Usefulness of the article: Public debt has risen sharply since the financial crisis, causing some concern despite very low interest rates (close to 0). This article aims to summarize the costs and benefits of increasing public debt, as recently outlined by economist Olivier Blanchard in his presidential address to the American Economic Association.

Summary:

- Public debt has risen sharply since the 2008 financial crisis in developed countries.

- In a context of low interest rates, it currently remains sustainable;

- The cost of crowding out private investment exceeds the benefits of public debt, but the total cost remains moderate.

- The risks are greater in small economies or in a monetary union, but the economic arguments for rapid fiscal consolidation are limited.

The recent communication by economist Olivier Blanchard[i] to the American Economic Association has reignited the debate on the increase in public debt observed since the 2008 financial crisis. The increase has been around 40 points of GDP in the United States since 2007, 30 points of GDP in France, and more than 60 points in Japan (see Figure 1). These developments may legitimately cause some concern. Will these debts be « sustainable » and will they not represent an excessive burden for future generations? However, at the same time, the interest burden on debt has remained at the same level in the United States and has even decreased in Japan and France (see Figure 2). How can this paradox be explained?

The rise in public debt has occurred in a context of historically low interest rates. These rates are lower than the rate of economic growth. We are in a world where r<g, where r is the nominal interest rate[ii] on public debt and g is the nominal growth rate, both rates referring to average values for a given country. This observation led Olivier Blanchard to reassess the costs and benefits of increasing public debt. What are the benefits and costs for a developed economy that is relatively insensitive to external shocks, such as the United States? What lessons can be learned for smaller developed economies or for the Eurozone?

I. Public debt: sustainable and potentially beneficial if r<g

Why is a negative spread between the interest rate and the growth rate important for public debt? One reason is that public debt is more likely to be sustainable in this scenario. Let’s take a simple example: suppose that the primary public deficit (before interest) is 0% and that public debt represents 100% of GDP. How will the public debt-to-GDP ratio evolve? The numerator will grow at the same rate as the interest rate, while the denominator will increase at the same rate as the growth rate. If the interest rate on public debt is lower than the growth rate, the numerator will increase more slowly than the denominator. The public debt-to-GDP ratio will gradually decline. It is fairly easy to generalize the reasoning and show that if the interest rate is lower than the growth rate, then over the long term, public debt does not explode but converges toward a stable debt level for any given level of constant primary deficit. A positive gap between the growth rate and the interest rate ensures the long-term sustainability of the debt. This explains, for example, why Japan pays such low interest charges despite having public debt exceeding 200% of GDP.

Public debt is not only sustainable, but can also be socially beneficial in certain respects. The idea was formalized by Nobel Prize-winning economist Peter Diamond in 1965 in his article « National Debt in a Neoclassical Growth Model. « Savings allow economic agents to transfer their income from the present to the future. However, if private investment is insufficient to absorb these savings, households and businesses cannot accumulate enough capital to, for example, maintain their standard of living once they retire or during periods of unemployment. Public debt then constitutes an alternative investment that allows these transfers of income from the present to the future. In this scenario, an increase in public debt will have a positive effect on the « well-being » of economic agents. It can be shown that, here too, this effect only exists if the interest rate on government bonds is lower than the growth rate. The effect is greater when the difference between the two rates is higher. Public debt can also be beneficial if it is used to finance public investments with a high social return (such as education or basic research). When interest rates are low, more public investment projects have a social return that exceeds the cost of borrowing, which may also justify an increase in public debt.

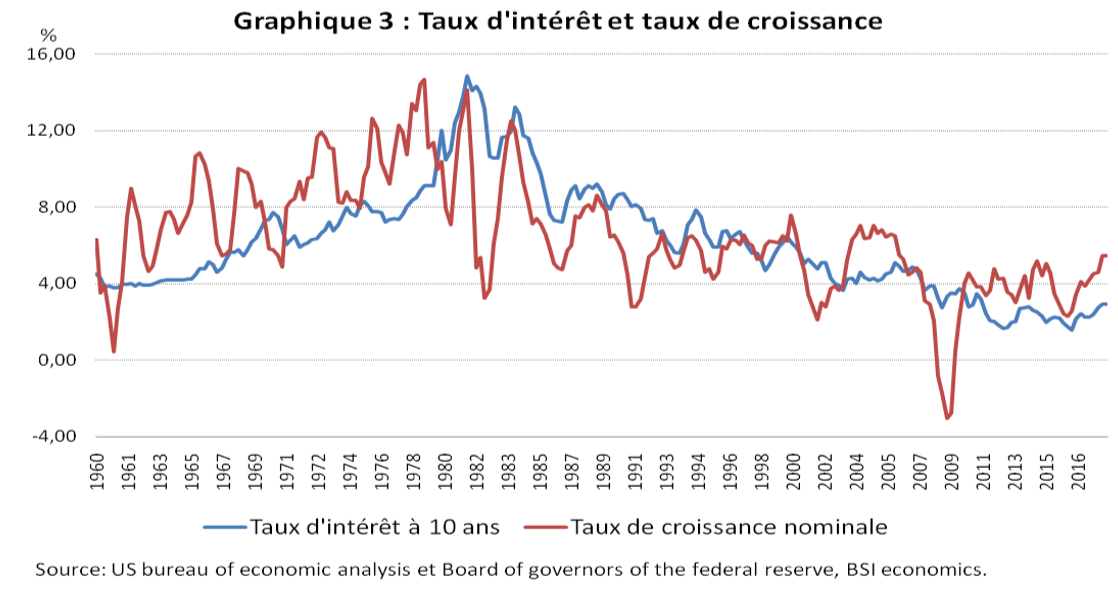

However, there is one objection to this reasoning. The current low interest rates may be a temporary consequence of the 2008 financial crisis and the monetary policies implemented in its wake. They could gradually return to values closer to their historical average and thus exceed the growth rate. The problem with this argument is that, over the long term, an interest rate on public debt that is lower than the growth rate is the norm rather than the exception. Figure 3 shows the 10-year interest rate on US federal debt and the nominal growth rate of the US economy. The latter was higher than the former during the 1960s and 1970s and since 2000. The interest rate was significantly higher only in the 1980s (see also Jorda et al. 2017 for an analysis since 1870). This result is all the more interesting given that 10-year rates may overestimate the cost of borrowing for the US government. Some government bonds are issued with shorter maturities, for which interest rates are lower. Olivier Blanchard constructs an adjusted interest rate that takes into account the different maturities. The growth rate is very rarely lower than this adjusted rate, even during the 1980s and 1990s (see Fig. 4). This phenomenon does not seem to be specific to the United States. Barrett (2018) estimates that the long-term gap[x] between the interest rate and the growth rate is negative not only for the United States but also for Germany, France, and the United Kingdom.

II. The cost of public debt: crowding out private investment

Public debt can remain sustainable despite high levels in a low interest rate environment and may even have advantages. However, it always has a cost: that of crowding out private capital. In theory, strong demand for government financing increases the cost of capital for businesses and individuals. This leads them to reduce investments whose return has fallen below the cost of capital, resulting in a reduction in total investment. The negative impact of this crowding-out effect depends on the difference between the marginal return[xi] on private capital and the rate of economic growth. The higher this return, the greater the decline in output resulting from the reduction in investment. Historical data suggest that, unlike the interest rate on public debt, the return on private capital is higher than the rate of growth. Thus, the average return on capital, measured by the ratio of net operating surplus to non-financial corporate assets valued at replacement cost, has been stable at around 10% on average in the United States since the early 1980s, well above the growth rate of the economy. This gap would suggest that the negative impact of the crowding-out effect outweighs the potential benefits of public debt.

However, there is still considerable uncertainty surrounding this effect. Two factors may mitigate it. Financial frictions (e.g., maximum limits on private debt, or risk premiums on corporate bonds) may limit the response of private investment to an increase in interest rates caused by higher public debt. Second, measures of average capital returns may overestimate marginal capital returns if profits include monopoly or oligopoly rents. Some studies suggest that these rents have increased in the United States (see De Loecker and Eeckhout 2017, Gutierrez and Philippon 2016). Geerolf (2019) presents a related argument and suggests that a significant portion of profits remunerates land ownership rather than capital ownership. The stability of the ratio between corporate profits and assets could therefore mask a decline in the marginal return on capital, reducing the cost associated with crowding out private investment.

Taking into account the positive effect of intergenerational transfers and the negative effect of crowding out private investment, Blanchard simulates[xiv] the impact of public debt on welfare[xv]. An increase in public debt of around 15 points of GDP at time 0 generates an average decline in « well-being » of 1% after 100 years. Most simulations generate declines of between 0 and 2% in long-term welfare. The cost of public debt to future generations exceeds its benefits, but the overall effect remains moderate. This result is sensitive to the assumptions used, but there is little evidence to suggest that the cost will be high.

III. What lessons can be learned for economies that are more sensitive to external shocks?

Olivier Blanchard’s argument is developed within the theoretical framework of a closed economy, without financial or trade exchanges with the outside world. This approximation may seem relevant for a large economy that is relatively insensitive to external shocks, such as the United States. But is it valid for a small open economy or for countries participating in a monetary union such as those in the eurozone? It is difficult to say. Certain specific factors can increase the cost of public debt.

In economies that are smaller than the United States and more vulnerable to capital movements, the increase in public spending can interact with exchange rate dynamics. Indeed, there is a risk that investors, concerned about the dynamics of public debt, will simultaneously sell their government bonds denominated in domestic currency, causing an attack on the exchange rate. The recent difficulties in the Argentine economy provide an example of a currency crisis, caused in particular by the accumulation of primary deficits.

In a monetary union, a similar risk exists. Different countries are very sensitive to the risk of investor coordination on what economists call a « bad » equilibrium: investors anticipate difficulties in repaying the debts of certain countries, demand high risk premiums, which increases interest rates, weighing down the debt burden and effectively fueling the risk of sovereign default. In theory, a central bank has the ability to intervene to prevent this type of attack. In a monetary union, such interventions pose significant problems. They require the central bank to distinguish between « liquidity » crises caused by coordination on a bad equilibrium and genuine solvency crises caused by an explosive debt trajectory in one of the countries participating in the monetary union. An overly broad definition of liquidity crises may encourage governments to implement overly lax fiscal policies, which can lead to inflationary pressures within the zone. An overly restrictive definition makes public debt vulnerable to speculative attacks, which can weaken the financial systems of member countries and lead to a risk of redenomination. One solution is to avoid accumulating public debt in the first place in order to prevent such attacks without resorting to central bank intervention or to avoid any ambiguity about the sustainability of the debt in the event of an attack. The risk then is a harmful « austerity » bias in times of economic crisis. It should also be noted that this risk of « speculative » attacks on public debt depends on the institutional specificities of each monetary union: mechanisms for fiscal solidarity between member countries, integration of financial systems, presence of a risk-free asset common to the entire zone in sufficient quantity, existence of a lender of last resort, etc.

Conclusion

The cost of public debt probably exceeds its benefits. However, in major economies such as the United States, and in a context of interest rates that are consistently lower than the rate of economic growth, this cost remains moderate and public debt as high as Japan’s can remain sustainable.

Other risks may emerge, particularly in economies vulnerable to rapid capital movements or in a monetary union. This suggests that fiscal consolidation, i.e., reducing public debt, is a legitimate economic policy objective. However, there would be no obvious gain from overly strong and rapid fiscal consolidation.

References

Abel, A., Mankiw, N., Summers, L., and Zechauser, R. (1989), « Assessing Dynamic Efficiency: Theory and Evidence, » Review of Economic Studies, 56, 1-20.

Barrett, P. (2018), « Interest-Growth Differentials and Debt Limits in Advanced Economies, » IMF Working Papers

Blanchard, O. (2018), « Public debt and low interest rates, » AEA presidential address

Diamond, P. (1965), « National debt in a neoclassical growth model, » American Economic Review, 55, 1126-1150.

De Loecker, J., and Eeckhout, J. (2017), « The Rise of Market Power and the Macroeconomic Implications, » NBER Working Papers 23687.

Geerolf, F. (2018), « Reassessing Dynamic Efficiency, » mimeo.

Gutiérrez, G., and Philippon, T. (2016), « Investment-less Growth: An Empirical Investigation, » NBER Working Papers 22897.

Jorda, O., Knoll, K., Kuvshinov, D., Schularick, M., and Taylor, A. (2017), « The rate of return on everything, 1870-2015, » NBER Working Papers 24112.

[i], professor at MIT, former chief economist at the International Monetary Fund, and former president of the American Economic Association,

[ii] As opposed to the real interest rate, which is equal to the nominal interest rate minus the inflation rate.

[iii] The reasoning works using the nominal interest rate and the nominal growth rate or, alternatively, using the real interest rate and real growth rate (minus inflation).

[iv]The result is valid in a certain environment with values of r and g and a constant primary deficit. The public debt-to-GDP ratio then follows a convergent arithmetic-geometric sequence. The result is no longer automatic if the interest rate, growth rate, and primary surplus are random variables, but their volatility does not appear to be strong enough to call into question the validity of the result (see Blanchard’s analysis on this issue). The correlation between periods of primary deficit and low interest rates would rather argue for a broader convergence domain. The analysis does not take into account the effects of economic openness and the possibility of multiple equilibria.

[v] This does not rule out temporary increases in public debt due to large primary deficits in situations where debt is initially low.

[vi] Such reasoning is not a priori valid in economies with a developed pay-as-you-go pension system and unemployment insurance. By providing replacement income, these theoretically limit the need for precautionary savings or savings for retirement. Public debt and a pay-as-you-go pension system function as substitutes in these models. In practice, however, observed savings rates are not systematically lower in this type of economy.

[vii]Well-being here refers to the « utility » of a given generation.

[viii] More specifically, the « risk-free » interest rate, generally equated with government bond rates.

[ix] Blanchard also takes into account the taxation of interest. Some US government bonds are held by US residents and are therefore taxed, which reduces the interest burden actually paid by the federal government.

[x]Barrett posits the existence of a stable long-term gap between growth rates and interest rates.

[xi]The additional output generated by an additional unit of capital.

[xii] Net operating surplus corresponds to the operating profits of companies before provisions, interest, and taxes for financial companies. It is equal to gross operating surplus minus depreciation (or, equivalently, minus capital depreciation).

[xiii] This question is directly related to the concept of dynamic inefficiency introduced by Diamond (1965). If the return on net capital after depreciation is lower than the growth rate, the economy is dynamically inefficient. Abel et al. (1989) systematically studied whether modern economies were dynamically inefficient and rejected this hypothesis. However, their results do not take into account the possible existence of rents.

[xiv]In a simple nested generations model where several generations coexist. These models differ from representative agent models in which all individuals are similar and have an infinite horizon.

[xv] Defined as in the previous section.

[xvi] Redenomination risk corresponds to the risk of a member state leaving the monetary union.