Abstract:

● Exchange rate pass-through to prices can be defined as the change (upward or downward) in various prices in an economy following an appreciation or depreciation of its exchange rate.

● This transmission is neither complete nor immediate. Its importance seems to have diminished in the euro area in recent years, but there are differences between Member States;

● These differences stem from the various factors influencing this transmission, which can be divided into two categories: factors related to globalization (the international role of the euro, the type of goods traded, trading partners, etc.) and factors related to corporate strategies and market structures (competition, the type of currency used for trade, etc.).

The degree to which exchange rate movements have an impact on domestic prices appears to have declined in recent years in the euro area, according to a ECB study published in September 2016([1]). This study highlights the potential factors behind this decline, as well as the reasons behind the differences in the transmission of exchange rates to inflation in the euro area Member States.

After reviewing the mechanisms involved in the transmission of exchange rate movements to different prices in an economy, we will examine the extent to which the production structures of the main euro area economies and the globalization of trade affect this transmission.

1. The three stages of the transmission of exchange rate movements to prices in an economy

The transmission of exchange rate changes to prices can be defined as the degree to which prices in an economy rise (or fall) following a depreciation (or appreciation) of the exchange rate. A distinction must be made here between the different stages of exchange rate transmission to prices, particularly between import prices and consumer prices (Figure 1). The impact of the exchange rate on import prices is determined by the pricing strategies of domestic importers and foreign exporters, the sectoral and geographical breakdown of a country’s imports, and the use of the national currency in trade. The impact of the exchange rate on the level of consumer prices (HICP), the second stage, depends mainly on an economy’s integration into global value chains (GVCs) and the pricing strategies of companies in the domestic market. The impact of the exchange rate on prices also includes a third stage, between the HICP and export prices, and depends on the extent to which domestic exporters can adjust their prices or margins following a rise in domestic prices, given competition for their international market shares.

Figure 1. The three stages of exchange rate transmission to prices

Sources: author, BSI Economics

There are several reasons why the transmission of exchange rate movements may be incomplete, i.e., either delayed or partial. At the import price level, attention should be paid to competition between foreign exporters (outside the euro area) for market share in the euro area, which determines their pricing policies. The degree to which changes in import prices are passed on to consumer prices in a country depends in turn on competition in the domestic market. The impact on consumer prices is then smaller and materializes later. The increase in production costs following the increase in the prices of imported goods fuels inflationary pressures throughout the economy, but these can be partially offset by the fact that some domestic companies may decide to keep their prices constant and thus cut their margins, thereby limiting the final impact on the HICP.

Thus, the overall impact of exchange rate movements on domestic prices is a combination of direct and indirect channels that overlap and differ in importance and timing. A distinction must be made between factors arising from corporate strategies (currency used for trade, pricing strategies, market structures, etc.) and factors related to the globalization of trade (the weight of emerging economies, integration into currency boards, trade dynamics, the international role of currencies, etc.).

2. Exchange rates, margins, and market share: how flexible are companies’ pricing strategies?

First, the choice of currency used in international trade is a major factor in the extent and speed of exchange rate transmission to import prices. The stability of the euro and its international role have led more foreign companies to use this currency for their exports to the euro area. A foreign company exporting euro-denominated products to the euro area may choose not to pass on the full impact of a depreciation of the euro to its selling prices in order to remain competitive. It would therefore decide to absorb the exchange rate risk to maintain its market share in the euro area. In addition, the larger share of trade within the euro area may have reinforced the overall decline in exchange rate pass-through by increasing imports from member states invoiced in euros, which are not subject to exchange rate fluctuations. Furthermore, the choice of billing currency may also be part of a company’s strategy (to limit transaction costs, stabilize profits by protecting against currency volatility, etc.).

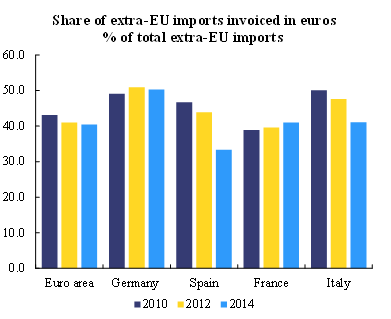

The transmission of exchange rates to prices may be lower (later and less significant) in Germany than in France, Spain, or Italy due to the larger share of their imports invoiced in euros. Germany stands out with a very stable 50% share of its non-EU imports invoiced in euros (Chart 1), while Spain and Italy experienced a significant decline between 2012 and 2014. In France, this share is increasing slightly but remains 10 points below that of Germany. These figures seem to show the variety in exchange rate pass-through levels: Germany appears to have lower exchange rate pass-through due to the larger share of its imports invoiced in euros, while in Italy and Spain there has been a change in the currency used for these imports.

The more a euro area country imports goods priced in euros, the less it will be subject to price effects due to changes in the euro exchange rate, and therefore the less significant and rapid the transmission of exchange rate policy will be.

Figure 1. Share of non-EU imports denominated in euros (% of total non-EU imports)

Sources: Eurostat, BSI Economics

In addition to the choice of currency used for trade, the degree and speed of exchange rate pass-through to prices can be determined by the pricing policies that companies adopt given the elasticity of demand for their goods in the destination market. The degree to which companies can adjust their margins after a depreciation depends on how substitutable their products are. As noted by Bussière (2013), the degree of competition in a market has an impact on the transmission of the exchange rate to prices. When an importing company experiences a negative exchange rate effect and sees the price of its imported inputs rise, it has more leeway in an oligopolistic market to pass on this increase to its selling prices without jeopardizing its market share. On the other hand, in a more competitive market, a company may choose not to pass on this increase in the price of its inputs to its selling prices and thus reduce its margins in order to maintain its price competitiveness. The transmission of the exchange rate to prices therefore appears to be less complete in more competitive markets.

3. Globalization: a factor of structural change in the relationship between exchange rates and domestic prices

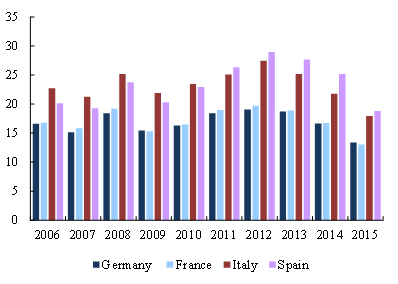

The scientific literature has identified changes in the sectoral and geographical composition of a country’s imports as one of the main factors in the decline in the impact of the exchange rate on domestic prices. As noted by Campa and Goldberg[3], commodity-based goods tend to be priced in dollars on a single global market with highly homogeneous but highly volatile prices. Imports of commodities

represent a larger share of total imports in Italy and Spain (Figure 2), it is likely that prices in these economies are more sensitive to fluctuations in commodity prices and changes in the euro/dollar exchange rate (as these products are often denominated in USD), unlike countries that import goods with more stable prices.

Chart 2. Share of raw materials in total imports (%)

Sources: Eurostat, BSI Economics

Second, the growing importance of low-cost producers in international trade has fostered international competition and, as a result, incomplete transmission of exchange rate movements to the prices of foreign companies. The growing share of euro area imports from emerging economies, which tend to absorb exchange rate movements in their margins and keep their prices constant in order to maintain their market share, is leading to a decline in the pass-through of exchange rates to import prices in the euro area (Bussière, 2013).

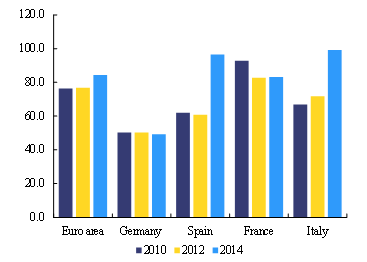

Energy imports account for a significant share of total imports for most euro area Member States. In the case of Italy and Spain, it is not the price of oil that has changed, but rather the currency used for oil imports. While in 2012, 70% of Italy’s oil imports and 60% of Spain’s were invoiced in dollars (Chart 3), this rate rose to almost 100% in 2014 for both countries. In Germany, oil imports in dollars remained stable and less significant (around 50%). In France, this rate remains slightly higher but has been falling in recent years. This would partly explain why import and consumer prices in Italy and Spain are more sensitive to exchange rate movements than in France or Germany, as distribution costs are more affected by changes in the euro/dollar exchange rate. The more imported products are denominated in foreign currencies, the more local companies are exposed to exchange rate risk on the goods they import.

Chart 3. Share of oil imports denominated in dollars (% of total oil imports)

Sources: Eurostat, BSI Economics

Finally, the gradual integration of euro area countries into global value chains (GVCs) may also lead to changes in how prices respond to exchange rate movements. The globalization of production processes can significantly alter the various stages of the transmission of exchange rate movements to prices. In particular, it is important to consider a country’sbackward linkages in GVCs, i.e., the share of imported inputs in domestic value added and in exported value added.

First, greater import penetration[4] may be associated with greater market power for foreign companies and therefore greater leeway to maintain their profits and pass on exchange rate movements to their prices. Second, a higher share of imports of intermediate goods can lead to inflationary pressures following a depreciation of the exchange rate, as producers see their production costs increase and may pass them on to prices in order to maintain their profit margins.Backward linkages are therefore a source of increased transmission of exchange rate movements to consumer prices. The same mechanism is at work for export prices: the greater the share of imported goods in exported value added, the smaller the gains in price competitiveness after a depreciation of the exchange rate, as the decrease in export prices is partly offset by an increase in production costs. Assessing the transmission of exchange rates to different prices in an economy is therefore essential for anticipating the impact of exchange rate movements on inflation or the price competitiveness of exporting companies.

Conclusion

To sum up, certain factors identified in the literature explain the decline in the transmission of the exchange rate to prices in the euro area, as well as the differences between Member States. For Italy and Spain, the different composition of their imports and market structures could explain the greater sensitivity of domestic prices to changes in the euro exchange rate compared with Germany or France. Changes in the euro exchange rate therefore have asymmetric effects on inflation and price competitiveness in different euro area countries.

Bibliography

● Auer, R., and Schoenle, R., (2016) “Market structure and exchange rate pass-through” Journal of International Economics, 98, pp. 60-77.

● Bussière, M., Delle Chiaie, S., Peltonen, T., (2014) “Exchange Rate Pass-Through in the Global Economy: The Role of Emerging Market Economies” IMF Economic Review Vol. 62, No. 1

● Campa, J.M., and Goldberg, L.S., (2005) “Exchange rate pass-through into import prices” The Review of Economics and Statistics, vol.87, is. 4, pp. 679-690.

● Choudhri, E. U., Hakura, D. S. (2015) “The exchange rate pass-through to import and export prices: The role of nominal rigidities and currency choice” Journal of International Money and Finance, Vol.51, pp.1-25.

● Di Mauro, F., Rasmus, R., and Irina B., (2008) “The changing role of the exchange rate in a globalized economy” ECB Occasional Paper Series, no. 94.

● European Central Bank (2016) The international role of the euro. Interim report. June 2016

● European Commission (2014) “Member States vulnerability to changes in the euro exchange rate”, Quarterly report on the euro area, vol. 13, is. 3, pp. 27-33.

● Faruquee, H., (2006) “Exchange Rate Pass-Through in the Euro Area” IMF Staff Papers, Vol. 53, No. 1

● Osbat, C. and Wagner, M.,(2006) “Sectorial exchange rate pass-through in the euro area”, available at www.cide.info/conf/papers/O2.pdf

● Özyurt, S., (2016) “Has the exchange rate pass through recently declined in the euro area?” ECB Working Paper Series, No. 1955.

[1]Özyurt, S., (2016) “Has the exchange rate pass through recently declined in the euro area?” ECB Working Paper Series, No. 1955.

[2] Risk for a company of seeing the currency in which the prices of its final products are denominated depreciate against the currency in which its production costs are denominated. In the short term, this company can either increase its selling prices to maintain its margins or reduce its margins to remain price competitive.

[3]Campa, J.M., and Goldberg, L.S., (2005) “Exchange rate pass-through into import prices” The Review of Economics and Statistics, vol. 87, is. 4, pp. 679-690.

[4] Volume of imports of goods and services as a percentage of total final expenditure at constant prices (OECD)