Usefulness of the article: This article discusses changes in monetary policy practices within central banks in advanced countries since the crisis, the limitations encountered, and the alternative monetary frameworks put forward to overcome these problems.

Summary :

- Despite the new instruments adopted since the financial crisis, central banks are struggling to achieve their inflation targets.

- The alternative monetary frameworks that have been put forward, such as « average inflation targeting » or higher inflation targets, seem complicated to implement, as they are based on overly optimistic assumptions about the adjustment of inflation expectations;

- Macroprudential measures are necessary to limit the risks of bubbles in a context of low interest rates—most often zero or negative.

- However, to preserve their credibility and independence, central banks will need to clarify the limits of their actions.

Ten years after the financial crisis, central banks in advanced economies are far from returning to their pre-crisis modus operandi. Interest rates remain close to historically low levels and their balance sheets are very large (see Chart 1). In addition, they have adopted new instruments, not only to guide monetary policy, but also to address financial stability concerns.

Despite this, central banks are struggling to meet their inflation targets. This raises the question of whether the tools available to central banks are still sufficient. If not, how will they respond to the next crisis? In addition, macroprudential supervision now gives them more power. It is in this context that central banks are rethinking their monetary framework.

Chart 1: The Fed and the ECB are operating with very high balance sheets

Sources: ECB, Federal Reserve, BSI Economics

Low inflation while interest rates are at rock bottom: should the monetary framework be changed?

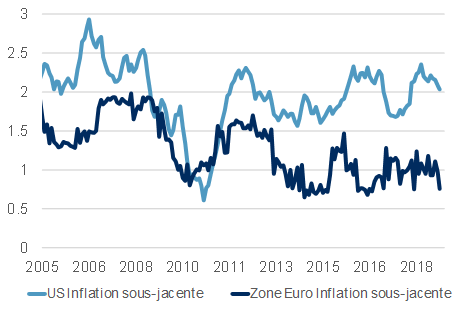

In response to the crisis, central banks have had to be creative and add new instruments to their arsenal. They have experimented with negative interest rates, injected liquidity directly into financial markets through monetary easing, and are now using forward guidance to reinforce their interest rate policy. Despite this, the return to potential growth has been slow, and central banks are still struggling to generate inflationary pressure to reach their inflation targets. Core inflation[1] is struggling to stabilize around the 2% target in the US and appears to be stuck at around 1% in the eurozone (see Chart 2).

Chart 2: Core inflation is far from the ECB’s target in the eurozone

Sources: ECB, Bureau of Labor Statistics, BSI Economics

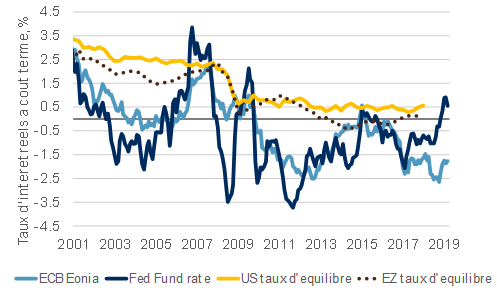

To make these tools more effective, some[2]are proposing changes to the monetary policy framework. The 2% inflation target was adopted in light of the stagflation experienced in the 1970s and 1980s. Today, economies face other problems: structurally low inflation (see The headache of low inflation in advanced countries) and negative real equilibrium interest rates (known as « neutral rates ») (see Chart 3).

Chart 3: Real interest rates set by central banks are likely to be negative more often

Note: we use Holston Laubach’s equilibrium rate estimates

Sources: ECB, Federal Reserves, Bureau of Labor Statistics, Holston Laubach, Author’s calculations, BSI Economics

The two main proposals are as follows:

- To stimulate low inflation, one option would be to opt for « average inflation targeting. » In concrete terms, if the inflation target were 2%, this would mean that after a period of inflation below 2%, the central bank would aim for inflation above 2% over a period long enough to achieve an average of 2%. Knowing this, economic agents (i.e., households, businesses, financial markets, and public administration) would theoretically adjust their inflation expectations upward, leading to faster price increases. Anticipating higher prices, households would demand higher wages, which would drive up business costs and therefore their selling prices. This additional inflationary pressure would therefore allow a return to equilibrium more quickly than is currently the case. (N.B. a variation on this approach is the « temporary price level targeting » proposed by Ben Bernanke);

- To counter the problem of negative interest rates, some economists (such as Olivier Blanchard and Larry Summers) recommend raising the inflation target. Doing so would immediately reduce real rates and, in the medium term, give the central bank more leeway before reaching negative rates.

But both proposals are subject to the same problem. They only work if agents adjust their inflation expectations to the new system. For this to happen, the central bank’s new strategy must be credible. Raising the inflation target in a context of weak prices seems difficult to implement. Furthermore, the monetary policy framework must be understandable. However, in the case of average inflation targeting, the reaction functions[3] of central banks would be more complex.

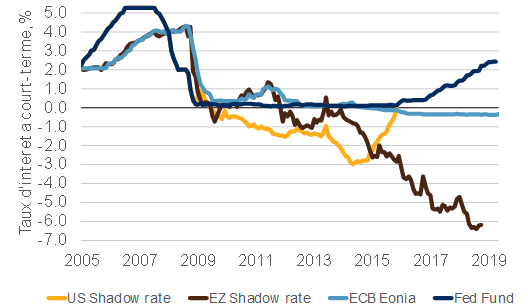

For the time being, central banks do not seem inclined to adopt these new models. The transition could generate more costs than benefits. If implementation does not work, central banks could lose credibility, making price stabilization even more difficult. Furthermore, although the current model has its limitations (including the difficulty of stimulating inflation and low or already negative interest rates), central banks have demonstrated that they can lower interest rates beyond negative rates through forward guidance or by targeting long-term rates through their monetary easing programs (see Chart 4). They have therefore already changed their monetary policy framework by developing tools other than interest rates.

Chart 4: Central banks can use other instruments to lower the effective interest rate below policy rates

Note: Wu-Xia’s « shadow » rates provide an estimate of effective interest rates in the US and the eurozone, taking into account the improvement in financing conditions through unconventional monetary policy measures.

Sources: ECB, Federal Reserves, Wu-Xia, BSI Economics

A macroprudential policy to limit the risk of bubbles in a low interest rate environment

Interest rates that remain low for a long period of time can pose a problem for financial stability. Low rates encourage greater risk-taking (e.g., in the search for yield) and therefore make credit bubbles more likely. To counteract these side effects, central banks are now making greater use of macroprudential measures, such as countercyclical buffers for banks and loan-to-value limits for households.

With these new tools, central banks also exercise greater control over credit markets. However, these new « powers » could jeopardize their independence as they would go beyond the mandate of price stability (see John Cochrane). Conversely, after the financial crisis, central banks were criticized for not taking financial markets into account. The macroprudential framework therefore seems to remedy the shortcomings of the pre-crisis model. It becomes all the more important in a context of low interest rates. In the case of the US economy, Kiley and Roberts ofthe Fed find that interest rates could be at their floor—close to 0%—more frequently (30 to 40% of the time) in response to economic crises. In the euro area, there is the additional factor that the interest rate is the same for all countries, even though economies may be at different stages of the economic cycle. Macroprudential policies at the national level thus help to mitigate the inherent problems of a single monetary policy.

Conclusion

Central banks will not return to the pre-crisis monetary policy: stabilizing inflation with interest rates alone is no longer possible in a context of negative real rates. The debate on monetary policy framework options is ongoing, but the proposals put forward are not yet convincing.

[1]Core inflation excludes prices subject to government intervention (electricity, gas, tobacco, etc.) and products with volatile prices (energy and food).

[2]See, for example, the discussions on this subject by the US Federal Reservehttps://www.federalreserve.gov/monetarypolicy/review-of-monetary-policy-strategy-tools-and-communications.htm

[3]The central bank’s reaction function establishes a rule for the use of monetary policy tools (such as interest rates) based on the difference between inflation and growth and the central bank’s targets.

[4]The countercyclical buffer is defined as an additional capital charge for banks. Its purpose is to « protect the banking system from potential losses related to the exacerbation of cyclical systemic risk […] thereby supporting the sustainable supply of credit to the real economy throughout the financial cycle, » see https://www.esrb.europa.eu/pub/pdf/recommendations/2014/140630_ESRB_Recommendation.fr.pdf?b11e1d7f73d148fd5924c5c6a30adcef