News: Tomorrow, British citizens will have a choice between two options for their future in Europe: remain in or leave the European Union. According to recent estimates by Ipsos Mori from June 11-14, 2016, Brexit is ahead in the polls, although 13% of those surveyed remain undecided. Such an event would have negative economic consequences for the United Kingdom and would particularly fuel sovereign risk, with the risk of seeing public debt « explode. »

Deterioration of public finances

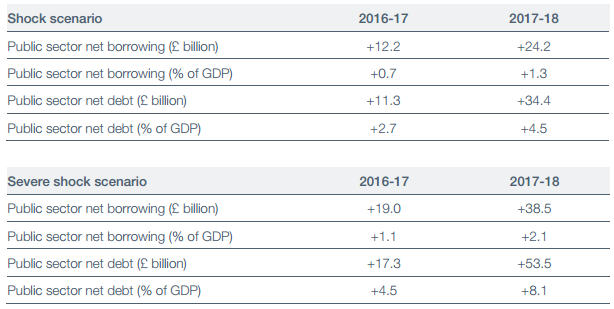

There is a consensus among the various economic forecasting institutes that, in the event of Brexit, growth in the United Kingdom would be revised downwards. A contraction in GDP growth and a slowdown in economic activity would result in a decrease in tax revenues and even an increase in public spending (to potentially benefit from a stimulus effect). The combination of these two events would inevitably worsen the public balance, whose deficit already reached 4.4% of GDP in 2015.

Summary table of the impact of Brexit on public finances

Source: UK Treasury

The United Kingdom currently enjoys some of the highest ratings from credit rating agencies (triple A from S&P, like Germany, Aa1 from Moody’s, and AA+ from Fitch), but a deterioration in public finances could prompt them to quickly revise their ratings[1]. At this stage, even though public debt represents 89% of GDP, there would be no major risk to British public finances. However, a series and combination of events, which are all likely, would turn this situation into a downward spiral.

Depreciation of the pound and rise in inflation

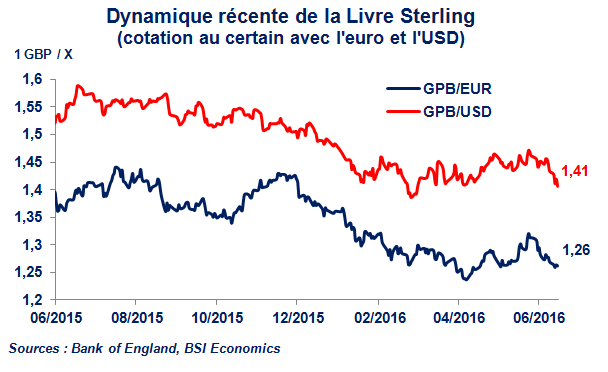

Capital outflows, caused by doubts about the risk of Brexit, have already begun to put downward pressure on the value of the pound sterling (GBP) (see chart below). In the event of Brexit, these capital outflows could intensify further, causing a sharp depreciation (more than 12% before the end of 2016, according to the UK Treasury).

This depreciation is likely to lead to:

· A rise in inflation, via a loss of household purchasing power, higher import prices, and upward expectations. CPI inflation was only 0.3% in May 2016, but it would rise by an additional 2.3 to 2.7 percentage points in 2016 alone, according to various UK Treasury scenarios.

· A negative currency effect for investors holding financial assets denominated in GBP. Arbitrage in favor of financial assets with the same credit quality denominated in other currencies (which have appreciated against the GBP over the same period) could then occur. This is a significant risk given that 30% of UK public debt is held by non-residents.

Monetary policy transmission and term premium

The increase in sovereign risk resulting from a deterioration in public finances would likely fuel a rise in sovereign bond yields, as the estimate of public debt sustainability would be revised in line with the evolution of risks weighing on public finances. Currently, these yields are fairly low (0.38% at 12 months, 0.48% at 3 years, 1.14% at 10 years) and have not increased in recent months[2]. Even if the Bank of England (BoE) maintains low interest rates in the short term to provide banks and the economy with liquidity in the event of Brexit, rising inflation and the depreciation of the exchange rate could cause it to face conflicts of interest regarding its priority monetary policy objectives:

· If key benchmark interest rates remain low, the transmission of this monetary policy should favor low bond yields for UK sovereign bonds;

· However, low benchmark rates would not discourage and/or limit capital flight.

Therefore, a rise in inflation combined with a negative exchange rate effect would tend to increase the term premium[3] on sovereign bonds. An increase in bond yields could then be observed, either due to a rise in the term premium or due to poor transmission of monetary policy to sovereign bond interest rates as a whole. However, if sovereign bond yields rise, their prices automatically fall. This fall in prices remains a likely scenario, and potential capital losses would then be recorded on UK sovereign bonds.

A stress scenario on the bond market?

If this situation is anticipated by the financial markets, a tactical (or even strategic) reallocation of bond portfolios could take place, to the detriment of UK sovereign bonds and to the benefit of European sovereign bonds of the same or similar credit quality (Germany, Switzerland, or France).

Such a scenario would trigger sales of UK bonds and thus a self-fulfilling decline in their price (net short positions). Under such conditions, a negative spiral would be created: sale of sovereign bonds – fall in prices/rise in yields – increase in debt servicing costs – rise in sovereign risk – sale of sovereign bonds, etc. Once this spiral is in place, it becomes very difficult to stop, and public debt can quickly balloon and the rating of public debt by agencies can deteriorate.

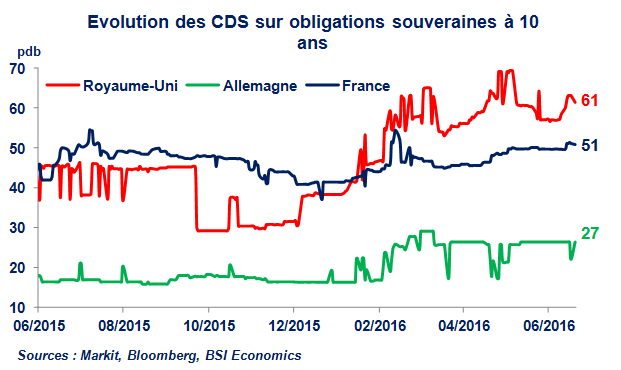

Since the beginning of 2016, credit default swap( CDS) premiums on UK sovereign bonds have risen across all maturities (see chart above). The levels reached remain reasonable, but the dynamics of CDSs in the run-up to the vote clearly reflect the markets’ growing concern about Brexit. The markets may already have priced in Brexit by incorporating it into CDS premiums. In the event of Brexit, sovereign CDSs would be a good proxy for assessing the likelihood of stress on the bond market, generating the spiral described above.

Conclusion

In the event of Brexit, this scenario would probably be the most risky for the British authorities. However, it is not considered a central scenario. But a public debt crisis cannot be ruled out. It is currently too early to comment on the feasibility of such a scenario, given the uncertainty that still surrounds the outcome of the June 23 referendum. More than ever, Bremain appears to be the best way to avoid this worst-case scenario.

[1] S&P has already planned to change its rating to negative in the event of Brexit.

[2] They have even fallen as the probability of Brexit has increased.

[3] A premium that compensates investors who agree to hold long-term securities rather than renewing investments in short-term securities.

[4] In a scenario where inflation rises faster than anticipated by the UK Treasury, we could also see a decline in the real yield on these bonds.

[5] CDSs are derivatives that take the form of insurance contracts. By paying premiums to the CDS issuer, the CDS buyer benefits from financial protection in the event of a loss linked to a potential decline in the value of the underlying asset.