Usefulness of the article : this note presents the challenges posed by the demonetization of the economy for monetary policy and how certain central banks are attempting to respond to them, notably Sweden’s Riksbank, which is in the process of introducing an electronic version of its currency, the e-krona.

Summary:

- While cash remains the dominant means of payment in advanced and emerging economies, numerous alternative means of payment and changing practices could ultimately reduce its use, as in the Swedish economy.

- Deminization should, in theory, enhance the effectiveness of monetary policy, particularly in a context of negative interest rates, although this does pose risks to the security of payment systems.

- In this context, a gradual transition, for example through an exchange rate between cash and deposits, as proposed by the IMF, and, in the long term, the introduction of an electronic currency, such as the Swedish e-krona, could address these challenges.

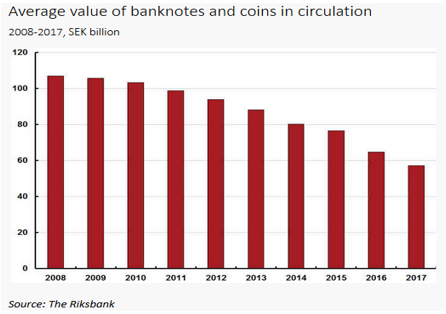

Sweden is on track to become the first economy in the world to do away with cash. The amount of cash in circulation there has fallen by almost 50% since 2007, with 36% of Swedes no longer using banknotes or coins on a daily basis. This revolution in practices is shaking up the Swedish economy. Demanding cash out of circulation offers significant opportunities in terms of combating crime, tax evasion, and corruption, but also and above all in terms of economic policy, particularly monetary policy.

More broadly, while cash remains a dominant means of payment in advanced economies, changing practices are likely to marginalize its use in the coming years. While demonetization offers significant advantages in a context of negative interest rates, it also poses risks to financial stability. According to several recent studies, notably by the IMF, a gradual transition to a digital central bank currency could limit these risks and establish the technical framework for the smooth functioning of payment systems in a cashless economy. The operational considerations currently underway at the Riksbank (Sweden’s central bank, the oldest in the world) regarding the introduction of an e-krona, the first digital central bank currency, are particularly promising in this regard.

Swedish krona: average value of coins and banknotes in circulation (SEK billion)

Cash remains the dominant form of payment in advanced economies, although structural trends are working towards its demonetization

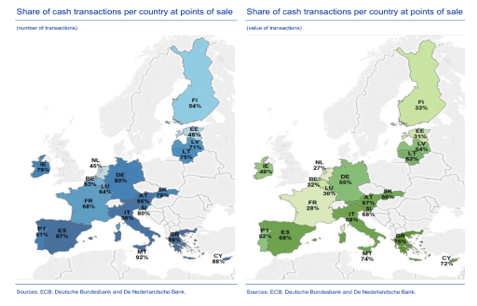

At present, cash remains the dominant means of payment in the eurozone, accounting for nearly 80% of point-of-sale transactions and 54% of their total value, according to a study by the ECB and the Eurosystem[1]. The demand for fiat money remains particularly strong (in 2017, the value of euro banknotes in circulation worldwide rose by 4% to EUR 1,170 billion, with coins rising by the same amount to EUR 28 billion). Cash (banknotes and coins) thus represents a significant share of the M1 monetary aggregate, a narrow component of the monetary base, which is an important steering instrument for central banks.

Outside the eurozone, its use is also growing in most advanced and emerging economies, according to a study by the Bank for International Settlements, which notes that cash in circulation increased by 7% to 9% of GDP between 2000 and 2018. There are disparities within this trend: the increase is particularly marked in Japan and Hong Kong (+7 and +9 percentage points of GDP respectively), but the share of cash in circulation fell by 5 percentage points of GDP in China over the same period, where a significant proportion of transactions are now carried out via WePay. The trend is less clear in the United States, where cash usage is declining only very slowly (cash accounted for 30% of payments in 2017, compared with 33% in 2015, according to the Federal Reserve Bank of San Francisco).

Overall, cash remains the dominant form of payment, but it is changing, facing competition from new payment methods (e-payments, card payments, e-wallets, etc.): the growing share of large denominations in advanced economies suggests, for example, that its main function is now as a store of value. Its use also reflects structural preferences that differ between economies. For example, thanks to the work of the Eurosystem, we can distinguish between different practices in the euro area, which can be summarized as follows: cash-centric economies such as the Mediterranean countries, Germany, and Austria, both in terms of the number of transactions (86% in Italy, 80% in Germany) and the value of these transactions (75% in Greece, 68% in Spain); and economies that favor other means of payment (contactless, electronic, etc.), both in terms of the number of transactions (45% in the Netherlands) and the volume of these transactions (28% in France, 33% in Finland, 32% in Belgium).

However, in the long term, as explained by Riskbank Governor Stefan Ingves[5], the consumption practices of younger generations (automated payments, online payments, contactless payments) are set to become major demographic trends, supported, for example, by the rollout of electronic payment solutions (e.g., USD 617 billion in cardless payments in 2016 in the United States vs. USD 60 billion in 2010, according to the Fed). These trends are contributing to the demonetization of advanced economies, as illustrated by the cases of Sweden and Norway, based on the need to ensure the reliability of the payment system.

Use of cash among the various member states of the eurozone (2017)

In theory, the demonetization of the economy promotes more effective transmission of monetary policy, especially in an environment of low or even negative interest rates, at the cost of risks to financial stability.

Deminization has significant consequences for economic policy, as noted in particular by economist K. Rogoff in his book The Curse of Cash (see video at this link) and in a recent 2017 IMF study[6]. While the impact is significant in terms of monetary policy, it is also considerable in other areas: in a 2014 study[7], the Bundesbank estimates that reducing processing costs would lead to a 2-3% gain in GDP in Germany. In terms of public finances, the aforementioned IMF study considers that the expansion of the tax base linked to demonetization, notably through the reduction of tax evasion and fraud, would increase budget revenues (by around €100 billion per year across the European Union (EU) according to an analysis based on European Commission data[8]). Furthermore, these potential tax revenues should more than offset the small losses in revenue indirectly linked to seigniorage[9]. Finally, demonetization could promote financial inclusion through the opening of a bank account, which would be de facto mandatory for the entire population, and reduce the negative ecological footprint of paper money (IMF, Wang, 2016).

However, the effects are more structural in monetary terms. At first glance, this obligation to have a bank account or an electronic wallet (since, without cash, only electronic money could fulfill the role of store of value) would lead to an increase in bank deposits. This increase could primarily favor bank financing, as well as the profitability of banking groups—deposits being a pillar of the banking transformation process—and, in theory, ultimately their ability to lend to the economy, which would strengthen the effectiveness of the bank credit channel in the transmission of monetary policy[10], although this approach is somewhat simplistic.

Furthermore, the absence of arbitrage between cash and electronic deposits would put an end to the liquidity trap situation in the face ofthe zero lower bound. In this situation, agents are neutral between deposits and currency, since the latter yields nothing (0% interest rate).As a result, the central bank is unable to control interest rates, as economic agents no longer react to increases in the monetary base. This situation is exacerbated in a context of negative interest rates, as is currently the case in the euro area (with the deposit facility rate at -0.50%).

And while their impact on the bank credit channel is criticized by some studies[11] given their potential negative effects on bank profitability, demonetization could restore the effectiveness of this channel. Indeed, the absence of cash would no longer allow economic agents to exchange their bank deposits for cash in order to escape potential negative interest rates on their demand accounts. These negative rates, which would effectively constitute a tax on bank deposits, would encourage economic agents to consume and invest rather than hold savings that are losing value, thereby stimulating consumption and investment and, consequently, demand and economic activity.

This controversial approach would have the merit of responding to the current difficulties of the European economy, namely over-savings in some economies and insufficiently dynamic domestic demand in others. It is advocated in particular by W. Buiter in a 2009 paper[12]which proposes going beyond thezero lower bound by eliminating cash and implicitly taxing money through the same mechanism. This would overcome the ECB’s limited conventional room for maneuver in the face of the ZLB or the » reversal rate, » the negative interest rate beyond which the aggregate effects on the economy would be negative.

Nevertheless, total demonetization presents risks in terms of access to the payment system but also in terms of financial stability, as summarized by the Riksbank in its preparatory work for its electronic currency project (e-krona, see elsewhere). The Riksbank considers that the absence of physical currency may threaten the viability of payment systems for several reasons. Firstly, the intermediation of value storage and money creation by private service providers with no link to the central bank (such as Facebook’s Libra—it should be noted that central bank money has zero credit and liquidity risk) could lead to risks of monopolization and therefore higher costs. In its 2018 annual report, the Swedish Consumer Association highlights the risks of exclusion from the financial system. In addition to the risks associated with money laundering and terrorist financing, the bankruptcy of a private currency provider could threaten the viability of payment systems. Finally, the deterioration of the central bank’s control over the money supply would undermine its ability to manage the economic cycle. This highlights the need to prepare for the transition or even introduce a digital central bank currency capable of ensuring the stability of payment systems, managing the economic cycle, and maintaining the institutional role that currency plays between a state and its citizens.

The risks of demonetization mean that we need to prepare for the transition to a cashless financial system, or evencreate adigitalcentral currency, various versions of which are already being studied by different central banks, particularly in Sweden, where the project is most advanced.

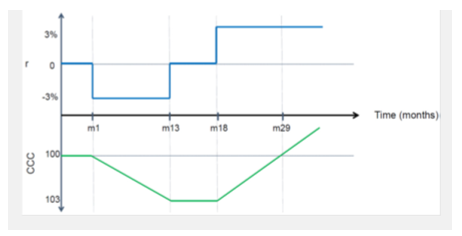

The IMF[13]reports on an operational proposal aimed at promoting a gradual transition to demonetization. The aim is to decouple cash (fiat currency) from central bank money (reserves, which pay interest, potentially negative) and to link the two via an exchange rate, which is itself controlled by the central bank in order to control the conversion of digital currency into cash.[14]In this way, an economic agent wishing to withdraw banknotes from an ATM would have to convert their deposits, valued in central bank money, into cash at the conversion rate specified by the central bank. Conversely, a cash deposit into their bank account would be valued in central bank money at the fixed conversion rate. As a result, an agent who deposits $100 in cash could be credited with a different amount in their bank account depending on the exchange rate.

In this way, a central bank wishing to apply negative rates to excess reserves (i.e., bank deposits with the central bank in excess of required reserves, as is the case in Japan, Switzerland, and the euro area) could, at the same time, penalize the conversion of these reserves into cash by controlling the conversion rate of cash into reserves. This mechanism is detailed in the numerical example provided by the IMF below, which takes the case of a negative interest rate of 3% on reserves (during the period m1 to m13 on the graph), accompanied by an increase in the cost of cash in terms of reserves via the exchange rate between these two currencies (in green). In effect, the negative interest rate policy is made more effective.

Exchange rate between cash and reserves in a negative interest rate environment

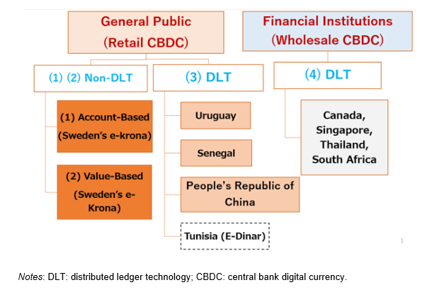

While this IMF proposal addresses the risks associated with the ineffectiveness of monetary policy in the short and medium term, it does not address the longer-term financial stability risks associated with demonetization. Following the example of Sweden, which will test a dematerialized version of its currency, the e-krona, at the end of 2019, it therefore also seems relevant to plan for the creation of an electronic central currency in order to guarantee the sustainability and resilience of payment systems in the event of financial tensions. In theory, digital central currencies can take several forms, as summarized in a document presented by Sayuri Shirai[14], a member of the Board of Directors of the Bank of Japan, which lists the various options currently being studied by central banks around the world:

- Offering the public the option of opening an account with the central bank, i.e., an account-based central e-currency: this would give citizens an account with their central bank and allow them to exchange central currency for electronic currency (in the event of a crisis);

- The central bank providing digital central bank money (de facto « prepaid ») on an electronic wallet ( » value-based « ), which would have the advantage of guaranteeing the anonymity of transactions below a certain amount (below EUR 250 according to the current anti-money laundering directive) but not that of the account holder;

- The use of blockchain technology to create a ledger on which citizens could deposit or withdraw central bank money. This option is particularly popular in less financialized and emerging economies (e-dinar in Tunisia, studied in China, Uruguay, Senegal, and Israel) where there is a stronger desire to move away from cash[16], dictated by its cost in terms of corruption but also by the desire to catch up with the technological frontier in the field of fintech. It guarantees the anonymity of transactions thanks to blockchain technology.

- Use of blockchain technology to create a ledger on which financial institutions could deposit or withdraw central bank money. This option is popular among advanced economies (Canada, Singapore), which rely on reliable payment systems and benefit from significant financialization;

Four major models of digital central bank currency (Sayuri Shirai)

In this regard, the Swedish central bank is studying the feasibility of the first two options and inviting the Swedish Parliament to consider the concept of legal tender in a demonetized economy. The e-krona, which is currently undergoing technical analysis by the Riksbank, could therefore take the form of an e-currency held at the central bank or a digital currency held in an electronic wallet. Both proposals would be based on a technical infrastructure managed by the Riksbank around a register that interfaces between end users (citizens via the internet, phones, cards, the internet of things, etc.) and payment service providers, as well as any organizations wishing to make payments in e-krona, and enabling the settlement and tracking of various transactions. The properties of these two options differ significantly due to current regulations (in particular the Anti-Money Laundering and E-money Directives); for example, it would not be possible to pay interest in the prepaid currency model, but transactions of less than EUR 250 would be anonymous.

Ongoing discussions in the Swedish Parliament and the progress of technical preparatory work within the Riksbank should provide more visibility on the design of this first digital central bank currency. The success of this major innovation in the world of payment systems, and the eventual reduction in cash in circulation in the eurozone, could even, if necessary, support the creation of a future e-euro, the first common digital central bank currency.

Conclusion

In short, demonetization presents significant challenges for central banks. If well prepared and supervised, it offers an opportunity to enhance the effectiveness of monetary policy in a context of negative interest rates. Given the risks to financial stability, the rollout of central bank digital currencies should help reduce the risks to payment systems. The Riksbank’s experiment is particularly exciting in this regard.

[1] ECB, The use of cash by households in the euro area, 2017

[2] Countries belonging to the Committee on Payments and Market Infrastructures

[3] BIS, Payments are a-changin’ but cash still rules, 2018

[4] https://www.frbsf.org/cash/publications/fed-notes/2018/november/2018-findings-from-the-diary-of-consumer-payment-choice/

[5] IMF, Finance and Development, June 2018

[6] IMF, WP, The macroeconomics of De-cashing, 2017

[7] Bundesbank, The usage, costs, and benefits of cash, 2014

[8]https://ec.europa.eu/taxation_customs/fight-against-tax-fraud-tax-evasion/a-huge-problem_endont, although the method is controversial

[9] Seigniorage measures the gain resulting from the difference between the face value of fiat currency and its production cost, as well as the gain relating to cash lending by the central bank

[10] NB. It should be noted that currency and deposits are part of the same monetary aggregate (M1), so a decline in demand for cash offset by an increase in demand for deposits would have no impact on the monetary base

[11] Molyneux, Reghezza, Thornton, Xie, Did negative interest rates improve bank lending?, 2019

[12] Negative nominal interest rates: three ways to overcome the zero lower bound, 2009

[13] IMF, WP, Monetary policy with negative interest rates: decoupling cash from electronic money, 2018

[14] This operational modality is understood in a context where the supply of central liquidity is abundant (e.g., the current fixed rate, full allotment model in force within the Eurosystem).

[15] Shirai, Central Bank Digital Currency: Concepts and Trends, 2019

[16] As argued in particular by J. Sachs