Summary:

· European private equity has experienced strong growth in parallel with European integration;

· Capital flows follow the logic of competitiveness and attractiveness, causing imbalances within the region;

· The development of European SMEs and SMIs and the resumption of growth will depend in particular on the willingness of national governments to develop their European and national financing;

· Brexit poses a threat to European private equity financing, and uncertainty over its terms is heightening concerns across financial markets.

On June 24, 2016, Europeans woke up to news that will go down in European history: the United Kingdom had voted in a referendum to leave the European Union. The UK Prime Minister resigned and, in the days that followed, the architects of Brexit left the political scene, leaving all Europeans in complete uncertainty as to the terms of such an unprecedented initiative.

The shock was immediate on the markets. Stock markets plummeted, and European shares lost more than 10% in less than two days of trading. Real estate was also impacted, and the effects of the Brexit announcement were quickly felt, particularly in the office property market. The City of London recorded a 6% drop in office values in July 2016, and one example of this is the reaction of La Défense in France, which launched a campaign called » Tired of the fog? Try the frogs » in an attempt to attract British investment to France’s main business district.

There are fears that this could have an impact on another market, namely private equity[1]. The British economy plays a key role in the European private equity landscape. It has established itself as the most mature market in Europe, accounting for more than 40% of investments made in 2015[2].

British private equity is the most attractive in Europe

Fundraising represents the ability of funds to invest in unlisted companies. The operation of private equity investment funds can be summarized in four phases:

1- Fundraising: the period during which investment funds collect funds from investors (institutional or individual);

2- Investment: During the first five to six years, the investment fund invests the capital raised by acquiring stakes in unlisted companies;

3- Divestment: Realization of capital gains or losses on investments and payment of the proceeds from disposals to investors;

4- Closure of the fund: in the case of mutual funds (FCP), the vehicle is closed once all holdings have been sold. This is referred to as the liquidation of the fund. It generally occurs 8 to 12 years after the fund is established.

Figure 1. Life cycle of a private equity investment fund

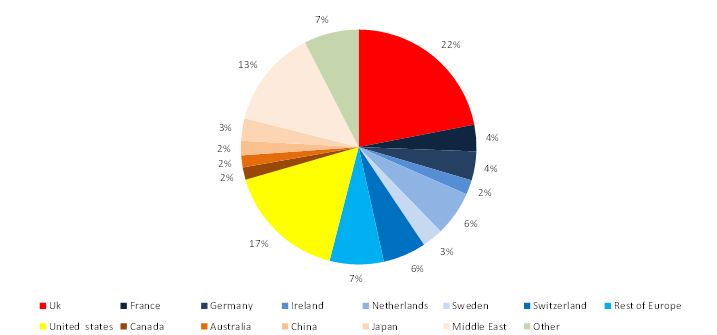

British private equity has raised nearly €220 billion since 2007, representing more than 50% of the amounts raised by all European funds. In addition to the maturity of the UK market, it is worth noting the ability of UK-based private equity funds to raise funds from international investors. In 2015, UK funds were able to attract investors from all over the world, as shown in the chart below:

Graph 2. Origin of funds raised by UK investment funds in 2015

Sources: BVCA, BSI Economics

Thus, 78% of the capital raised in 2015 by British funds came from abroad, including 32% from European countries (excluding the UK), 17% from the United States, and 13% from the Middle East. By way of comparison, French private equity raised 29% of its capital abroad over the same period, including 19% in Europe (excluding France) and 10% in the rest of the world. It should therefore be noted that 71% of the capital raised by French funds came from investors based in France.

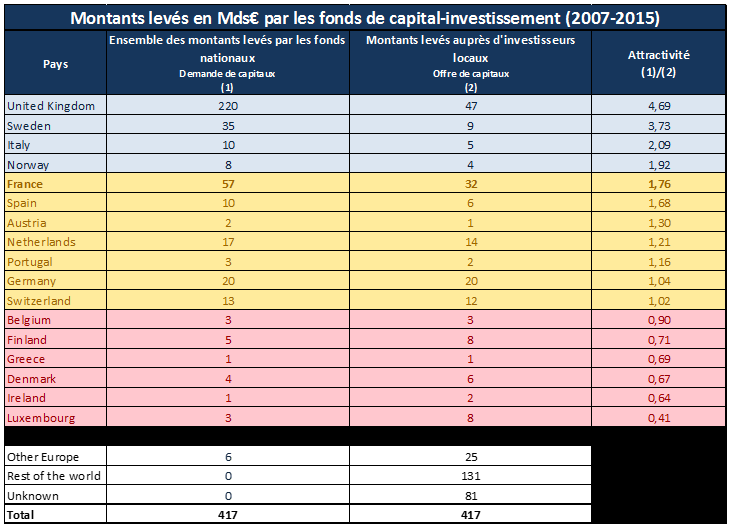

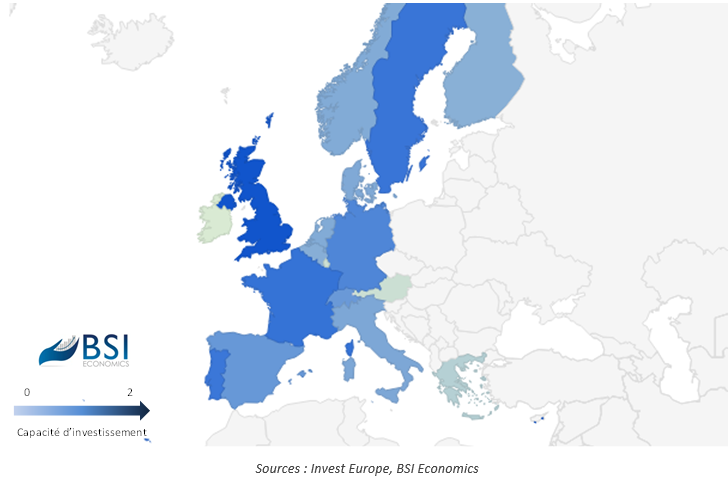

Of the €417 billion raised by European-based investment funds between 2017 and 2015, 60% came from European investors. However, the ability of financial centers to attract this capital varies from country to country. This requires investment funds capable of raising these funds. Let us define the concept of private equity attractiveness as the ratio between the amounts raised by national funds from national and international investors (which we will refer to as capital demand for simplicity) and the contributions of national investors to European private equity (which we will refer to as capital supply). This supply of capital can be seen as institutional investors’ appetite for private equity resulting from their portfolio asset allocation strategy. We performed this calculation for the period 2007-2015 and identified three categories of countries (see Table 1 below).

Table 1. Fundraising in Europe from 2007 to 2015

Sources: Invest Europe, Perep Analytics, BSI Economics

On the one hand, there are highly attractive countries, i.e., countries in which investment funds are able to attract foreign capital. It is noteworthy that the United Kingdom is the most attractive alongside Sweden.

France, the Netherlands, and Spain are among the relatively attractive countries, but they remain rather dependent on the appetite of domestic investors. Indeed, when we analyze in detail the origin of the capital raised in these countries, we see that, like France, Spain, Portugal, and the Netherlands raise most of their capital within their own borders. Therefore, the investment capacity of funds based in these countries depends on the health of domestic investors and their portfolio decisions.

Germany has raised capital equivalent to the capital invested by domestic investors. This can be explained by the type of investors, as Germany is characterized by the presence of banking players that finance companies with both debt and equity, and thus a low presence of investment funds independent of German banks. These are referred to as captive funds.

Finally, it is not surprising to find Ireland and Luxembourg, which appear to be providers of European capital. These countries have institutional investors for whom private equity is part of their portfolio diversification strategy. However, local demand is not sufficiently developed to meet these needs. As a result, this capital flows out of these countries en masse to other countries where the private equity market is more mature and where there are more investment opportunities.

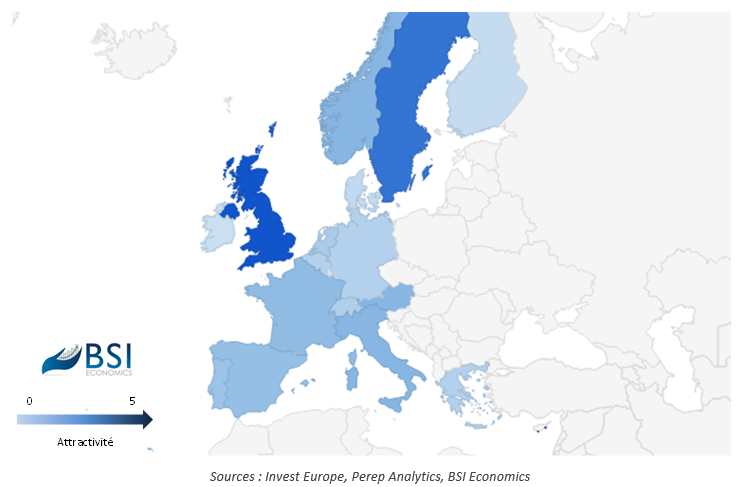

Figure 3. Attractiveness of funds in Europe

Fundraising represents the ability of investment funds to acquire stakes in the capital of unlisted companies in the medium/long term (between 1 and 12 years). In the case of UK private equity, the funds raised are denominated in pounds sterling. Movements in the foreign exchange market following Brexit are already impacting UK private equity by reducing its investment capacity in Europe. In addition, they may impact future fundraising as international institutional investors are exposed to currency risk.

British private equity is the only source of financing for companies in Europe

The capital raised is then invested in unlisted companies, in the form of venture capital, growth capital, and LBOs[4]. The latter account for the majority of private equity investments. Between 2007 and 2015, LBO investments accounted for an average of more than 70% of annual private equity investments.

Here again, British private equity has the characteristics of a major financial center with largely internationalized investment funds and the ability to invest in companies in Europe, but also in the United States. Forty-five percent of the amounts invested by British funds are invested in the United States. Thirty-five percent benefit the national ecosystem and 14% are destined for European companies.

By way of comparison, in 2015, French investment funds devoted 66% of their investments to French companies. Twenty-four percent of the amounts are invested in Europe and only 10% outside Europe.

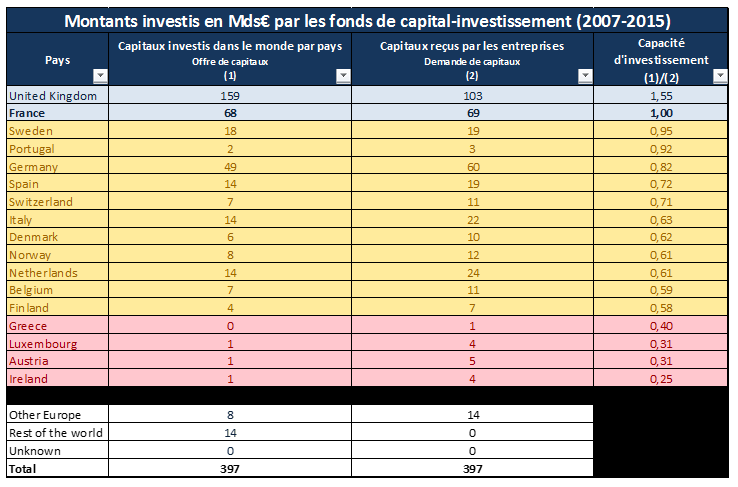

In light of these statistics, we propose to determine the investment capacity of private equity funds by country. We define the supply of capital for a given country as the capital invested by that country’s private equity funds worldwide, and the demand for capital as the sum of the amounts received by companies in that country. We define a country’s investment capacity as the ratio between the supply of capital from investment funds and the demand for capital from companies. We obtain the following results:

Table 2. Investments in Europe from 2007 to 2015

Sources: Invest Europe, Perep Analytics, BSI Economics

It can be seen that British investment funds are the only ones with an investment capacity strictly greater than 1. In other words, demand from companies based in the United Kingdom is not able to absorb the capital raised by national funds. This implies that British funds are internationalizing and taking advantage of investment opportunities in Europe and around the world. The financing of European companies therefore depends on the ability of British funds to invest outside their borders.

France is well positioned according to this indicator. The amounts received by companies are close to the amounts invested by national funds. In the event of a shock to the European private equity market, it is reasonable to assume that French companies would be able to find financing within the French private equity ecosystem.

Other European countries, on the other hand, appear to be somewhat dependent on the ability of foreign funds, particularly British funds, to invest in Europe. Indeed, domestic investors do not have sufficient resources to meet the investment demand of companies.

Figure 3.Investment capacity of private equity funds in Europe

Potential threats and opportunities of Brexit for the European private equity market

Brexit could therefore have a negative impact on the private equity market, mainly in the downstream segments (LBOs and growth capital). British funds are the main players in mega-deals in Europe, i.e., large-scale investments (generally exceeding €1 billion). This could affect company valuations and limit private investment in the largest companies in the European Union.

However, the UK’s potential withdrawal from European private equity could enable other European financial centers to attract the interest of institutional investors outside Europe in order to be able to make these investments. This could allow France to come out on top by asserting its position as the leader in continental Europe and continuing the internationalization of its investment funds. France can also count on a reorientation of the EIB’s (European Investment Bank) investment capacities towards continental Europe to develop. Nevertheless, the financing of companies in Europe will depend on the terms of Brexit, which are still uncertain.

Conclusion

Capital movements within the European Union are at the heart of the concerns generated by the UK’s Brexit referendum. The UK plays a central role in Europe’s private equity market. The British ecosystem is characterized by investment funds that are large enough to attract capital from around the world. As a result, they are less dependent on the appetite of domestic institutional investors and are able to attract capital from the US, the Middle East, and other European countries.

Capital raising reflects the medium/long-term investment capacity of funds. British funds are currently the only ones able to invest significantly outside their borders. Concerns about the terms of Brexit and its effect on capital movements from the United Kingdom are significant. France must assert its position as the leader in private equity in continental Europe and refocus its ecosystem in order to attract international capital and replace British funds. To do so, it will need to encourage the emergence of global private equity players.

[1] For more details on private equity, see Stéphane Dahmani’s article on BSI Economics: http://www.bsi-economics.org/675-le-capital-investissement-etat-des-lieux-en-france

[2] Investments made worldwide by British funds in 2015. Source: Invest Europe (formerly EVCA).

[3] A captive fund is an investment fund whose capital comes mainly from the parent company (bank, insurance company, etc.).

[4] Leverage Buy Out or capital transfer involves an investment fund acquiring a majority stake in mature companies by resorting to debt, corresponding to leverage.

[5] Annual average share of LBO in European private equity. Source: Invest Europe