Usefulness of the article:The article provides an overview of capital taxation in France, comparisons with other European Union member states, and an analysis of the capital tax reforms implemented since 2018.

Summary :

- Capital is taxed more heavily in France than in other European Union countries. This is due, on the one hand, to the high level of public spending, which requires substantial financing, and, on the other hand, to a desire to tax capital slightly more than labor and consumption (relative to other European countries).

- The economic theory on optimal capital taxation is flawed, leaving the question of the fair level of capital taxation to a political decision that can be summarized as a trade-off between efficiency and equity.

- A reform of capital taxation in France was launched in 2018. The level of compulsory levies on capital should thus converge towards the European average while remaining significantly above it, at a level that is consistent with the needs of the French social model.

- According to initial estimates, the transformation of the ISF and the introduction of a single flat-rate levy on investment income will mainly benefit the wealthiest households, with a very moderate impact on growth. The abolition of the housing tax will have much greater redistributive effects.

In economics, the concept of capital is polysemic. For a household, capital is the totality of financial or real estate assets that can generate income (also referred to as wealth). For a company, it is the totality of assets used in the production process (also referred to as productive capital).

However, the boundary between these two definitions is blurred. Household savings, when invested in the financial markets (either directly or through an intermediary), constitute a source of financing for companies wishing to invest in productive capital. Households own companies when they are shareholders and provide them with funds when they become direct or indirect creditors (loans, corporate bonds).

This porosity raises the following question: what taxation system can reduce wealth inequality without preventing companies from investing in the productive capital that the economy needs? Since 2018, capital tax reforms have been implemented, one of the challenges of President Emmanuel Macron’s term of office. Here we will look at the consequences of these reforms.

1. The level of capital taxation is a trade-off between fairness and economic efficiency

The distribution of capital is very unequal in France, although this is not unique to the country. France’s net national economic wealth is nearly six times its GDP. In other words, French people hold assets worth on average six times the per capita income (€41,000 in 2018[1]). Household wealth, which accounts for most of the net wealth, is held 60% in real estate (housing and land) and 40% in financial assets (bank deposits, company shares, life insurance). As in most countries, wealth is unevenly distributed. In terms of wealth inequality, France ranks in the middle among OECD countries, where the wealthiest 10% hold more than 47% of the national wealth. Financial wealth is particularly concentrated in the hands of the wealthiest households, unlike real estate wealth, which is more evenly distributed.

Capital inequality has automatically increased as French wealth has been rebuilt since World War II, justifying its taxation. Capital inequality can be explained by differences in behavior between individuals (given equal income, some will consume more than they save) but above all by the fact that there are inequalities in income and inequalities of birth (the possibility of inheriting). As a result, capital inequality tends to reinforce itself: i) Over the course of an individual’s life, income inequality creates wealth gaps, which in turn generate income, further widening the inequality gap. ii) Over generations, an individual who inherits wealth that generates additional income is likely to pass on to their descendants even more wealth than they inherited. This is how the rebuilding of French wealth that has taken place since the end of World War II (average per capita wealth has tripled over the period) has led to growing wealth inequality, as Thomas Piketty (2013) points out. In a state that defends a meritocratic ideal, taxing capital becomes necessary.

However, taxing capital could have negative effects on long-term growth.Some economists, inspired by the work of economist Nicholas Kaldor, explain that long-term growth is very closely linked to the amount of productive capital invested in the economy. The growth rate of per capita production would thus be an increasing function of the growth rate of per capita capital. However, the various mechanisms for taxing savings/capital reduce the expected return on productive capital, which has an impact on the behavior of economic agents on two levels. On the one hand, a tax on capital reduces the incentive for households to save, reducing the funds available for business investment. On the other hand, a tax that reduces the expected return on productive capital—such as an increase in corporate tax—directly reduces the expected profits of companies wishing to invest in productive capital, which then become less entrepreneurial.

The economic theory of optimal taxation is flawed and leaves the question of the appropriate level of capital taxation to democratic arbitration.For a long time, the economic theory of optimal taxation remained fixed around the « above-ground » conclusions of Atkinson and Stiglitz (1976), who advocated the total absence of capital taxation, despite the very restrictive assumptions on which their theory was based[2]. Since the 2000s, economic theory has attempted to move beyond this horizon, but without succeeding in providing a unified and relatively consensual framework on which democratic debate could be based. The question of capital taxation has therefore remained eminently political, perceived as a trade-off between economic efficiency and equity.

However, this debate should not be reduced to the aggregate level of capital taxation in force in the country, as different methods of capital taxation have very different effects on redistribution and growth. Thus, corporate tax, property tax, and wealth tax logically have very different impacts on economic activity and inequality, since they do not affect the same households and do not generate the same reactions from economic agents.

2. A higher tax burden on capital than on other categories of taxes compared to other European countries

Capital levies in France account for 23% of total compulsory levies. Capitaltaxation corresponds to taxes and duties on the assets of individuals and legal entities. Capital taxation therefore includes various types of taxes that can be classified into four sub-categories: levies on corporate income (EUR 71 billion), on the income of self-employed workers (EUR 42 billion), on capital income received by households (EUR 40 billion – property income, dividends, interest, etc.) and finally on the capital stock held by households (EUR 91 billion – property taxes, inheritance taxes, registration fees, etc.). In total, compulsory levies on capital amount to nearly EUR 243 billion, or 11% of GDP and just under a quarter of total compulsory levies.

Table 1: Amount of compulsory levies on capital in France in 2017 by reason for taxation (in EUR billion)

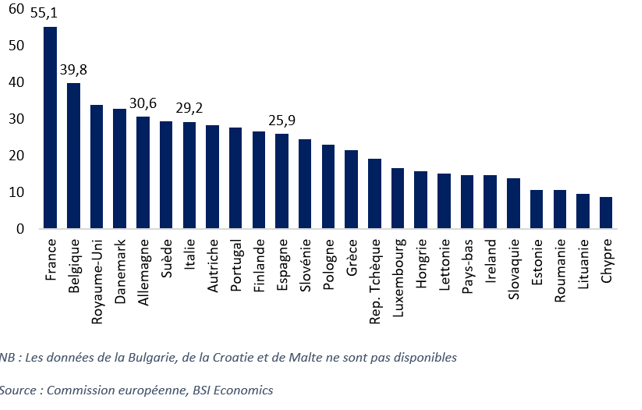

In the European Union, French capital is by far the most heavily taxed. To enable comparisons over time and between countries, the European Commission produces an indicator, the implicit capital tax rate, based on the ratio between the revenue from compulsory levies on capital and the amount of capital income recorded over a year in the same country. Comparing the implicit capital tax rate in France with that of other European Union countries, we see that France (55% –1st among 25 EU countries) taxes its capital much more heavily than Belgium (39% –2nd ), Germany (30% –5th ), and Spain (26% –11th ).. It should also be noted that the countries accused of being « quasi-tax havens » within the European Union, which are at the root of tax competition between member countries to attract foreign capital, are among the countries that tax capital the least: Luxembourg (17% –16th out of 25 countries), Hungary (16% –17th), the Netherlands (15% –19th), Ireland (15% –20th), and Cyprus (9% –25th).

Table 2: Implicit capital tax rates in 2018 (in %)

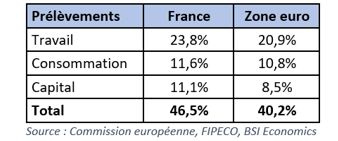

The high level of capital taxation in France can be explained in part by the high level of public spending, which justifies substantial levies. Indeed , public administration spending in France amounts to 56% of GDP, which is 7 points higher than the European Union average. Such spending, when it is structural, must inevitably be associated with significant tax revenues. As a percentage of GDP, France ranks second among European countries in terms of capital taxation (11.1% of GDP) andfifth in terms of labor income taxation (23.8% of GDP).

Table 3: Compulsory levies as a percentage of GDP by type of tax base

However, this high level of capital taxation can also be explained by a French peculiarity, which consists of increasing the tax burden on capital—and more specifically on capital stock. Levies on capital stock represent 8.9% of compulsory levies in France, compared with only 5.6% on average in the OECD. This is the result of particularly high property taxes, which are also criticized for their complexity (they are divided into four subcategories of taxes, compared with one or two in other countries, and there are problems with updating the calculation basis, which creates forms of injustice, etc.). It should be noted that France also stands out for its corporate tax rate, which is significantly higher than in the rest of the EU (the effective corporate tax rate is 32% in 2020, compared to 22% for the European average). However, the reforms that have been initiated should significantly lower this rate by 2023 (see last section).

3. Without calling into question the French social model, the capital tax reforms introduced since 2018 remove the French specificity of taxing capital more heavily than labor and consumption

1/ The 2018 tax reform: the transformation of the ISF (wealth tax) and the introduction of the single flat-rate levy

In 2018, the finance law ratified two measures that caused quite a stir: the introduction of a single flat-rate levy (PFU) of 30% on income from movable capital and the transformation of the Solidarity Tax on Wealth (ISF) into the Real Estate Wealth Tax (IFI). The first measure led to a significant reduction in the tax burden on income and capital gains from movable capital for the wealthiest households, which could previously have been subject to taxation of more than 60% on this income. The second reduced the number of taxpayers subject to wealth tax from 360,000 to 130,000, and reduced the tax base for those who remain liable for this tax, as it is now limited to real estate only (compared to movable and immovable property at the time of the ISF).

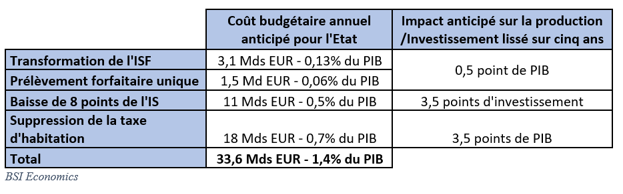

The total budgetary loss for the State is estimated at more than €4.5 billion, or 0.2% of GDP. IFI revenues amounted to €1.3 billion in the year following the reform, which corresponds to an estimated notional loss of €3.1 billion compared to a situation where the ISF would have been maintained. The budgetary cost of the PFU is estimated at between €1.4 billion and €1.7 billion. The various estimates predict a very slight positive growth gain from these reforms. This gain would come from lower capital costs and greater tax neutrality, which would increase the supply of financing to the economy. In 2019, France Stratégie estimated the additional growth gain attributable to these two reforms at 0.5 percentage points of GDP spread over five years. An estimate produced by the OECD in 2018 predicted a similar increase in GDP. It should be noted that, at the same time, these reforms would have led to a slight increase in inequality. According to France Stratégie, the gains from these two reforms would be concentrated among the wealthiest households, particularly the richest 5%. The average annual gain for these households would be close to €7,500 per year, contributing to a slight increase in the Gini index, which measures inequality (to nearly 30 points – +0.3 points).

It is interesting to note that the 2018 reform has led to opportunistic behavior on the part of some taxpayers. On the one hand, the introduction of the PFU has triggered unusual dividend payments by companies (€22 billion in 2018 compared to less than €15 billion in the previous five years). In 2013, the systematic inclusion of investment income in the progressive tax scale had increased the tax burden on dividends and encouraged companies to retain cash, boosting their cash flow and equity rather than distributing dividends to shareholders. In 2018, the introduction of the PFU had a symmetrical effect, resulting in a reduction in taxation. On the other hand, the transformation of the ISF (wealth tax) has probably encouraged wealthy taxpayers to remain in France, as shown by the statistics on the number of ISF taxpayers leaving the country: only 400 in 2018, the lowest number since 2005.

With these reforms, the marginal tax rate on capital income has moved significantly closer to the European average. France now joins the ranks of many countries offering a dual system (progressive income tax scale and a single flat rate on investment income) without taxation on movable assets.

2/ The gradual reduction in corporate income tax

President E. Macron has committed to bringing the corporate tax rate (IS) in line with the European average in order to support business investment, with a reduction of more than 8 points in the IS rate between 2018 and 2023. The effective corporate tax rate calculated by the OECD varies erratically from one European country to another, ranging from less than 9% in Hungary to more than 30% in some countries (Austria, France). France has the highest rate (32% in 2020), well above the European average (22%). The gradual reduction in the corporate tax rate in France has begun, with the effective tax rate already falling by 2.4 points over the last two years. This trend is set to continue if the measures planned until 2023 are confirmed.

As a result of the reduction in corporate tax, the state budget would be cut by more than €11 billion per year (i.e., 0.5% of GDP).Mechanically, an identical increase in companies’ after-tax profits is to be expected. This gain could be reinvested in the company or paid to shareholders. According to the latest estimates by the European Commission in 2017, the corporate investment rate would increase by 1 point in France if the corporate tax rate were to fall by 5 points. By extension, we can therefore expect the abolition of the housing tax to lead to an investment surplus of nearly 3.5 points of GDP smoothed over 5 years.

3/ Abolition of the housing tax

Another reform promised by the current president is that 80% of the population will see their housing tax completely abolished in 2020. The remaining 20% will have to wait until at least 2022. This measure directly supports household purchasing power (the average gain from the reform is estimated at €720 per household) and would eliminate a tax considered to be unequal. Indeed, the housing tax is both non-progressive and calculated on the basis of a rental value of real estate that has not been updated since 1970.

The abolition of the housing tax would cost the state an estimated €18 billion per year, or 0.7% of GDP. A March 2018 CEPII study explained that property taxes have a very negative effect on consumption and, to a lesser extent, on business investment. A 1% increase in property tax would therefore lead to an increase of nearly 3% in GDP over three years. We can therefore roughly estimate that the abolition of the housing tax will lead to a 2.1% increase in GDP over three years.

Table 4: Summary of measures and their anticipated short-term impact

Conclusion

Until now, France has been the European champion of capital taxation. This was due both to high levels of public spending, which require significant tax revenues (income from work and consumption are also taxed more heavily than the European average), and to a desire to tax capital more heavily than work and consumption—relative to other European countries.

When he became president in 2017, Emmanuel Macron embarked on a far-reaching reform of capital taxation in France, modeled on European standards. This should reduce capital taxation by nearly 1.4% of GDP, bringing the level of compulsory levies on capital in France (11.1% of GDP before the reforms) closer to the European average (8.5% of GDP). A high level of taxation remains appropriate, consistent with the financing needs of the French social model.

Each of the reforms initiated has an impact on inequality that must be considered in relation to its impact on GDP in order to assess its relevance. Ex-post estimates to be delivered in the coming years, particularly after the reforms relating to the housing tax and corporate income tax have been completed, will provide more precise information on the effects of these reforms.

Sources:

Sources:

Taxation trends in the European Union (2020)

Committee for the Evaluation of Capital Tax Reforms, France Stratégie (first report (2019), second report (2020)

Capital tax reform: the secession of the rich, Fondation Jean Jaurès (2018)

Compulsory levies on household capital: international comparisons (Benoteau and Meslin – Court of Auditors)

Taxation of Capital Income, Artus, Bozio, and García-Peñalosa (2013)

Why corporate tax rates should be lowered, Fipeco (2019)

Recent Changes in Statutory Corporate Income Tax Rates in Europe, Tax Foundation (2020)

Statutory Corporate Income Tax Rates, OECD (2020)

Fiscal Measures and Corporate Investment in France (2017)

Increasing or reducing taxes: what are the effects on the economy? The example of property tax. CEPII (2018)

Household income and wealth, INSEE (2018)

Capital in the Twenty-First Century, Piketty (2013)

« To reduce inequality, we must tax wealth, » Piketty on France Culture (2013)

« A Model of Economic Growth, » Nicholas Kaldor (1957)

Balanced growth and functional distribution, Bougi

The effect of corporate taxes on investment and entrepreneurship, Djankov, Ganser, McLiesh, Ramalho, Shleifer (2009)

« The design of tax structure: Direct versus indirect taxation, » Atkinson T. and Stiglitz J. (1976)

[1] That is, gross national income for a given year divided by the number of inhabitants.

[2] Notably: i) individuals should only differ from one another in terms of their productivity in the labor market (in other words, in a context where there are no inequalities other than those induced by differences in remuneration—for example, there is no inheritance) and they have the same preferences in terms of consumption and savings