Summary:

· Canadian GDP growth is expected to be more dynamic in 2017;

· The banking sector remains resilient;

· The impact of Donald Trump’s election as US president on the Canadian economy is expected to be negligible in the short term.

In 2016, economic activity in Canada was severely constrained by low oil prices, prompting the Trudeau government to implement a stimulus policy. At the same time, the federal and regional governments were forced to introduce restrictive measures for the real estate market to limit price increases, which reached 30% annually in Greater Vancouver, for example. Both of these risks appear to be easing at this stage.

However, are Canada’s economic and financial prospects more encouraging in 2017? The uncertainty resulting from Donald Trump’s election in the United States is a new risk for Canada, even if the economic cost is likely to be zero in the short term. On February 13, Justin Trudeau met with Donald Trump to discuss, among other things, the trade prospects between the two countries under NAFTA, which Trump wants to renegotiate, and thus dispel uncertainties. Furthermore, the European Parliament’s ratification on February 15 of the free trade agreement between Canada and the European Union (CETA) should increase trade, which is good news for Canada.

Acceleration of activity in 2017

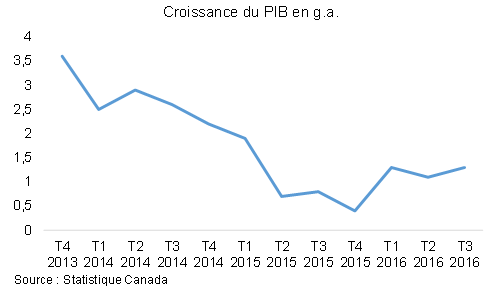

After two years of moderate GDP growth, Canada is expected to see an acceleration in activity in 2017, to 2% according to the government, compared with 1.2% in 2016. The economy should continue to benefit from domestic demand (+1.9% in 2016), supported mainly by household consumption, even if incomes are sluggish. The reform of the child benefit[1] in July 2016 should provide additional support. Residential investment, on the other hand, is expected to slow due to new regulations that have come into force as a result of sharp rises in real estate prices, particularly in Toronto and Vancouver (up 19.7% and 17% year-on-year at the end of December 2016, respectively). British Columbia, for example, has introduced a 15% tax on real estate purchases by non-residents.

In addition, private investment should benefit from a production capacity rate (81.9%) close to its historical average (83%) and a rebound in investment in the energy sector[2] starting in the second half of 2017. The rise in oil prices (+17% since the end of November 2016) should enable companies in the sector to rebuild part of their margins. Furthermore, exports should benefit from gains in competitiveness (improved terms of trade due to rising oil prices) and the trade agreement signed with the European Union (CETA), which is expected to increase exports between Canada and the EU (European Commission) by 25% by 2030. Conversely, exports would not benefit from a depreciation of the USD/CAD exchange rate (a rise in Fed rates could put downward pressure on the CAD) due to their low exchange rate elasticity[4].

The unemployment rate stood at 6.9% of the labor force in December 2016. The employment rate and labor force participation rate remained broadly stable in 2016 compared with 2015, at 65.7% and 61.1% respectively. The decline in investment in the energy sector in the first half of 2017 is expected to continue to affect employment in the most dependent provinces, primarily Alberta and Saskatchewan. However, the acceleration in activity should, on the whole, have a slightly positive impact on unemployment.

The measures adopted in the 2016 budget could increase GDP growth by 0.5% in 2017, according to the OECD. It should be noted, however, that the stimulus plan desired by Prime Minister J. Trudeau[6] will mainly be implemented during the second half of his term, which would strengthen medium-term growth, particularly by increasing productivity and developing alternative energies.

The banking system is solid, even if risks remain

Inflation in Canada reached 1.5% over 12 months at the end of December 2016, within the Central Bank’s inflation target (1-3%). The BoC could raise rates starting in the last quarter of 2017 if the Fed’s monetary policy normalization accelerates—analysts are forecasting two to three rate hikes this year—putting downward pressure on the CAD and increasing imported inflation.

In addition, a rate hike would reinforce new real estate regulations by increasing the cost of financing. Given that Canadian households are heavily indebted (170% of gross disposable income) and have a low savings rate (4% of GDI), such measures would contribute to a gradual slowdown in real estate price increases. However, these effects could be stronger than anticipated, leading to a significant decline in real estate prices (low probability in the short term). This shock, among three others[7], could be amplified by the main vulnerabilities cited by the BoC in its Financial System Review (FSR): household debt, real estate market imbalances, and fragile bond market liquidity. However, the report highlights the resilience of the Canadian banking system and an unchanged level of risk compared to the previous assessment.

What consequences could the measures announced by Donald Trump in his program have?

The economic measures announced in Trump’s program could have an impact of 0.1 percentage points of GDP by 2018 (compared with 0.5 percentage points in the United States), according to the BoC’s estimate, although it is difficult to assess the impact due to the lack of details on how these measures will be implemented.

On the one hand, the infrastructure stimulus plan and the reduction in corporate tax (from 35% to 15%) would support investment and household consumption in the United States. Canadian exports (equipment, services) would thus benefit from the excess demand. Conversely, the corporate tax cut could increase the attractiveness of the United States for Canadian companies and have a negative impact on Canada. Furthermore, President Trump’s desire to renegotiate NAFTA could damage Canadian foreign trade, as the United States is by far Canada’s largest trading partner (77% of exports, 53% of imports). Furthermore, the United States’ withdrawal from the Trans-Pacific Partnership (TPP) renders the agreement null and void, since, in order to enter into force, the agreement must be ratified by all 12 signatory countries or by six member countries whose combined GDP accounts for 85% of the total GDP of the 12 members. The Canadian government had estimated that this agreement would increase GDP by 0.13% and real income by 1.3% (Peterson Institute) in the long term.

Indirectly, the increase in political risk since Donald Trump’s election (the EPU[9] index in the United States has risen by 90 points) is being reflected in the financial markets. The Canadian 10-year bond yield has risen by 54 basis points since Donald Trump’s election, which could increase the cost of financing the Trudeau government’s stimulus plan.

Finally, the renegotiation of the softwood lumber export agreement, a market worth CAD 4.7 billion in 2016, could be unfavorable to Canada. The U.S. International Trade Commission has ruled that Canadian softwood lumber exports are subsidized and harm U.S. producers. Analysts are predicting the introduction of an import tax of around 25%, with a significant risk of repercussions on employment in British Columbia, which accounts for 50% of Canadian exports to the United States.

Conclusion

The new budget measures and the recovery in investment should have a positive impact on the Canadian economy in 2017. In addition, measures implemented in the real estate sector should curb price increases. However, the sector will remain under scrutiny in the event of a sharper-than-expected slowdown in prices, which could have a significant impact on the banking sector given household debt levels (unlikely in the short term).

Finally, the lumber sector and, more generally, export companies could be the losers of President Trump’s desire to renegotiate trade agreements. However, renegotiating the two agreements (lumber and NAFTA) would lead to a significant increase in prices for US consumers. A renegotiation could therefore be reached that does not fundamentally alter the broad outlines of the agreements.

Bibliography:

http://www.bankofcanada.ca/wp-content/uploads/2017/01/mpr-2017-01-18.pdf

http://www.bankofcanada.ca/wp-content/uploads/2016/12/fsr-december2016.pdf

http://www.bankofcanada.ca/wp-content/uploads/2017/01/fad-press-release-2017-01-18.pdf

http://www.bankofcanada.ca/2016/12/fsr-december-2016/

http://www.crea.ca/housing-market-stats/national-average-price-map/

[1]The reform eliminates and replaces the various family benefit systems with a single, more generous and tax-free financial assistance system.

[2]Oil production was also affected by the major fires that occurred in May 2016 in Fort McMurray, Alberta. The cost (direct and indirect) is estimated at around CAD 9 billion, according to the authorities.

[3]Oil exports accounted for 15.3% of Canada’s total exports.

[4]Source: BoC monetary policy publication

[5] In addition to reforming the child benefit, the 2016 budget provides, among other things, lowering the second tax rate by 1.5 percentage points to 20.5%, reducing the waiting period for employment insurance benefits, investing more than CAD 120 billion in infrastructure over 10 years, increasing student grants, creating a CAD 2 billion Low Carbon Economy Fund over two years, etc.

[6]This includes immediate investments of CAD 11.9 billion in infrastructure and an additional CAD 81 billion in infrastructure and rural communities by 2027-2028.

[7]Sharp rise in long-term interest rates, stress from China and other emerging countries, low commodity prices over an extended period.

[8]The impact of this measure on the Canadian economy is expected to be zero in 2017, as the plan cannot be implemented before the next budget process, which begins in October. It should be noted, however, that Donald Trump has signed an executive order accelerating the construction of the Keystone XL project, connecting Alberta to Nebraska via a 1,900 km pipeline. The Conference Board of Canada estimates that oil exports would increase by 1 million barrels per day by 2030 as a result of this project.

[9]The Economic Policy Uncertainty Index (EPU) measures the level of uncertainty surrounding economic policy through the press, tax provisions and economists’ forecast discrepancies (see BSI’s note on this subject, « Economic policy uncertainty: an index to measure it, » dated November 24, 2015)..

[10]This agreement expired in October 2015 and was renewed for 12 months.