Abstract :

:

- A previous article showed how the STS (Simple, Transparent, Standardized) framework has made securitization safer since 2008. Despite this, the European market remains atrophied: €244.9 billion in 2024, 60% less than in 2008 and only 15.8% of the US market.

- The obstacles are structural. European insurers, penalized by Solvency II, allocate only 0.33% of their portfolios to securitization, compared with 17% in the United States. Legal and tax fragmentation creates barriers to entry for cross-border investors. The European bank-based model differs structurally from the US market-based model.

- Securitization could mobilize institutional savings (13 trillion in assets) and free up bank capital to meet the challenges of financing SMEs and the energy transition.

- Without reform of Solvency II and increased political coordination, the realistic scenario remains a moderate recovery (€400-500 billion by 2030), far from US volumes. The question is no longer whether the tool is safe, but whether Europe will be able to create the conditions for a truly functional market.

Download the PDF:the-return-of-securitization-in-europe-part-2.pdf

In our first article, we showed how the European regulatory framework has radically secured securitization since 2008, whether through the STS label, with its strict requirements for homogeneity, transparency, and risk retention, or the reform of the CRR (Capital Requirements Regulation), which drastically reduced capital requirements for senior tranches (from 100-250% to 10-25%).

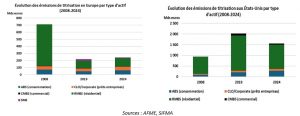

On paper, everything seems to be in place for a revival. However, six years after the introduction of the STS label, the European market remains atrophied: €244.9 billion in 2024, 60% less than in 2008 and only 15% of the US market (see charts above). This asymmetry cannot be explained by a lack of product security, as the STS framework has demonstrated, but by deep structural barriers that go far beyond regulation.

This second article analyzes the intrinsic limitations of the European model: why are institutional investors staying away despite the STS label? Why can’t Europe replicate the US model? And above all, what concrete economic needs does the revival of this market meet in the face of the massive challenges of financing the ecological transition?

Between market fragmentation, cultural reluctance on the part of investors, and transatlantic regulatory asymmetries, we will see that the real challenge is no longer to make securitization safe, but to create the conditions for a truly functional market.

1) The structural limitations of the European model

The creation of the STS (Simple, Transparent, Standardized) label was based on an implicit assumption: once products were secured and standardized, institutional demand would naturally recover. However, six years after its introduction, the European market remains modest.

This stagnation reveals a fundamental limitation beyond the lack of structural demand: the cumbersome European regulatory framework is hampering market development. Europe, which has never developed a real tradition of securitization, combines heavy regulatory constraints with deep structural obstacles. Several factors explain this situation.

1.1 Investment culture and risk aversion

European institutional investors, particularly insurers and pension funds, have a historically different investment culture from their US counterparts. The trauma of 2008 remains deeply ingrained in risk management practices, but it is above all the Solvency II prudential framework governing insurers that explains this divergence [1]. Solvency II imposes capital requirements (Solvency Capital Requirement) that heavily penalize assets perceived as complex or very illiquid, even when they are of high quality. Unlike the banking CRR (Capital Requirements Regulation), which introduced preferential weightings for STS securitisations, Solvency II does not provide for any equivalent favorable treatment: securitisations remain subject to high capital charges, whether they are STS or not. This regulatory asymmetry creates a major competitive disadvantage. Although the European Insurance and Occupational Pensions Authority (EIOPA) and several market players are calling for a revision in line with the CRR [2], these reforms are meeting with strong resistance from the most cautious regulators.

As a result, European life insurers allocate only 0.33% of their investment portfolios to securitization, compared with around 17% for their US counterparts [3]. European insurers overwhelmingly favor the highest-rated sovereign and corporate bonds (investment grade (IG)) to meet their solvency requirements. Securitization products, even those labeled STS, are still perceived as more complex and less liquid, which makes them less attractive despite often offering higher returns.

This reluctance can also be explained by the structure of demand. In the United States, institutional investors, pension funds, insurers, and asset managers account for the majority of securitization buyers, creating a deep and liquid market. In Europe, this pool of non-bank investors remains structurally weaker: European pension funds, which are less developed due to predominantly pay-as-you-go pension systems, manage significantly less assets than their US counterparts relative to GDP. This difference in demand explains why, even with secure products (STS label) and prudential incentives (rebalancing weights), the European market is struggling to reach critical mass.

Furthermore, national guarantee mechanisms, although useful for securing credit, can hinder securitization. In France, for example, real estate loans are often covered by mutual guarantee organizations such as Crédit Logement, which guarantee up to 100% of the loan amount. This near-total guarantee reduces the economic appeal of securitization for French banks: the regulatory capital cost of a guaranteed loan (20-35% weighting under Basel III) is lower than the economic cost of securitization, even STS. Banks therefore keep these loans on their balance sheets, depriving the market of a significant potential volume. This national specificity illustrates how local mechanisms create additional fragmentation.

1.2 Fragmentation of the European market

Unlike the United States, which has an integrated mortgage market with uniform standards (conforming loans), Europe suffers from persistent fragmentation. The legal, tax, and regulatory regimes for loans vary considerably from one Member State to another.

An investor purchasing a securitized Spanish mortgage product, for example, must be familiar with the legal framework for Spanish mortgages [5], local collection processes, and the macroeconomic specifics of the Iberian real estate market, as well as the potential political instability affecting housing assistance schemes (moratoriums, subsidized loans, foreclosure regulations). This complexity constitutes a significant barrier to entry and reduces the pool of potential investors, as evidenced by the high geographical concentration of issuances.

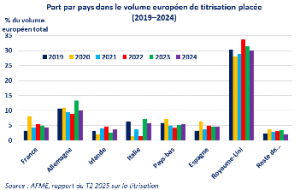

Data from the Association for Financial Markets in Europe (AFME) confirm that institutional demand is concentrated in a small number of jurisdictions. Between 2019 and 2024, the distribution of total European volume (see chart below) shows a market largely dominated by the United Kingdom (typically accounting for more than 30% of total volume) and that, apart from France and Germany, the significant percentages observed for markets such as the Netherlands and Ireland confirm a specialization of jurisdictions. Ireland serves as a hub for structuring cross-border transactions, while the Netherlands has a very mature domestic mortgage market. This concentration on a few established and specialized markets is evidence that investors do not view Europe as a homogeneous market.

1.3 Are prudential costs enough to boost demand?

Rebalancing risk weights makes securitization more attractive to issuing banks, but it does not seem to solve a fundamental problem: who buys these securities?

European banks remain the main holders of European securitization products. This situation reflects market developments since the 2000s: initially developed to optimize balance sheets under Basel II, European securitization has gradually transformed into a largely closed circuit where banks structure products that they trade mainly among themselves, creating barriers to entry for non-bank investors (technical complexity, lack of transparency, absence of standardization of practices).Many issues do not find buyers among external investors and remain on the balance sheet of the issuing bank, sometimes in the form of « retained securitization » used as collateral with the ECB, allowing for balance sheet relief without going through a sale. However, for third-party purchasing banks, acquiring securitization securities, even STS, ties up regulatory capital and automatically reduces lending capacity, which limits the economic interest of these transactions between banking institutions.

It is precisely for this reason that non-bank investors (insurers, pension funds, and asset managers) appear to be the natural target for these issues. They are not subject to the same regulatory capital constraints and can hold these assets to maturity without immediate liquidity pressure.

A recent study by the French Prudential Supervision Authority (ACPR) [6] confirms this dynamic: even in the event of a significant reduction in prudential costs, institutional demand elasticity remains low as long as liquidity and market fragmentation issues remain unresolved.

1.4 What is the realistic ceiling for the European market?

When comparing economic and financial structures, several indicators suggest that the European market will never be able to reach the proportions of the US market.

Europe remains deeply rooted in a system centered on banking intermediation, where bank loans dominate household and corporate financing, while the United States has developed a model more focused on capital markets. This difference is reflected in the figures for 2024, with bank loans accounting for around 80% of European corporate financing and almost all residential mortgage financing [7]. Conversely, only 20-30% of corporate financing is provided through bank credit, with the remainder coming from bond issues, securitization, and the equity market. Practices also differ, with refinancing being common in the US, while loans are often held to maturity by banks in Europe. The asymmetry between the US and European markets is not so much due to the absence of issuers as to the absence of structural buyers. In the US, the GSEs (Fannie Mae, Freddie Mac) [8] have certainly standardized the RMBS market, but it is above all the depth of the pool of institutional investors, with pension funds representing the majority of buyers, that explains the volumes. In Europe, pension funds manage significantly lower assets relative to GDP (pay-as-you-go pension systems), and insurers are penalized by Solvency II. This structural weakness in demand automatically limits the size of the market, regardless of existing guarantee mechanisms (Bpifrance, KfW, EIB), which mainly operate in the area of SME financing.

Finally, transatlantic regulatory asymmetry also helps to explain the development gap. Although the Basel III agreements are theoretically harmonized at the international level, their implementation differs. In the United States, prudential rules are applied with a degree of flexibility, particularly for regional banks (which are not subject to the full Basel III requirements). In Europe, supervision is significantly stricter: the EBA (European Banking Authority) imposes detailed guidelines, the ECB exercises close supervision via the Single Supervisory Mechanism (SSM), and European stress tests are considered to be more severe than their US equivalents.

While this regulatory rigor strengthens the European banking system, it also increases operational constraints and reduces the relative attractiveness of securitization. For example, the granular reporting requirements imposed by the ECB via the European DataWarehouse, while improving transparency, have increased the fixed costs of structuring, making small transactions economically unviable.

Under these conditions, even an optimistic scenario would only allow for partial convergence: the European market could reasonably reach €400-500 billion annually by 2030, double the 2024 figure, but still far below the relative size of the US market.

2) What need does the market recovery meet?

If the growth potential of the European market remains limited, the key question remains: why actively promote securitization? The answer lies largely in capital.

2.1 Freeing up bank capital for the green transition

The European banking system faces a major challenge: financing the ecological transition on a massive scale while maintaining the high capital ratios imposed by Basel III. European banks hold considerable loan portfolios, which tie up regulatory capital in proportion to their exposure to risk.

The Banque de France has estimated the investment needs for the ecological transition at €620 billion per year until 2030 [9]. These investments concern renewable energies, energy-efficient building renovation, transport electrification, and infrastructure adaptation.

Although European banks’ balance sheets would theoretically be infinite in size through the granting of credit (loans creating deposits according to the money creation mechanism), this capacity is constrained in practice by the regulatory capital requirements of Basel III. Capital ratios impose an effective ceiling on the growth of bank balance sheets; a bank cannot lend more without having regulatory capital to cover the risk-weighted assets. Securitization offers precisely such a mechanism for reallocating capital: by selling existing loan portfolios (particularly low-risk « mature » mortgages), banks free up capital that they can reallocate to new green loans (see this proposal by BSI Economics to the Finance Committee of the French National Assembly in 2018). This transaction does not necessarily transfer the commercial relationship that generates commissions, but only the risk associated with the assets (synthetic securitization, see definition in the first article).

This dynamic makes perfect sense with green securitizations, backed by environmentally-focused loans (energy renovation, electric vehicles, solar installations). The Commission has created the EU Green Bond Standard label, compatible with the STS framework, to channel responsible savings towards these instruments. Although marginal today (4 billion issued in 2024), projections anticipate an explosion to 300 billion annually by 2030 [10], making green securitizations a potential pillar of transition financing.

2.2 Diversifying sources of financing for the economy

Beyond bank capital, securitization would connect institutional savings to the real economy. European insurers and pension funds manage considerable assets, amounting to €13 trillion in 2025 [11], but invest heavily in sovereign bonds, which offer historically low returns.

Securitization products, when well structured and transparent, would offer an attractive alternative: indirect exposure to the real economy (SMEs, residential real estate, consumption), higher yields than sovereign bonds, and a risk profile potentially better correlated with insurers’ long-term liabilities. Senior STS tranches have spreads comparable to investment-grade corporate bonds with the same rating. For example, recent AAA tranches are priced at around 40-85 basis points above Euribor, depending on the structure, according to a market study published by Redbridge in 2024. [12]

However, this argument only holds if secondary market liquidity improves significantly. Institutional investors need to be able to adjust their positions without excessive friction, which requires market depth that is currently lacking.

2.3 Financing SMEs and underbanked segments

One particularly promising segment is SME securitization (securitization of loans to SMEs). European SMEs are heavily dependent on bank credit in the primary market and are often the first loans to be securitized when banks seek to transfer risk.

Securitizing SME loan portfolios would allow some of this risk to be transferred to specialized investors, while freeing up bank capital for new loans. However, this segment remains marginal: in 2024, SME issuances accounted for only €9.8 billion out of a total of €244.9 billion, or barely 4% of the European securitization market. This weakness can be explained by the inherently heterogeneous nature of SME loan portfolios, which complicates structuring and rating.

Article 20 of the European Securitization Regulation requires that underlying exposures be « homogeneous in asset type, » which poses a particular challenge for SME loans. While product homogeneity is relatively easy to achieve, risk homogeneity is much more difficult to guarantee: SMEs are highly heterogeneous in terms of sector, geography, size, and maturity. For example, how can we ensure that a portfolio combining a Parisian bakery, a German industrial SME, and a Spanish fintech start-up has a homogeneous risk profile?

This difficulty is amplified by the strict interpretation of the ECB and national supervisors, who examine the composition of SME portfolios with particular vigilance when granting the STS label. The limited granularity of certain portfolios increases the risk of concentration and complicates the modeling required for tranche rating.

Initiatives such as the European Investment Fund’s (EIF) InvestEU guarantee program aim to enhance the creditworthiness of certain tranches in order to attract institutional investors, but their impact remains limited at this stage for several reasons: the volumes guaranteed remain low (only a few billion euros per year); the administrative complexity of the guarantee process, as well as its cost, discourages many issuers, particularly medium-sized banks; the guarantee does not solve the problem of portfolio heterogeneity, which limits the ability to obtain the STS label.

2.4 Who really has an interest in the recovery?

There are many potential beneficiaries, but their interests converge unevenly. For banks, securitization enables the transition from an « originate to hold » model to an « originate to distribute » model [13], offering increased balance sheet flexibility and expanded lending capacity. Regulators see a double advantage in this: a tool for financial stability that allows risk to be transferred out of the banking system, and a mechanism for financing strategic priorities such as the ecological transition.

For end borrowers, greater bank lending capacity should theoretically translate into better credit terms, although this effect has yet to be demonstrated empirically. As for investors, they gain access to unlisted assets, and in particular to the financing of SMEs, but only if the risk-return ratio proves competitive compared to available alternatives.

The alignment of these interests is not automatic. The real question is whether the rebalancing of prudential costs and the ongoing strengthening of regulation with the integration of minimum safety levels will be enough to trigger a virtuous circle: more issuance would create more liquidity, attracting more investors, which in turn would allow for more issuance. Recent history suggests that this balance is difficult to achieve without a strong institutional catalyst, comparable to US government agencies that act as guarantors and standardizers of the market.

Conclusion

Six years after the introduction of the STS label, the conclusion is clear: regulatory security is not enough to revive the European securitization market. European insurers, penalized by Solvency II, remain structurally sidelined, while legal fragmentation discourages cross-border investors. Transatlantic regulatory asymmetry and the European bank-based model structurally limit convergence with the United States.

However, given the $620 billion needed annually for the ecological transition, securitization remains an indispensable but underutilized lever, particularly for green securitizations and SME financing.

Two scenarios are emerging: an optimistic convergence towards €400-500 billion by 2030, driven by a reform of Solvency II and increased political coordination; or a moderate recovery, concentrated geographically and sectorally, maintaining the gap with the United States. The second scenario seems more realistic in light of recent history: the market will remain a tool for regulatory optimization for large banks rather than a genuine mechanism for financing the real economy on a continental scale.

The question is no longer whether securitization can be safe, as the STS framework has demonstrated. It is whether Europe is ready to create the political, regulatory, and cultural conditions for a truly functional market. Without structural change, including ambitious reform of Solvency II and increased coordination between Member States, securitization will remain largely untapped potential in the face of the massive challenges of financing transitions.

Léo NICOLAU ( article written on December 23, 2025)

FOOTNOTES / SOURCES

[1] Solvency II imposes higher capital requirements for illiquid or complex assets, making securitization less attractive from a prudential perspective for European insurers, even for STS products.

[2] EIOPA (2021), « Opinion on the 2020 Review of Solvency II, » EIOPA-BoS-21/280; AFME & PCS (2023), « Unlocking Solvency II for securitization, » Position Paper; Insurance Europe (2022), « Position on Securitization under Solvency II. »

[3] Oliver Wyman, « How to Fix Europe’s Securitization Market, » March 2025.

[5] Concrete example: foreclosure times vary from 6-12 months in the Netherlands to 24-36 months in Italy, directly impacting recovery rates and therefore the valuation of securities.

[6], [9] ACPR and Banque de France, « Securitization for transition financing: the urgent need for a cross-cutting regulatory review, » 2025.

[7] IMF Global Debt Database Household debt, loans and debt securities (% of GDP);

Board of Governors of the Federal Reserve System, « Financial Accounts of the United States – Table B.101: Balance Sheet of Households and Nonprofit Organizations »; ECB, « MFI Balance Sheet Statistics, » December 2024.

[8] Fannie Mae and Freddie Mac guarantee approximately 70% of new US mortgage loans. These GSEs (Government-Sponsored Enterprises) purchase compliant loans from banks and issue guaranteed MBS, creating a standardized secondary market worth several trillion dollars. (Federal Housing Finance Agency)

[10] AFME (Association for Financial Markets in Europe), « Potential of Green Securitisation could exceed €300 billion annually by 2030, » 2022

[11] CEPS, « It’s Finally Time to Leverage Pension Funds to Foster EU Productivity and Benefit Pensioners, » 2025

[12] Redbridge Debt & Treasury Advisory, « Putting securitization to work for the energy transition, » 2024

[13] The « originate to hold » model refers to a banking practice in which institutions keep the loans they grant on their balance sheets until maturity. Conversely, the « originate to distribute » model is based on loans intended to be sold, particularly through securitization, allowing the partial transfer of risk to investors.

APPENDIX: COMPARATIVE TABLE EUROPE/UNITED STATES in 2024

| INDICATOR | EUROPE | UNITED STATES |

| Annual emissions (€ billion) | 244.9 | 1,548.4 |

| Securitization (as a % of GDP) | 1.08 | 5.7 |

| RMBS (% of total) | 49 | 74 |

| CMBS (% of total) | 1 | 3 |

| ABS (% of total) | 26 | 18 |

| CLO (% of total) | 20 | 5 |

| SME (% of total) | 4 | 0 |

| Outstanding bank loans (trillion €) | 13.5 | 11.5 |

Sources: AFME, Eurostat, ONS, BEA, FSO, SSB, European Banking Federation

Note: As European GDP figures are not officially provided, they have been approximated here as the sum of EU GDP and that of the other major economies, namely the United Kingdom, Switzerland, and Norway.