DISCLAIMER: The opinions expressed by the author are personal and do not reflect those of the institution that employs him.

Abstract :

- The rise of shadow banking warrants continued vigilance on the part of financial regulators, while its multifaceted nature, encompassing complex structures, makes it a particularly difficult area to define and therefore to supervise.

- In view of the intrinsic risks of shadow banking, particularly with regard to financial stability, several areas of reform have been implemented since the crisis, including those related to securitization, reducing the sensitivity of money market funds to investor runs, and securities financing transactions.

- There are many difficulties associated with regulating shadow banking, including opportunities for regulatory arbitrage and the need for coordination between jurisdictions (including China).

- Nevertheless, supervisory and regulatory mechanisms have been significantly improved since the 2007-2008 crisis and now make it possible to monitor more closely and mitigate the risks arising from shadow banking. However, greater knowledge of the shadow banking universe and the prevention of emerging risks to financial stability remain a priority for regulators today.

In view of the global growth of non-bank financing and the risks it entails, financial supervisors have joined forces to supplement the applicable regulatory framework in order to ensure financial stability. According to the Governor of the Banque de France, three priorities should guide the actions of regulators: gaining a better understanding of the components of shadow banking, conducting a more in-depth study of the interconnections between financial institutions, and developing a proportionate and consistent regulatory framework at the international level.

Shadow banking is credit intermediation (i.e., maturity and liquidity transformation and credit risk transfer) involving entities and activities outside the traditional banking system, which are not subject to prudential regulation and do not benefit from central bank refinancing and therefore from the provision of emergency liquidity in the event of a crisis. These activities therefore represent a potential source of systemic risk, particularly because of their interconnections with the traditional banking system.

The current situation of shadow banking

A few facts can be highlighted by way of introduction, in order to gauge the scale of shadow banking and its implications in terms of regulation at European and global level:

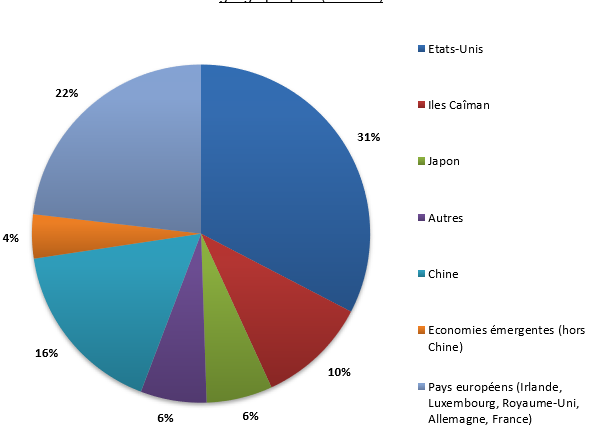

1. On March 5, 2018, the Financial Stability Board published its seventh annual report on the assessment of shadow banking[2]. Shadow banking involving systemic risk was estimated at nearly $45 trillion at the end of 2016, up 7.6% from the previous year, and equivalent to 13% of the total assets of the financial system of the countries that contributed to the exercise, i.e., $340 trillion. It should be noted that, for the first time since the exercise began, Chinese non-bank financial entities are included in the » narrow measure » of shadow banking. The United States thus accounts for nearly 40% of global shadow banking, while France accounts for 4%.

Figure 1 – Breakdown of shadow banking assets by geographical area (in 2016)

Source: FSB Global Shadow Banking Monitoring Report 2018 (2016 data). Others : Australia, Belgium, Hong Kong, Italy, Netherlands, Korea, Netherlands, Singapore, Spain, Switzerland / Emerging economies (except China): Argentina, Brazil, Chile, India, Indonesia, Mexico, Russia, Saudi Arabia, South Africa, Turkey.

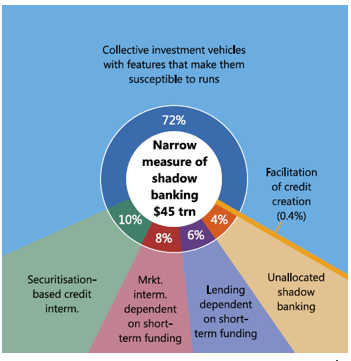

Shadow banking, according to the FSB report, breaks down as follows (see chart below). It should be noted that 72% of its assets are classified under « economic function No. 1, » i.e., collective investment vehicles (excluding money market funds) subject to maturity, liquidity, credit, and/or leverage risk and therefore potentially subject to the risk of massive outflows (bond funds, hedge funds, real estate funds, funds of funds, mutual funds, etc.).

Chart 2 – Breakdown of shadow banking assets presenting systemic risk

Source: FSB Global Shadow Banking Monitoring Report 2018 (2016 data).

2. At its last plenary meeting on October 22, 2018[6], the FSB decided to replace the term » shadow banking » with » market-based finance » due to its pejorative connotation and given that most of the » narrow measure » (i.e., asset management) remains regulated.

3. In his introduction to a Banque de France report on non-bank finance (April 2018), the Governor of the Banque de France, François Villeroy de Galhau, highlighted the role of non-bank financing in growth and innovation and the benefits of diversifying financing in Europe, while insisting on the need to prevent risks to financial stability (mainly liquidity risks of non-bank financial entities) and to improve understanding of the shadow banking universe [7] ;

4. In its October 2017Global Financial Stability Report[8], the International Monetary Fund (IMF) expressed alarm atthe steady increase in Chinese debt and the associated risks to financial stability. This phenomenon reflects both the strong growth in short-termwholesale financing (see BSI Economics note on the wholesale market in the banking sector, published in August 2013) andthe growing supply of credit from shadow banking (i.e., via trusts and off-balance-sheet credit.

What is shadow banking?

Shadow banking, or the parallel banking system, is a multifaceted and constantly evolving sector with close links to the banking sector. According to the definition of the Financial Stability Board (see BSI Economics note on the international architecture of financial regulation, published in June 2017), shadow banking isthe intermediation of credit to the public by non-banking and non-insurance entities and activities (trusts, money market funds, hedge funds, investment companies, securities financing transactions). These credit intermediation activities (maturity and liquidity transformation and credit risk transfer) represent a potential source of systemic risk, particularly due to their leverage and their interconnections with the traditional banking system.

The entities that make up the shadow banking system are therefore:

- monetary[9] and non-monetary investment funds with deposit characteristics that are vulnerable to massive withdrawals (runs), including hedge funds[10];

securitization vehicles;- broker-dealers; and

- financial companies that grant loans (leasing companies, factoring companies, consumer credit companies, etc.).

It should be noted that shadow banking can have advantages in terms of financing the economy, in that it provides investors with an alternative to bank deposits, allowing for a more efficient allocation of resources according to their specific needs (for example, money market funds are characterized by short-term investments, which limits the risks associated with fluctuations in value, and the net asset value is calculated at least daily). It thus offers a significant opportunity for risk diversification compared to the traditional banking system. Furthermore, shadow banking does not pose any risk of loss to public authorities, as the entities that comprise it do not benefit from central bank refinancing in times of stress.

However, the risks inherent in shadow banking make it an area of vigilance for financial supervisors. These risks vary depending on the players and activities involved in shadow banking. Securitization can lead to poor assessment of credit risks and correlation of defaults (due to adverse selection and information asymmetry[12]). In addition, the characteristics of repurchase agreements and securities lending/borrowing transactions[13], which are a source of low-cost financing for shadow banking ( reuse of securities as collateral and artificial inflation of securities volumes, procyclical nature of valuations and haircuts, etc.), and the characteristics of money market funds ultimately pose risks to financial stability. Finally, shadow banking has structural characteristics that can make parallel finance a less resilient form of market financing (Adrian and Jones, 2018)[14].

This is why the members of the G20 affirmed the need to prevent the risks posed by shadow banking to the economy and to strengthen its regulation (in Seoul in 2010 and then in Cannes in 2011). Regulating shadow banking requires coordinated regulation at the international level. However, implementation remains complex due to the diversity of practices and supervisors involved and the necessary combination of approaches (sectoral legislation, accounting reforms, prudential requirements, etc.).

Strengthening the regulation of shadow banking: what progress has been made in managing risks?

The Financial Stability Board has adopted a two-pronged approach: first, to establish a system for monitoring the systemic risks associated with shadow banking (which required data sharing among member jurisdictions and resulted in a single global measure, see footnote 2 on the » narrow measure « ), as well as strengthening IMF supervision in the context of its Article IV consultations and bilateral financial system assessment programs), and, on the other hand, a joint effort by the authorities to develop an appropriate regulatory framework to contain these risks.

Despite the difficulties associated with this exercise (possibilities of regulatory arbitrage, necessary extension of the scope of supervision by the authorities, coordination between G20 member jurisdictions, including China), several regulatory projects have gradually emerged and are now increasingly being finalized, particularly within the European Union.

The following international reforms are worth mentioning:

1. The Basel III framework ( see BSI Economics note on the Basel III regulatory project, published in April 2013).

Designed in addition to the « large exposures » measure (limiting banks’ exposure to the risk of default by the most indebted companies to 5%), it aims to ensure better capitalization of banks’ implicit and contingent exposures to entities in the shadow banking system. The Basel Committee has therefore worked on introducing capital requirements to cover the exposure of banks that invest in shadow banking entities.Step-in risk is characterized by the financial intervention of banking entities (in the absence of a contractual obligation to do so) to support shadow banking entities in distress, even though these entities do not belong to the same consolidation group as the banks (and are therefore not taken into account in the prudential constraints to which they are subject). The Basel Committee has published a draft common framework[17] for banks to self-identify step-in risk (where banks act as sponsors of entities outside their accounting and prudential consolidation group) and report it to the regulator. These guidelines, which are expected to be transposed into European law, could lead to the implementation of additional prudential requirements to prevent risk (based on a total consolidation approach for entities presenting step-in risk ( or) proportionate to the sponsor bank’s participation in the assets and liabilities of these entities).

2. Reducing systemic risks associated with money market funds(MMFs)

In October 2012, the International Organization of Securities Commissions (IOSCO) published a series of recommendations aimed at reducing the sensitivity of money market funds to investor runs. One of the report’s key recommendations was to encourage money market funds to ensure that their net asset value is no longer disconnected from their market value and thus reflects changes in the instruments that comprise them.

Several jurisdictions have revised their regulations accordingly, notably the United States in July 2014[19] (i.e., transition to a floating net asset value for money market funds invested in corporate and bank securities and intended for institutional investors, and the possibility for management companies to impose exit fees and/or restrictions for all non-government MMFs if the fund holds less than 30% of its total assets in the form of 7-day liquid securities) and in China in May 2015.

As for the European Commission, from 2013 until the publication of the European regulation on money market funds on June 30, 2017[20], it worked on revising European regulations on this subject. The European regulation thus proposes a restrictive list of eligible assets as well as rules on liquidity management and transparency vis-à-vis investors and competent authorities, knowledge of liabilities, regular stress testing requirements, and ensuring the good credit quality of securities in the portfolio.

3. Standardization of securitization activities

In 2012, the IOSCO worked on issuing recommendations aimed at reducing the risks associated with the structuring of securitization vehicles, in particular through product standardization and the implementation of risk retention mechanisms (i.e., requiring originators of securitized loans to retain a portion of the transferred risks on their balance sheets). In 2015, the Basel Committee and IOSCO published criteria for defining simple, transparent, and comparable securitization[21], which the European Commission used as a basis for preparing the European regulation establishing common rules on securitization (which will come into force on January1, 2019)[22] (see BSI Economics note on the Capital Markets Union and securitization, published in October 2015). Simple, comparable and standardized securitization thus has three characteristics: (i) simplicity, i.e., homogeneity of the underlying assets and a transaction structure that is not overly complex; (ii) enhanced transparency for investors (regarding the underlying assets, the structure of the transaction and the parties involved); and (iii) comparability, which should enable simple comparison between securitization products within the same asset class (see BSI Economics note « Securitization to the rescue of European financial union? », published in June 2017). In 2018, the IOSCO and the Basel Committee also adapted the requirements for simple, comparable and standardized securitization to short-term securitizations (known as ABCP, see footnote 7) in view of their specific characteristics (short maturity, diversity of issuance programs and credit and liquidity guarantees). These recommendations are intended to be implemented within national regulatory frameworks, including in the European Union.

4. Reducing the risks arising from repurchase agreements and securities lending/borrowing transactions

The 2013 Financial Stability Board recommendations on securities financing transactions, which included measures to regulate the reuse of collateral and establish data collection and aggregation processes, were followed up by work within the European Union. This resulted in the publication of the European Securities Financing Transactions Regulation (SFTR)[24] in 2016 (whose reporting requirements gradually came into force from 2018). This regulation requires (i) an obligation for counterparties to an SFT to report to central data repositories; (ii) an obligation for fund managers to be transparent with their investors about the use of SFTs; and (iii) a framework for the reuse of securities used as collateral.

Conclusion

The first step is to « demystify » shadow banking: thanks to the data collection system set up by the FSB, supervisors[25] now have a better understanding of the entities that make up shadow banking in nearly 30 countries. In addition, the current risks associated with shadow banking are being addressed by regulations that are being developed or have already been implemented at the European and international levels, particularly in the asset management sector, which includes activities that are subject to close supervision. As for the most « toxic » components of shadow banking, they are now in decline or have normalized (i.e., ABCP conduits , repo transactions , etc.). Nevertheless, the regulation of shadow banking is not a completed process. New vulnerabilities, including the continued increase in global debt, require stronger regulation and supervision of shadow banking. Emerging risks, particularly those arising from low interest rates, the search for yield, and new forms of credit intermediation based on new technologies (e.g., crowdfunding), must also be monitored closely.

Selected bibliography

– Senate, Information report on improving the transparency and regulation of the parallel financial system, May 2016

– CEPII, Les transformations de la finance chinoise (The transformation of Chinese finance), CEPII Letter No. 372, December 2016

– FSB, Global Shadow Banking Monitoring Report, March 2018

– Banque de France, Financial Stability Review, Non-bank finance: trends and challenges, April 2018, including Adrian T., Jones B., « Parallel banking sector and market financing, » pp. 13–25.

[1]For an in-depth analysis of interconnections within the shadow banking system, see Portes R., « Interconnections: mapping the shadow banking system, » Financial Stability Review (Banque de France), April 2018.

[2]FSB, Global Shadow Banking Monitoring Report, March 2018. Available online: http://www.fsb.org/wp-content/uploads/P050318-1.pdf

[3]The » narrow measure » of shadow banking, calculated according to the classification of non-bank financial entities into five economicfunctions, each involving non-bank credit intermediation posing potential risks to financial stability. See page 45 of the aforementioned 2017 FSB report.

[4]This expansion is justified on the one hand by the increase in the value of assets under management in connection with expansionary monetary policies and, on the other hand, by regulatory arbitrage; risk diversification by investors and the search for safe assets; and the development of repurchase agreements (repos) and securities lending and borrowing to address the relative scarcity of good-quality collateral.

[5]29 jurisdictions participated in the exercise, representing 80% of global GDP. These included the United States, the United Kingdom, seven eurozone jurisdictions (France, Germany, Italy, the Netherlands, Spain, Ireland, Belgium, and Luxembourg), Switzerland, Hong Kong, China, Japan, Singapore, Argentina, the Cayman Islands, India, Korea, and Russia.

[6]FSB reviews financial vulnerabilities and deliverables for G20 summit, October 22, 2018. Available online: http://www.fsb.org/2018/10/fsb-reviews-financial-vulnerabilities-and-deliverables-for-g20-summit/

[7]Excerpt from the Banque de France’s Financial Stability Review (March 2018): « It is now time to look beyond banks, following the major regulatory effort that has been accomplished with the finalization of Basel III. Market financing should not lead to irrational fears or an overly optimistic view, but rather be understood as an essential complement to banks in the efficient financing of the economy, including equity capital. The challenge now is to strike a balance between developing long-term market financing and controlling financial risks. Here too, closer international cooperation is essential in order to fully appreciate the interactions that exist between different national financial systems. »

[8]IMF, Global Financial Stability Report: Is Growth at Risk, October 2017. Available online: http://www.imf.org/en/Publications/GFSR/Issues/2017/09/27/global-financial-stability-report-october-2017

[9] Money market funds are funds known for being short-term investment tools in very short-term securities and relatively liquid money market instruments (?). They are mainly composed of money market securities with very short maturities (less than one year), such as Treasury bills and short-term bonds. They are a tool for investors to manage cash surpluses and are a key component of short-term financing for banks and businesses.

[10] Unlisted investment funds with a speculative purpose, targeting an absolute return (to be explained) and enjoying considerable freedom in their management. It should be noted that there is no common definition of hedge funds at the international level (see IOSCO’s Hedge Funds Survey, available online).

[11]Including short-term ABCP (asset-backed commercial paper) conduits, i.e., negotiable debt securities whose interest and principal payments are derived from the cash flows of a portfolio of underlying assets.

[12]The information asymmetry inherent in the » originate and distribute » model of securitization results in a phenomenon of adverse selection throughout the financing chain. A well-known example is the adverse selection in the subprime mortgage market in the United States prior to 2007, which arose in particular from securitization (due to the increasing complexity of instruments and the opacity of the market, which led to an underestimation of risk and its spread throughout the financial system).

[13]These transactions use securities deposited as collateral to generate short-term financing. Securities lending isa form of securities reuse that involves a variety of players, including both insurance companies and investment funds: a lender grants a temporary loan of securities, accompanied by a transfer of ownership of the securities lent to a borrower, who in return pays interest and provides collateral in the form of cash or securities. The borrower then returns the securities and the associated collateral to the lender.

[14]Greater leverage, complexity and opacity; risk transformation carried out along a chain of specialized and interconnected intermediaries; credit lines on off-balance sheet entities, etc.

[15]The European SystemicRisk Board has also begun to map the shadow banking system in the European Union, which feeds into its internal risk assessment mechanisms and the formulation and implementation of macroprudential policies.

[16] Shadow banking developed as a result of pre-crisis regulatory fragmentation. However, many jurisdictions are inclined to use shadow banking as a competitive advantage to attract foreign capital. Regulation therefore operates in a complex environment that cannot be resolved by regulation alone, hence the need for « peer pressure » within supranational bodies such as the FSB.

[17]BCBS, Identification and management of step-in-risk, March 2017. Available online: http://www.bis.org/bcbs/publ/d398.htm

[18]https://www.dechert.com/files/Publication/12aee394-4b76-4eb9-984e-bc3130042515/Presentation/PublicationAttachment/46aed730-b19a-4d22-aa41-2aea7f4d2c97/FS_IOSCO_FSB_01-13.pdf

[19]The US regulator, the SEC, has given money market fund managers two years to implement these measures (until October 2016).

[20]http://www.consilium.europa.eu/fr/policies/money-market-funds/The regulation came into force on July 21, 2018, initially for money market funds created after July 21, 2017, and then, from July 21, 2019, for money market funds created before July 21, 2018.

[24]European regulation on securities financing transactions (2016). Available online: http://eur-lex.europa.eu/legal-content/FR/TXT/?uri=CELEX%3A32016R1033.

[25]In addition to regional regulations (e.g., the SFTR regulation within the European Union) that provide a more detailed view of secured transactions, for example.

[26]Tobias and Jones (2018) emphasized this point, noting that « authorities and market participants should not be under any illusion that the job is done, » particularly given the still widespread risk of regulatory arbitrage, gaps in data on cross-border interconnections, and the concentration of risk among institutions in certain sectors, such as insurance.

[27]In particular, increases in sovereign debt-to-GDP ratios and household debt in advanced economies; a 100% increase in GDP since 2010 in non-bank credit intermediation activities in China; and a rise in leveraged structured finance in the United States.