Usefulness of the article: After nine years of armed conflict, Syria’s economy is in tatters. The war has devastated key economic sectors (oil/natural gas, agriculture, textiles, tourism, etc.) and economic recovery does not appear to be on the horizon. The difficult political transition, ethnic tensions exacerbated by the conflict, and the flight of foreign investors threaten to undermine the country’s recovery. This study analyzes the impact of the revolution on Syria’s main economic sectors.

Disclaimer: The data contained in this study comes from reliable sources. However, it is only valid for areas controlled by Bashar Al Assad’s regime.

Summary:

• Before the civil war, the Syrian economy was heavily dependent on its hydrocarbon resources, mining sector, textile industry, agricultural production, and tourism.

• Since the start of the civil war, industrial production has collapsed and the disorganization of the agricultural sector continues to threaten food security.

• Between 2010 and 2018, Syria’s GDP contracted by around 65%.

• Manufacturing and mining accounted for an average of 23% of GDP over the period 2006-2010, before falling to 10.7% of GDP over the years 2011-2017.

• The cost of the war has been estimated at around USD 300 billion in capital losses due to destruction throughout the conflict.

• Although the decline in GDP is beginning to slow, a sustainable recovery in economic activity is unlikely in the short to medium term.

• Reconstruction will depend mainly on foreign direct investment, primarily from Russia and Iran.

The Syrian Arab Republic was one of the countries affected by the Arab Spring in 2011. With a small, poorly diversified economy focused on low value-added industries, the country had a relatively low GDP per capita of around $2,800 in 2010 (ranked 179th in the world).

Before the outbreak of civil war in March 2011, the Syrian economy had a GDP of $60 billion (2010) with relatively high hydrocarbon production, which alone accounted for 35% of export earnings and 20% of government revenue. The mining sector, particularly through phosphate production, agriculture (including cotton for the textile industry), and tourism were the main areas of the economy.

All economic sectors have been impacted by the civil war, but the lack of data on certain industries makes it impossible to quantify the impact of the conflict on each sector. That is why this study focuses on five key sectors: the oil and gas industry, the mining sector, agricultural production (including cotton used by the textile industry), and tourism.

Over the period 2011-2017, the total cost of physical destruction is estimated at USD 114.1 billion by the United Nations. Transport, manufacturing, electricity production and distribution, and health account for 12.6%, 9.9%, 6.2%, and 4.5% of physical destruction, respectively. Education comes next, accounting for 3.4%.

1. A sharp decline in GDP and a drastic drop in trade

A sharp contraction in GDP

With a GDP of $60 billion in 2010, Syria had been experiencing continuous growth for several years, due in particular to a policy of partial economic liberalization initiated in 2000 with the arrival in power of Bashar Al Assad. This policy mainly targeted the banking sector, with the introduction of private banks in 2004. The consequences were visible from the first year, with economic growth averaging 5% per year until the start of the civil war. However, the success of this liberalization must be qualified, as other economic difficulties remain. Indeed, the gradual depletion of oil reserves since the early 2000s, combined with growing domestic demand for energy, is depriving the regime of valuable tax revenues.

Since the beginning of the conflict, the Syrian economy has contracted, with varying degrees of annual recession. The year 2013 saw the deepest recession, with GDP falling by 26.3% compared to 2012. The easing of the conflict from 2015 onwards heralded a turning point with a weaker recession.

Change in Syrian GDP between 2010 and 2018

Sources: United Nations Economic and Social Commission for Western Asia & Economic Research Forum

In 2018, GDP was estimated at $21.2 billion, a contraction of around 65% compared to 2010. By way of comparison, Lebanon’s GDP contracted by 70% during the civil war (1975-1990), Kuwait’s by 55% during the first Gulf War (1990-1991), and Iraq’s by 35% during the US military intervention in 2003. In 2018, the lack of significant investment in reconstruction and the regime’s reconquest of territories heavily affected by the war are two explanations for the more sustained decline in GDP compared to previous years.

Data for 2019 is not yet available, but with economic sanctions still in place and a significant part of the territory beyond Damascus’s control, it is highly likely that GDP will remain in recession.

Trade profoundly disrupted

In 2010, Syria exported USD 8.7 billion worth of goods and services abroad and imported USD 18.8 billion. Due to the low added value of its industry, the country’s trade balance was in deficit in the years leading up to the civil war.

In 2017, exports amounted to only USD 0.8 billion, while imports, after reaching a low of USD 4.8 billion in 2016, rose again to USD 6.1 billion the following year. As a result, the trade deficit as a percentage of GDP rose from 16.6% in 2010 to 37.3% in 2017.

US and European sanctions on various economic sectors explain the sharp deterioration in the trade balance. The following section analyzes key economic sectors with an estimate of the losses caused by the civil war.

2. Key economic sectors severely disrupted by the civil war.

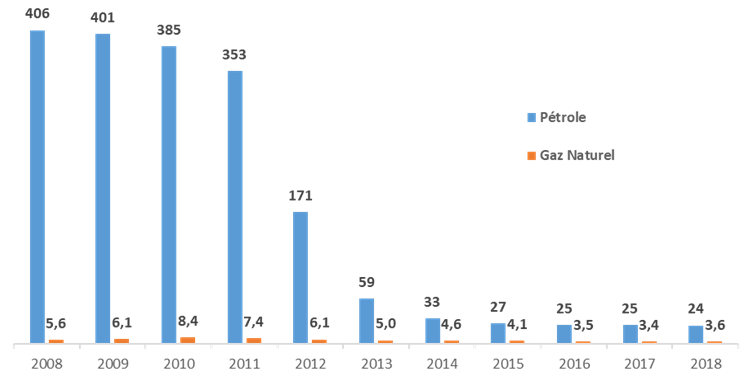

The oil and gas industry: sluggish production hindering reconstruction

Oil and gas production has been severely affected by the civil war. The Syrian Petroleum Company, a nationalized industry, holds a monopoly on extraction in the country and, prior to the conflict, controlled approximately 55% of production. Foreign companies, which account for the remaining 45%, must operate under the supervision of the SPC. With proven reserves of 2.5 billion barrels, Syria ranks 31st in the world.

However, most of the main oil wells fell into the hands of rebel groups in the first year of the revolution, which explains the sharp drop in production from 353,000 barrels per day in 2011 to 171,000 b/d in 2012. With the advance of Islamic State from 2014 onwards and the recapture of the main oil fields by the Syrian Democratic Forces (Kurdish militias), most of the production still eludes the Damascus regime, which will have to cope with reduced oil revenues to finance the reconstruction effort. Between 2011 and 2018, the government lost approximately 252 million barrels of production, which fell into the hands of various rebel groups and was sold on the black market. This loss of production represents an estimated shortfall of 2.623 trillion Syrian pounds for the authorities.

Current oil production, at around 24,000 b/d, meets approximately 25% of domestic needs. This delicate situation, combined with the embargo on Syrian oil that has been in place since the beginning of the conflict, is forcing the government to import oil to meet domestic demand. A return to pre-civil war production levels is unlikely in the short to medium term due to the deterioration of facilities (oil wells and pipelines) and the loss of refining capacity. The theoretical maximum capacity is 230,000 barrels per day, but the lack of infrastructure maintenance during the conflict, combined with the partial destruction of the Homs refinery, has reduced production by 50% since 2011.

The Syrian authorities are attempting to accelerate the development of natural gas, with the aim of using it to meet domestic demand and reserving oil for export. This strategy, initiated in the early 2000s, was brutally interrupted by the civil war. Natural gas production reached a low point in 2017, with output of 3.4 billion cubic meters, a figure that has stabilized since then. Despite the civil war, the main gas fields have remained under Damascus’s control, which explains why the decline in natural gas has been less severe than that of oil. This resource is expected to be a key element in the reconstruction process, with proven reserves of 300 billion cubic meters in 2018. However, the impact of the development of this industry will be limited, given the current embargo on Syrian hydrocarbons and the lack of infrastructure to facilitate exports.

Syrian oil production (in thousands of barrels per day) and natural gas production (in billions of cubic meters)

Source: British Petroleum Statistics 2019

The current sanctions on Syrian hydrocarbon exports mean that a rapid recovery of this economic activity is unlikely, and it will remain for internal use only for some time to come. It is important to remember that the European market accounts for around 95% of Syrian oil exports. To date, the Syrian authorities are focusing their efforts on restoring production to a level that can meet domestic demand. Furthermore, reserves, which have been declining for several years, will not be able to sustain production at pre-civil war levels in the long term.

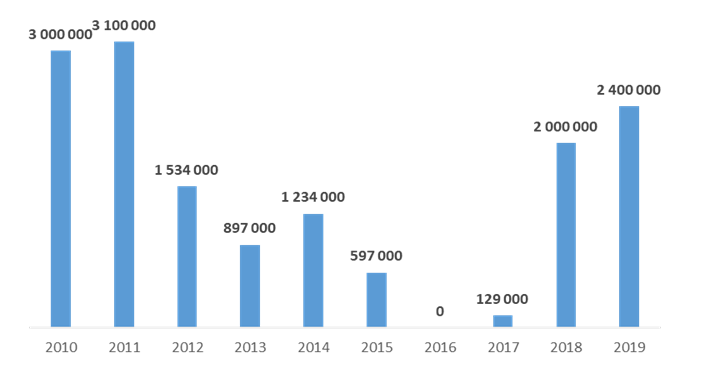

The mining sector: a promising industry on the rise

In addition to being a major producer of hydrocarbons, Syria has a wealth of minerals in its subsoil (chromium, manganese, gypsum, iron ore, marble, rock salt, asphalt, etc.), although the exact quantities that can be exploited are unknown. Phosphate mining accounts for a major part of the country’s mining industry, with 1,800 billion tons in proven reserves, or 3% of global reserves.

It is one of the mineral resources most affected by the civil war, with exports collapsing to near zero in 2016. Mining facilities alone account for 16% of all physical destruction related to the war. In fact, almost all production sites fell into the hands of ISIS before being recaptured by the Damascus regime. Exports are now on the rise again, with 328,000 tons exported in 2017 and 426,000 tons in 2018. However, these figures should be put into perspective, as the resource is still subject to European Union sanctions. Only Greece seems to have circumvented them and now imports around 17,000 tons of phosphate per month from Syria (compared to 5,000 tons in 2017). In terms of production, the sector has regained two-thirds of its pre-civil war capacity, and the authorities aim to reach 5 million tons by the end of 2020.

Phosphate production in tons

Sources: United States Geological Survey & CRU Commodities & Syrian Central Bureau of Statistics

The rapid recovery in production is mainly due to the quality of Syrian phosphate, which is among the purest in the world. As a result, Russian and Iranian investors have revived the country’s main mines. However, the Syrian industry’s limited capacity to process phosphate locally, the deterioration of transport infrastructure caused by the civil war, and the sanctions imposed by the European Union on this resource are likely to affect the sector, which will struggle to achieve export levels similar to those seen before the conflict in the short to medium term.

To date, there is no economic plan to revitalize the rest of the mining sector. The recovery of this sector will depend on the lifting of European Union sanctions and foreign investment, which is still timid and comes mainly from Russia and Iran.

Tourism, an economic sector that has virtually disappeared

Before the civil war began, tourism accounted for 12% of GDP and generated $3 billion in revenue for the government. With a peak of 9.5 million visitors in 2011, this activity came to a sudden halt as soon as the first events unfolded. Between 2011 and 2016, revenue generated by this sector fell by 94%, representing an estimated USD 130 million per year for the government at present.

Throughout the conflict, of the 10,000 sites identified in the country, around 300 were damaged or destroyed. The resumption of tourism depends on the renovation of many sites, some of which are no longer controlled by the government. The cost of damage to tourist sites is estimated at over $3.4 billion for the period 2011-2017.

According to the latest data published by the Syrian Ministry of Tourism, 1.3 million tourists returned to the country in 2017 and 2 million in 2018. However, these figures should be viewed with caution, as the vast majority of these tourists come from neighboring countries for short stays (around 88%).

The Syrian authorities have published the number of entries into the country between 2013 and 2017, but the exact revenue generated by this tourist activity is unknown. The number of international tourist arrivals rose from 51,635 in 2013 to 141,960 in 2017, showing steady growth. However, it is difficult to confirm these figures, as the Damascus regime is aiming to revitalize the country’s economy by banking on a rapid return of tourists.

The recovery of this sector of the economy depends on the pacification of the entire territory and costly investments to rebuild damaged or destroyed sites. It will undoubtedly take several decades for Syria to become an important tourist destination again.

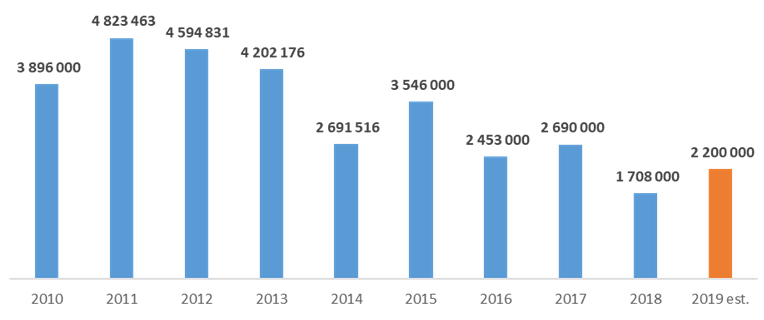

A disrupted agricultural sector threatening food security

The displacement of millions of people, the armed conflict depriving farms of labor, and the destruction of irrigation and transport infrastructure have had a major impact on agricultural production. In 2020, the Food and Agriculture Organization of the United Nations estimates that 7.9 million Syrians are food insecure and 1.9 million are on the brink of becoming so. In 2018, Syrian cereal production was the lowest in 30 years, with 1.7 million tons produced. Total losses in the sector were estimated at $16 billion between 2011 and 2016.

However, since the beginning of the conflict, agriculture’s share of GDP has varied little. It is currently estimated at around 26% of GDP, although the exact contribution is not known. This does not prevent cereal production from having fallen by around 44% between 2011 and 2019. While production performed well in the early years of the conflict, it has deteriorated since 2014 due to the rapid advance of ISIS, which deliberately pursued a scorched earth policy.

Cereal production in Syria (in tons)

Sources: Food and Agriculture Organization of the United Nations & Syrian Central Bureau of Statistics

The composition of Syrian cereal production changed during the conflict. While wheat accounted for 80% of production in 2011, this percentage fell to 70% in 2019, in favor of barley and corn, which require less water. In 2019, although the data are only estimates at this stage, the situation shows a slight improvement with an increase in the area of cultivated land in the country and better management of water resources. However, this is still insufficient to curb food insecurity, and a sustainable recovery of Syrian agriculture will require heavy investment in irrigation infrastructure and optimization of water resource use.

The case of cotton production

The case of cotton is also interesting to explore. Before the civil war, Syria was a major producer, with resources used by the local textile industry. From 212,000 tons in 2011, production subsequently declined to around 17,000 tons in 2018.

Production declined from the first year of the conflict, with a particularly sharp decline between 2014 and 2015. The Islamic State seized the vast majority of resources to resell them on the black market and circumvent the embargo on raw materials. Exports by the Damascus regime, meanwhile, fluctuated sharply, rising from 2,000 tons in 2010 to 50,000 tons in 2013, before falling again to 3,000 tons in 2019. The increase in exports during the conflict can be explained by the shutdown of the textile industry, forcing the authorities to export most of the raw cotton production.

Although cotton production can resume quickly, it is estimated that 70% of industrial textile facilities were destroyed during the conflict. In fact, a rapid revival of this industrial sector seems unlikely, as these facilities require significant investment to resume production. The issue of water, which has now become central, combined with the destruction of production infrastructure, suggests that neither cotton nor the textile industry will return to being key sectors of the economy. Focusing water resources on food production, while limiting waste, seems to be the best way to avert the risk of food insecurity.

3. Economic recovery dependent on foreign investment

Key partnerships with Russia and Iran

At the end of 2017, the UN estimated the total cost of rebuilding the country at $250 billion, a figure that has probably increased further today. With government revenues estimated at $1 billion in 2017, the Syrian government does not have sufficient resources to finance reconstruction. To achieve this, the Damascus regime could rely on remittances from the diaspora living abroad (around 5.6 million Syrians have fled the country since 2011, representing more than 26% of the 2010 population). However, the various estimates on this subject range from USD 1 to 2 billion per year, which is far from enough to quickly revitalize an economy devastated by conflict.

It will therefore be necessary to rely on foreign investment, particularly from Russia and Iran. In 2015, Russian financial aid to the regime was estimated at $1.6 billion (excluding the cost of the Russian military intervention), without knowing precisely how much was allocated to each economic sector. At the end of 2019, the Russian government also announced an investment of USD 500 million over the next four years for the port of Tartus. The aim is to turn it into an industrial center that will help revive the country’s economy.

Since 2013, Tehran has granted three generous lines of credit totaling $6.6 billion. However, it is difficult to accurately estimate Iranian investments in Syria.

China is also showing interest in the country as part of its New Silk Roads initiative. The Chinese authorities are planning to provide USD 23 billion in aid to the North Africa and Middle East region, although there is uncertainty about the exact amount that will be allocated to Damascus. Chinese private investment is estimated at $2 billion, but the industries involved are unknown. However, at this stage, these are only announcements and no investment has yet taken place.

The outlook is not promising, despite the country’s assets.

At this stage, while Bashar Al Assad’s regime appears to be clinging to power, ethnic tensions exacerbated by the conflict are undermining sustainable political reconstruction. Without political stability, it is difficult to envisage a major economic recovery.

The reconstruction of thermal power plants is a priority for the Damascus regime for two reasons:

– Businesses and individuals consume electricity all year round, which allows the government to generate stable revenues.

– The government can increase its foreign exchange reserves by selling electricity to neighboring countries.

In fact, agreements have been signed with Russia and Iran to recommission Syrian thermal power plants through technology transfer and financial aid. In 2018, the Syrian government also signed an agreement with Lebanon to export 100 MW of electricity each year for an estimated annual income of $266 million.

Although encouraging, this initial result is still insufficient to restore the rest of the economy. The main transport routes are still either damaged or destroyed. The government will first need to improve its diplomatic relations with its neighbors, particularly Turkey, to encourage them to invest in the country. Reopening and securing the borders is the first objective in order to allow trade to resume.

Matrice FFMO (Forces, Faiblesse, Opportunités, Menaces) de l’économie syrienne

Sources: Various press articles

Sources: Various press articles

Conclusion

The Syrian economy, heavily impacted by the civil war, shows no signs of a lasting recovery. The massive destruction of essential infrastructure and the reluctance of foreign investors due to ongoing political instability do not bode well for a sustainable economic recovery for at least another decade. Without an international political solution, the sanctions in place will remain in force and foreign investment will remain marginal and focused on a few strategic sectors, undermining any potential diversification of the economy.

Recent successes (electricity sales to Lebanon and Russian investment in the mining industry) are encouraging but still insufficient. A national plan to rebuild transport infrastructure (roads, railways, airports, ports, etc.) could be a first step, enabling better delivery of essential goods (particularly food).

BIBLIOGRAPHY

CHATHAM House, Russia and Iran: Economic Influence in Syria 2019: https://www.chathamhouse.org/publication/russia-and-iran-economic-influence-syria

Economic Research Center, Scenario-Based Forecast for Post-Conflict Growth in Syria 2020: https://erf.org.eg/publications/scenario-based-forecast-for-post-conflicts-growth-in-syria/

Syria Intelligence, Industry & Military Maps: https://www.syriaintel.com/category/economie-business/

University of Avignon, Tourism in Syria, Past, Present, Future: Between Resilience and Reinvention, 2018: https://tel.archives-ouvertes.fr/tel-01938543/file/pdf2star-1543414735-These–Zeid-A-KASSOUHA.pdf

Senate, Senate Report on Syria at a Crossroads, 2002: https://www.senat.fr/ga/ga44/ga44.html

World Food Program, Syria Food Security Analysis, 2020: https://www.wfp.org/publications/syria-food-security-analysis-march-2020

Food & Agriculture Organization of the United Nations, Syria Humanitarian Response Plan 2020: http://www.fao.org/3/ca7806en/CA7806EN.pdf

Food & Agriculture Organization of the United Nations, FAOSTAThttp://www.fao.org/faostat/en/#data

UNESCWA, Economic & Social Commission for Western Asia, Datahttps://data.unescwa.org/portal/32afeb40-1c3c-4b95-acab-061c5470bdc4

World Bank, The Toll of War: The Economic and Social Consequences of the Conflict in Syria, 2017 https://openknowledge.worldbank.org/handle/10986/27541

British Petroleum, Statistics 2019, https://www.bp.com/content/dam/bp/business-sites/en/global/corporate/xlsx/energy-economics/statistical-review/bp-stats-review-2019-all-data.xlsx

USGS, United States Geological Survey, Phosphate Data 2019 https://www.usgs.gov/centers/nmic/phosphate-rock-statistics-and-information

CRU Commodities, Market Analysis Phosphate 2019, https://www.crugroup.com/analysis/