Abstract :

:

- By addressing the issue of growing wealth inequality, the Zucman tax seeks to establish greater fiscal equity. This tax proposal also comes at a time when there are calls for collective efforts to restore public finances.

- However, this proposal faces several operational limitations, both economically and legally.

- While the Zucman tax could lead to tax exile among the wealthiest individuals, the extent of this risk remains to be seen.

- The proposal faces legal barriers, particularly in its approach to taxing unrealized capital gains, which seems difficult to reconcile with economic reality.

- Rejecting it without proposing a credible alternative adds no value and does not address the issues it raises. On the contrary, this tax should serve as a basis for broadening the debate in order to explore several avenues relating to asset holding companies (inheritance tax, national preference for investment, incentive mechanisms to link high net worth individuals and public services).

Download the PDF: zucman-tax-opportunities-fantasies-and-alternatives-part-1

The « Zucman tax, » approved by the National Assembly before being rejected in June 2025 by the Senate, has sparked heated debate in France. Economist G. Zucman supports a plan to tax net wealth exceeding €100 million at a rate of 2%. While this proposal comes at a time when public finances need to be rebalanced, the structural problem it raises is that of significant wealth inequality in France. The Zucman tax therefore reintroduces a quasi-secular issue that remains unresolved at this stage: restoring a form of fiscal equity. However, it is generating a wave of concern, particularly because of the tax exile it could provoke and its impact on the financing of innovation.

Beyond the debates on its principle, it has two significant merits. First, it is an innovative proposal on an important subject, which is far from negligible in the current French economic debate. Furthermore, it contributes to the discussion on issues that require innovative approaches. It has already elicited constructive responses (see this opinion piece) and suggestions (we will come back to this).

This note seeks to take stock of this proposal, particularly by examining its limitations. It is supplemented by a second note that explores alternatives.

Reminder: large fortunes and asset holding companies

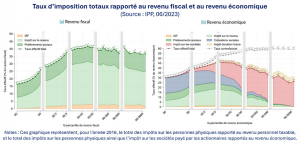

The basic premise of the Zucman tax is that the French system does not offer a solution to the problem of growing wealth inequality, which has exploded over the past 20 years (see this INSEE analysis). This system, a pillar of redistribution[1], focuses mainly on income taxation. However, the effective level of taxation on income in France is relatively lower for the wealthiest individuals (the richest 0.01%, see this note from the Institut des Politiques Publiques (IPP) and the graphs below).

In fact, the latter tend to have economic incomes that far exceed their taxable incomes[2]. These economic incomes benefit from more favorable taxation thanks to various tax optimization systems (asset holding companies), which allow income tax to be circumvented.

For an individual who has started their own business, setting up a holding company involves placing the shares they hold in their company, as well as other sources of income related to this activity (dividends, rental income, capital gains), in a structure (holding company) whose income is subject to corporate tax. This means that part of their income is not derived from their salary (taxable income) and income derived from capital holdings is not taxed under the individual tax regime (flat tax of 30%) but under the asset holding company regime, which is significantly more advantageous (minimum effective rate of 1.25%).

The main purpose of asset holding companies is to avoid double taxation on dividend income between a parent company and its subsidiaries (see ndbp 2) and to transfer assets via the Dutreil Pact, which offers a tax allowance on inheritance[4] (an important aspect that will be discussed in a second note).

The Zucman tax would therefore seek to correct a tax loophole, where the existence of such optimization systems prevents the relative contribution of the wealthiest individuals to the nation’s revenue from being adjusted. This tax optimization implies a de facto form of injustice towards the middle and upper classes, who bear a disproportionate share of the budgetary burden.

A significant risk of tax exile, but one that needs to be qualified

The argument of tax fairness is particularly emphasized to justify the introduction of such a tax, especially as wealth inequalities are widening. This system of holding companies, while not unique to France, does not exist in the United States, for example, where such holding companies pay a specific income tax of 20% in order to prevent income tax evasion, as is the case in France. While it is difficult to argue against striving for greater tax fairness, this tax is nevertheless the subject of much criticism, both economically and legally.

If adopted, the Zucman tax would pose a threat to large fortunes, which could be led to « leave the country » by moving their assets to a country with a more favorable tax regime. This is the famous riskof tax exile, the logic of which is as follows: the gains generated by the tax revenue from the Zucman tax would be more than offset by the losses associated with the departure of large fortunes, which also play an important role in the real economy through the investments they make in the country.

This argument, while entirely valid, must nevertheless be qualified. While transferring a holding company outside France is possible within the European regulatory framework (cross-border TUP, which nevertheless imposes certain conditions), such a process can be lengthy and costly (especially as it exposes the holding company to a potential » exit tax » ), which could discourage any desire to leave. Furthermore,the July 2025study by the Economic Analysis Council (CAE), which measured the impact of higher capital taxation on tax exile, presents mixed results. It shows that when capital taxation increases:

- This leads to outflows of income by the wealthiest populations.

- However, in France, the sensitivity to leaving is on average lower among the wealthiest than among the rest of the population in this specific scenario.

- To date, tax exile has had significant direct negative effects on the aggregate turnover of French companies, added value, and employment.

- On the other hand, when indirect effects are taken into account, the total economic impact of departures induced by this increase in taxation is low (see table below).

Significant legal barriers

The Zucman tax has also raised objections from legal experts, who consider it unconstitutional. Such a tax would not be proportionate to individuals’ ability to pay, which in France is based solely on income earned. However, by focusing on net wealth, the Zucman tax would impose capital gains[8] linked to the holding of assets, which from a constitutional point of view can only be taxed at the time of the sale of said assets.

The example of the founders of Mistral, a leading French unlisted company in the field of artificial intelligence, is often cited to illustrate this situation. The founders of Mistral hold shares in their company, currently valued at several billion euros. The unrealized capital gains linked to the holding of these shares would automatically fall under the Zucman tax. The founders would therefore most likely find themselves unable to pay the tax amounts linked to this wealth valued at billions but disconnected from their actual income level.

In this specific case, economist G. Zucman proposes an alternative, consisting of paying the tax « in kind. » Using the same example, the logic would be as follows: the founders of Mistral would have to sell part of their shares to the government, for an amount equivalent to the tax owed. The state would then have the right to sell them to Mistral employees or French investors. In practice, this proposal faces several obstacles.

First, for an unlisted company like Mistral, such an operation would be very complicated from a technical standpoint. It would require a complex financial arrangement to buy back the shares held by investors, which would weigh on the company’s development. Furthermore, investors could be discouraged in the future from investing their funds in this company and other innovative French start-ups. This would deal a severe blow to the emergence of high-potential companies in several sectors. Finally, payment in kind would most likely violate the principle of property rights.

While commendable in its spirit of restoring a form of tax fairness, the Zucman tax faces several limitations. As such, it cannot be adopted without several profound changes. This is precisely the subject of the second part of this note, which looks at potential alternatives. To be continued!

Article written on September 19, 2025

[1] This INSEE note details the effects of redistribution on income inequality, while showing that its effectiveness does not prevent the poverty rate from increasing.

[2] According to the definition used by the IPP, taxable income refers to « the income tax base before the application of various specific allowances, while economic income is broader and refers to income « actually earned and controlled by the tax household » and includes, in particular, income subject to corporate tax, typically that linked to the holding of shares in holding companies. »

[3] Under the holding company system, the level of taxation on income corresponds to that of corporate income tax (25%), to which an exemption of up to 95% applies. Therefore, with the maximum exemption: 5% x 25% = 1.25%. It should be noted that in order to benefit from the 95% exemption, the following conditions must be met: holding at least 5% of the capital of a company for a period of at least two years.

[4] These holding companies also make it possible to centralize different ranges of assets (movable and immovable) in a single entity, facilitate restructuring, transfers, mergers, and acquisitions within a group, and increase investment capacity (possibility of leveraging through the holding company without increasing personal debt).

[5] Such mechanisms also exist in the Netherlands, Cyprus, Luxembourg, and Singapore.

[6] However, the effective income tax rate is much lower in the United States than in France.

[7] These effects include corporate restructuring and labor market reallocations, all of which are described in detail on page 15 of the report.

[8] An unrealized capital gain is a potential gain linked to the holding of a financial security or asset that has not yet been sold. For example, an asset with an initial value of 100 that is now valued at 110 offers an unrealized capital gain of +10, but until the asset is sold, no real capital gain is recognized.