Summary:

• The high interest rates in Brazil, which have been among the highest in emerging countries for 15 years, are the result of a political decision made as part of the Real Plan to attract foreign capital to support the currency while combating rampant inflation.

• These rates have had three consequences: i) economically, a lack of financing for the economy; ii) fiscally, an increase in the debt burden, which is indexed to the base rate; and iii) monetarily, weak transmission of monetary policy given the predominance of administered-rate loans;

• Recently, thanks to low inflation, real rates have begun to fall, but the sustainability of this decline is questionable.

Faced with falling inflation, the Brazilian Central Bank (BCB) has begun a cycle of monetary policy easing. Inflation in Brazil has fallen to its lowest level in more than 20 years, at 2.5%, and has even fallen below the Central Bank’s target. Several sectors are even experiencing deflation, so the BCB has reduced the Selic rate, or base rate, from 14.25% to 7.5%, and it will likely fall to 7% in the near future. This policy accompanies the country’s fiscal consolidation. In this context, the question arises as to the sustainability of the decline in real interest rates, which currently stand at around 5% compared with 7% historically. The ex-ante real interest rate for 2018 is forecast to be around 3%, while the natural rate is expected to be around 5%.

In fact, the historically high level of real interest rates in Brazil is primarily the result of political will, but has gradually become structural. Without correcting the various consequences of this policy, real interest rates can only remain at this level through less support for the real and medium-term depreciation.

1. Interest rates: a structural issue

• Historically high interest rates to support the real and then combat inflation

On January 1, 1994, Brazilians woke up to a new currency: the real. After a decade of hyperinflation, which reached 2,500% in 1993, and six ill-conceived intervention plans, priority was given to fighting inflation and increasing the attractiveness of foreign capital to guarantee the monetary policy of the exchange rate regime. The BCB thus sought to avoid further sharp devaluations of the currency, following episodes of severe real depreciation, fiscal fragility, and inflation.

In this sense, in order to attract foreign capital and strengthen a currency born in a context of severely damaged confidence, the BCB’s base rate (Selic) was first raised to 41.2% per annum to give investors record returns, particularly with the real-USD parity initially set at 1 to 1.

In the context of currency crises in emerging countries, ranging from the Mexican currency crisis in early 1995 to the Russian sovereign default in 1998, the Selic was maintained at an average of around 34% per annum to support the currency. At the same time, the BCB decided to change its exchange rate policy, allowing a partially floating exchange rate.

From June 1999, with the adoption of the inflation targeting monetary regime, the short-term interest rate—or the Brazilian Central Bank’s key interest rate—became the crucial variable in the model for keeping inflation within the set targets.

• A monetary policy disconnected from the real economy since the 2000s

Over the last 15 years, the average Selic rate has stood at 13.5%, an excessive threshold that does not reflect the real risks surrounding Brazil’s economic and political situation.

Brazil has one of the highest real interest rates in the world, with an average real rate of 6.8% since 2002, on a par with countries in civil war or at risk of default. However, the risk associated with Brazil does not justify such a high real interest rate. Apart from the level of sovereign risk, as approximated by the level of CDSs, the low risks associated with foreign exchange or external debt cannot explain such high interest rates. In addition, CDSs have resumed their downward trajectory that began in 2002, which was temporarily halted in 2015-2016 due to impeachment. Furthermore, Brazil has very comfortable foreign exchange reserves (USD 363 billion at the end of 2016, or almost 30 months of imports), a relatively moderate level of public debt (73% of GDP in mid-2017), and low external debt (15%), which cannot explain such high real interest rates.

Overall, the BCB’s interest rate monetary policy has gradually become « out of touch » for several reasons.

First, this disconnect from monetary policy led to overreactions on the part of the BCB in order to combat inflation. Indeed, inflation trends led to sharp and rapid movements in the Selic rate, except during the gradual monetary easing of 2005. The Selic rate rose from 10% at the beginning of 2014 to 14.25% in September 2016, even though GDP contracted by nearly 8% and the 4-point rise in inflation over one year was mainly the result of a recalibration of administered prices in early 2015. This monetary overreaction, which is still ongoing, has led to a climate of high uncertainty and market volatility, undermining the credibility of the central bank.

Alongside the overreactions in the fight against inflation, monetary policy has gradually become disconnected from the federal government’s fiscal policy, even though more than 65% of the debt burden is indexed to the base rate. Highly pro-cyclical tax revenues (no VAT in Brazil), buoyed by a decade of strong growth (rising commodity prices), have made it possible to free the country from a costly debt burden.

2. Profound consequences for the economy’s financing model

• A domestic investment shortfall

Although the real was created on the basis of a high base rate, this had adverse effects on the financing of the economy.

In addition, Brazil sought to attract capital to compensate for low domestic savings, largely due to fears of hyperinflation and a traditionally short-term use of credit, which led to a structural current account deficit. While domestic savings remained low, Brazil’s dependence on foreign investment grew stronger and stronger, resulting in high levels of debt. In fact, since the 2007 crisis, Brazil has remained the second largest recipient of Foreign Direct Investment (FDI) among emerging economies, behind China and Hong Kong, according to UNCTAD. Overall, FDI has largely made up for this current account deficit. In addition, portfolio investment flows remained high until 2015—a year of political and economic crisis—and accounted for about 2% of GDP, compared with 4% for FDI.

In terms of domestic investment, the low rate of productive investment by companies in recent years (GFCF represented only 15% of GDP in 2017, which is low compared to the 25% average among BRICS countries) is closely linked to the extremely high interest rates charged by commercial banks, as an indirect consequence of the Central Bank’s interest rate policy. The interest rates charged by commercial banks are sometimes six times higher than the key interest rate, a situation that makes most investment projects unviable. Banks therefore focus both on short-term loans (the average maturity of loans in Brazil is just over one year) and on Tesouro bonds. As a result, private sector credit in Brazil represents on average only 26% of GDP, compared to 72% in OECD countries in 2016.

Commercial banks therefore play a marginal role in financing investment and mainly finance the government deficit by purchasing highly lucrative Tesouro bonds. This situation has prompted companies to turn to the National Bank for Economic and Social Development (BNDES) in particular to benefit from subsidized interest rates. The public sector now accounts for the majority of outstanding loans, while the refinancing spread (Selic minus subsidized rate) is borne by the federal budget.

The recent monetary easing policy (Selic lowered by 675 basis points since October 2016) pursued by the BCB, while reducing the real rate in the short term, has had little impact on the rates applied, reflecting a monetary policy that is unable to respond to the essential revival of investment.

• Excluding the public sector, credit is falling in Brazil

Given the above factors, private commercial banks are sticking to short-term credit, offering very high interest rates on private bank loans. This generous margin, compared to other sectors of activity in Brazil, can be explained in part by the concentration of banks and the lack of competition among private banking players in Brazil. On the other hand, the financial system remains robust.

To fill this gap, long-term financing remains essentially the preserve of the BNDES, at subsidized rates: the share of subsidized credit in GDP has more than doubled and now accounts for half of assets, in contrast to the private sector, which has been stagnating since 2007 (see Figure 1).

The BNDES finances companies, industrial policies, and infrastructure (states, municipalities, among others). It provides medium/long-term loans at a TJLP rate—now TLP as of 2018—which is lower than the Selic rate. The cost of refinancing is therefore borne by the federal government (Tesouro).

Figure 1- Share of credit in GDP, in %, by type of credit

Given this highly asymmetrical method of financing the economy, Brazil’s budgetary situation no longer allows it to grant resources to the BNDES. The long-term financing of investments could be called into question in the absence of commercial banks.

• Long-term budgetary consequences

The budgetary consequences are likely to be long-lasting for the economy and thus prevent a fall in real interest rates, given the dynamics of public debt. More than two-thirds of the cost of Brazil’s debt (6.5% of GDP in 2016) is indexed—directly or indirectly—to the Selic rate. This burden was artificially masked by strong growth driven by commodities (2002-2013), which stabilized the level of gross public debt to GDP at between 50% and 60%. Moreover, since the onset of the recession, this aggregate has risen from 53.3% to 73% of GDP in mid-2017, and will remain on a sustained upward trend. Recently, the increase in risk in Brazil since 2014, due to the political and institutional crisis, the « Lava Jato » scandal and the economic recession, has prevented the BCB from considering easing its key interest rate before October 2016, and the Tesouro (Brazilian Treasury) from reducing the yield on its bond issues.

3. This recent rate cut cannot be sustained without structural reforms

• Insufficient reforms delaying the post-2019 agenda

Recently, in addition to the difficult freeze on public spending deflated over 20 years, the BCB’s monetary policy has supported the vast budgetary adjustment currently underway. Added to this is the desire to bring the BNDES rate into line with market rates through a new long-term rate, the TLP. These reforms alone do not seem capable of significantly reducing the trajectory of public spending or correcting the structural biases of the Brazilian economy.

Thus, initially, the imbalances in the pension system, whose deficit accounts for most of the primary deficit, do not seem to be capable of significant reform in the immediate future in order to counter the increase in public debt, postponing this reform until after the election, i.e., in 2019.

Secondly, structural deficiencies will not be corrected in the short term, particularly with regard to the « Brazil cost » – which consists of a combination of cumbersome bureaucracy, tax complications, administrative layers and outdated infrastructure. Furthermore, without private banks stepping in to fill the gap left by the BDNES, medium-term investment financing appears compromised and risks further slowing Brazil’s potential growth. Finally, without reforming Brazil’s stagnant productivity, caused in part by the underutilization of its human capital, the issue of investment remains irrelevant for many agents.

• The question of the effectiveness of current monetary policy remains unanswered

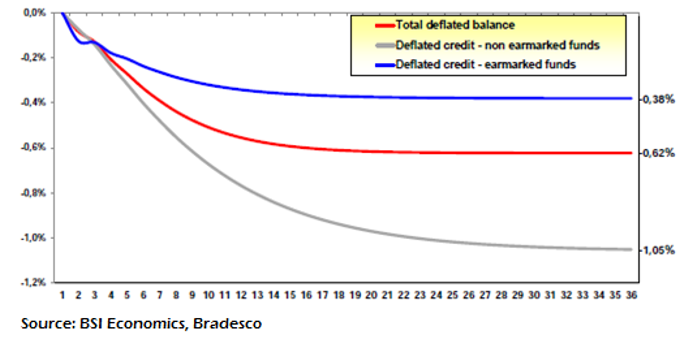

The heavy weight of public banks has led to the relative ineffectiveness of monetary policy and the response of interest rates to changes in the Selic rate. As shown in Figure 2, the response of the national financial system to a change equivalent to one standard deviation of the Selic rate has only a 40% impact due to the inertia of subsidized rates. When the Selic rate changes by one standard deviation, subsidized credit rates react three times less than private credit rates after three years. This result can be explained by the longer maturity of subsidized loans, which respond more to demand, unlike private credit, for which the Selic rate remains the main component of the cost of funding.

Figure 2 – Cumulative response to a standard deviation shock in the Selic rate over 36 months

Conclusion

The political will to break out of the high interest rate spiral in which Brazil finds itself could quickly be thwarted. While Brazil’s monetary management appears less erratic than in the past, a return to inflation seems likely with the acceleration in activity expected in 2018. In this case, given the expected context of a real interest rate below the natural rate, a rise in the base rate seems inevitable. Finally, Brazil’s attractiveness for portfolio investment would remain low, which could likely depreciate the currency in the medium term.