then used as collateral in repo transactions to generate sufficient liquidity to finance new loans. The fragility of the financial system thus increased without the increased risk being factored into prices.

Furthermore, if the risk materialized, this accumulation of vulnerabilities would weaken the entire system. Lehmann Brothers had rapidly increased its investments in mortgage securities through repo financing, especially since the bank had an incentive to refinance itself in the very short term through repo in the hope of breaking the deadlock rather than seeking protection under bankruptcy law (Duffie and Skeel, 2012). Although the repo counterparties were not directly affected by Lehman’s bankruptcy thanks to the exemption of such transactions from traditional bankruptcy law, these same counterparties rushed to resell the securities they had acquired, which were backed by real estate loans whose value was rapidly declining. The massive short positions had a mechanical downward effect on the value of the securities sold, accelerating the collapse of the US mortgage securities market, which affected all market participants.

Enhancing transparency in the use of repos to prevent another « hold-up«

As a result, the « safe harbor » principle is extended not only to the detriment of holders of unsecured debt securities, but also indirectly to the detriment of all market participants via a possible second-round effect in the event of bankruptcy.

In conclusion, regulation of the repo market must, at a minimum, involve greater transparency in its use by financial institutions sothat each investor is aware of the quantity of securities used as collateral for repos (Perotti, 2011), or even centralization of Repo-type derivative transactions (Tuckman, 2010), so that market discipline can be enforced by uninsured or less well-protected creditors than the parties to the Repo. The European Commission (2013) therefore wishes to initiate, after 2014, a reform aimed at clarifying the property rights associated with Repo-type transactions in order to overcome the lack of transparency of these derivatives.

[1] Paragraph 9 of Financial Accounting Standard (FAS) Statement 140

“A transfer of financial assets in which the transferor surrenders control over those financial assets shall be accounted for as a sale […]. The transferor has surrendered control over transferred assets if and only if all of the following conditions are met: […] The transferor does not maintain effective control over the transferred assets through either an agreement that both entitles and obligates the transferor to repurchase or redeem them before their maturity. ”

[2] Paragraph 100 of Financial Accounting Standard (FAS) Statement 140

“As with securities lending transactions, under many agreements to repurchase transferred assets before their maturity the transferor maintains effective control over those assets. Repurchase agreements that do not meet all the criteria in paragraph 9 shall be treated as secured borrowings. […] Other contracts under which the securities to be repurchased need not be the same as the securities sold, qualify as borrowings if the return of substantially the same securities as those concurrently transferred is assured.”

References:

– Duffie, D. and Skeel, D. (2012). A Dialogue on the Costs and Benefits of Automatic Stays for Derivatives and Repurchase Agreements. Stanford University Working Paper No. 108.

– Garbade, K. (2006). The Evolution of Repo Contracting Conventions, Federal Reserve Bank of NewYork Economic Policy Review, 12(1).

– Perotti, E. (2011). Targeting the Systemic Effect of Bankruptcy Exceptions, Journal of International Banking and Financial Law.

– Perotti, E. (2012). The roots of shadow banking. EBA working paper.

– Tuckman, Bruce (2010). Amending Safe Harbors to Reduce Systemic Risk in OTC Derivatives Markets, Centre for Financial Stability, New York.

– Chip, W. (2002). Are Repos really loans? Deloitte& Touche, Tax notes.

– European Commission (2013). Shadow banking – addressing new sources of risk in the financial sector, September 4.

– Epstein, B.J. (2010). When window dressing becomes fraud: Repo 105 was much more than window dressing Repo 101.