Abstract :

- The Japanese economy has benefited from a period of accelerated growth driven by robust household consumption and a weak yen, which favors exports. Investment also remains buoyant thanks to the prospect of the 2020 Olympic Games and a dynamic tourism sector.

- Similarly, the archipelago’s industrial structure (highly diversified with a dynamic high-tech sector) and high national savings are also factors contributing to the country’s economic dynamism.

- However, Japan faces risks, foremost among which are massive public debt (and the need for fiscal consolidation that this entails), the slow return to stable inflation, and protectionist risks.

- In the long term, an aging population and chronic underinvestment are fueling prospects of secular stagnation.

Six years after the launch of « Abenomics » (a highly accommodative monetary policy combined with fiscal stimulus and structural reforms), the Japanese economy appears to have regained some stability in terms of growth. What are the biggest contributors to this recovery? What risks could reverse this cycle?

An economy buoyed by household consumption and fiscal stimulus measures

Buoyed by foreign trade and Shinzo Abe’s stimulus measures, the Japanese economy ended 2017 with growth of 1.7%—well above the estimated potential growth of 0.8%. In the short term, protectionist risks (see details below) are likely to weigh on foreign trade and therefore on Japanese exports, primarily to their Asian partners.

In terms of business investment, the appreciation of the yen and protectionist risks are the main sources of concern for the coming months. However, for households, rising corporate profits and near full employment (at 2.8%, the unemployment rate is at its lowest since 1994) should lead to an acceleration in wage growth and thus support household consumption – albeit with a subsequent risk of higher imports.

The measures taken by Shinzo Abe to encourage companies to increase wages in exchange for a reduction in corporate tax for the 2018 fiscal year should be beneficial for household consumption (however, the deflationary outlook of companies, which does not encourage them to redistribute profits, remains an obstacle to this rise in wages). Similarly, the VAT increase expected in October 2019 (from 8% to 10%) should lead to anticipatory purchasing behavior between now and then. This VAT increase, which is necessary to consolidate public finances (see below), has nevertheless been postponed until October 2019 so as not to penalize the recovery in household consumption (the previous VAT increase in 1997 was one of the main triggers of Japan’s slide into recession).

The BoJ’s quantitative easing policy is struggling to bear fruit

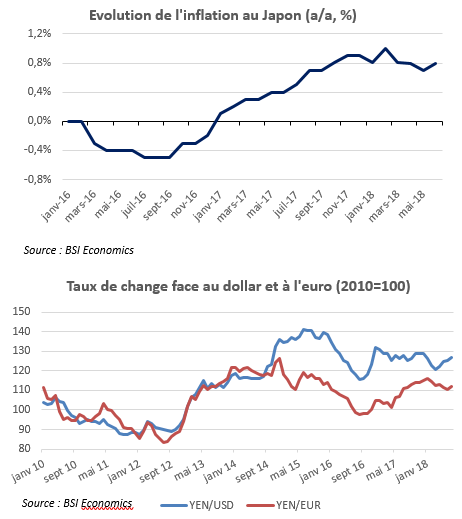

The Bank of Japan’s (BoJ) highly accommodative monetary policy, aimed at boosting credit and therefore production and employment, is associated with a 2% inflation target, a yield on 10-year government bonds of around zero, and a short-term deposit rate of -0.1%. However, in April 2018, the BoJ abandoned its forecast of when it would reach its 2% inflation target (after postponing it six times, most recently to March 2020).

As can be seen in the chart opposite, this target is currently far from being achieved. One of the main reasons put forward by BoJ Governor Haruhiko Kuroda to explain this slump is that consumers continue to refer to the long period of deflation in the 2000s when setting their price expectations. Monetary tightening by other major central banks (Fed, ECB, BoE) should mitigate the risk of yen appreciation against other major currencies (see chart below), which would be positive for exporting companies and should help generate imported inflation, already reinforced by rising commodity prices.

An aging population weighs on growth opportunities and public debt

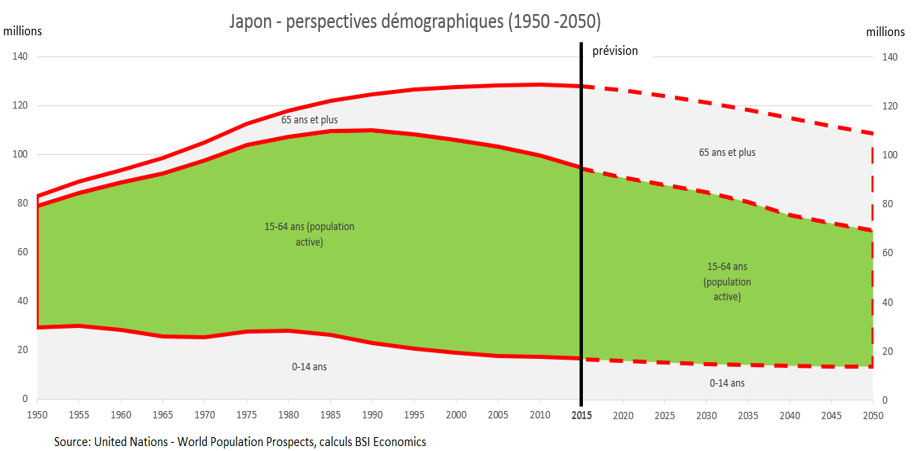

Japan’s demographic problems are an increasingly significant obstacle to economic growth. As the chart below shows, forecasts for the period 2015-2050 point to a double phenomenon of a reduction in the total population and in the share of the working-age population (aged 15-64) in that total population. In times of growth, the potential labor shortage caused by this demographic handicap is a drag on business activity and growth opportunities.

At the macroeconomic level, this translates into a growing slowdown in potential growth. At the business level, this translates into increased production abroad by large manufacturing companies and significant difficulties for micro-enterprises and SMEs. Other sectors[1] are bound to encounter structural difficulties due to this negative demographic trend – even if the negative effects of this trend should be mitigated in the short term by major upcoming international events (the 2019 Rugby World Cup and the 2020 Summer Olympics) that will benefit the economy. One of the major consequences of this situation is a slowdown in business investment. These demographic prospects are also putting pressure on pension systems and healthcare spending in general, which are placing an increasing burden on public debt.

Public debt remains a ticking time bomb

Public debt is the second biggest risk to the Japanese economy. At 240% of GDP in 2017, it poses a growing risk of a reversal in confidence. The significant fiscal stimulus and ultra-accommodative monetary policy implemented since 2013 by Shinzo Abe (the famous « Abenomics ») have led to a massive increase in the country’s debt. The VAT increase planned for 2019 is unlikely to be enough to restore the primary balance in 2020, as the government has set as its target. The budget deficit accelerated further in 2017 due to fiscal stimulus measures and the cost of infrastructure development for the 2020 Olympic Games.

However, the fact that more than 90% of public debt is held domestically limits the risk of derailment, even if the trajectory of debt accumulation (debt servicing accounts for 25% of the debt) raises questions about its sustainability. For the time being, however, the current maintenance of growth above the yield on government bonds remains a guarantee of debt control.

Significant dualism in the labor market remains a drag on productivity

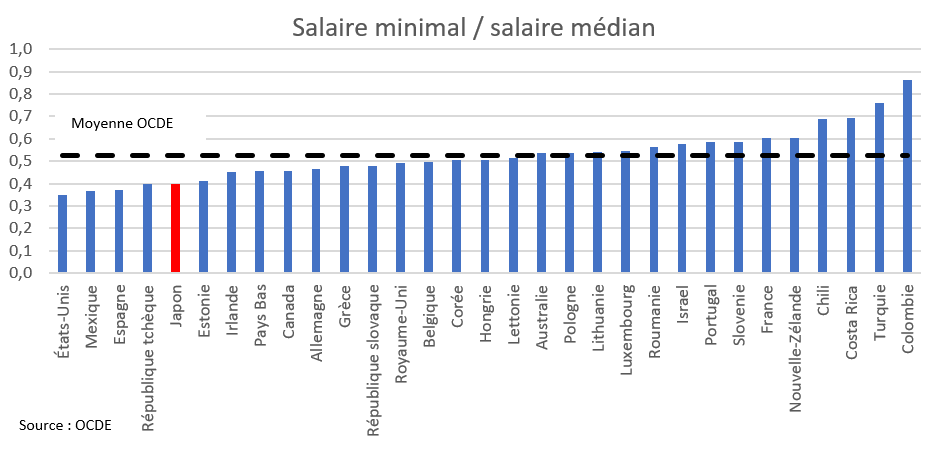

Finally, low labor productivity is also a drag on growth. Indeed, the growing productivity gaps between industry and services and between innovative and lagging companies (see the article on the productivity puzzle) have led to significant differences in wages and incomes. This dualism in the labor market has negative consequences in terms of productivity, as the large proportion of temporary workers (38% of total employment) receive little vocational training and have limited social security coverage. The significant gap between the minimum wage and the median wage (see graph below) illustrates this problem.

Similarly, the low integration of women into the labor market is illustrated by a significant wage gap between men and women, as well as unfavorable external factors (gaps in childcare facilities, long working hours, etc.).

The low rate of business creation and liquidation is also symptomatic of this phenomenon, due in part to the widespread use of personal guarantees and a particularly severe personal bankruptcy system.

US protectionism and North Korea: two external risks for Japan

Certain external risks also weigh on the Japanese economy, foremost among which is the protectionist policy initiated by Donald Trump. Japan is one of the countries with which the United States has a trade deficit and is therefore targeted by the import tariffs that Donald Trump wants to implement; the Japanese automotive sector is particularly exposed to this risk. The losses in terms of exports could therefore be significant. With regard to North Korea, recent diplomatic advances (the Trump-Kim meeting, the agreement on the denuclearization of the Korean peninsula) have reduced the risk of military conflict and thus reassured Asian markets, which had been shaken by the ballistic missile tests conducted in 2017.

Conclusion

Japan should benefit from a favorable cycle over the coming quarters. Abenomics are having a positive effect on household consumption and investment, while exports continue to be buoyed by a weak yen. However, the VAT increase planned for 2019 could dampen this economic momentum, as could protectionist risks to international trade. In the longer term, the prospects of secular stagnation and unmanageable public debt are the main structural risks.

[1] Construction, retail, medical services, security, catering/hospitality, and personal services.