Should we fear another sharp rise in interest rates?

English version follows the French version

PDF in French

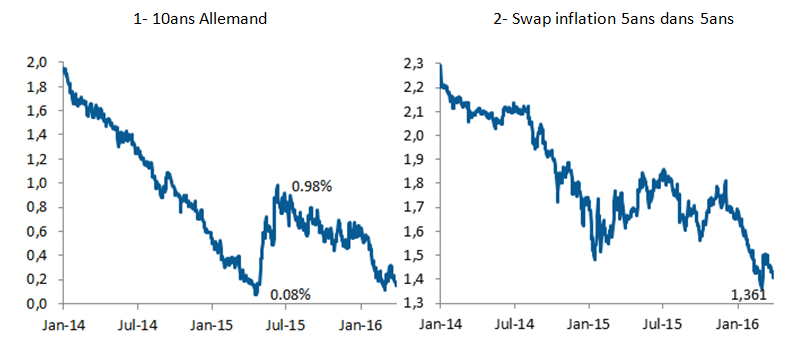

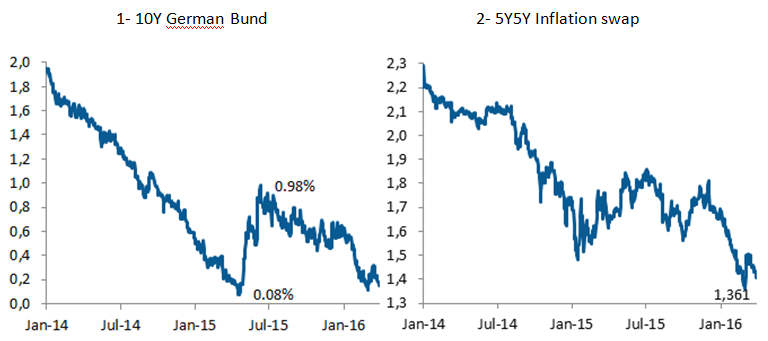

News: Last spring, the German 10-year interest rate (the Bund) plunged to an all-time low, supported by the ECB’s extremely expansionary policy. The Bund thus reached a yield of 0.07% before rebounding sharply to 1% within a few weeks. Similarly, in February 2016, the German 5-year rate fell to -0.4%, an unprecedented low. How low can interest rates in the eurozone go? What are the determinants of sovereign yields?

I- What are the determinants of sovereign yields?

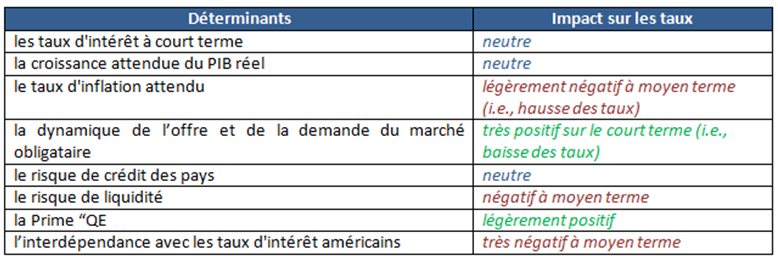

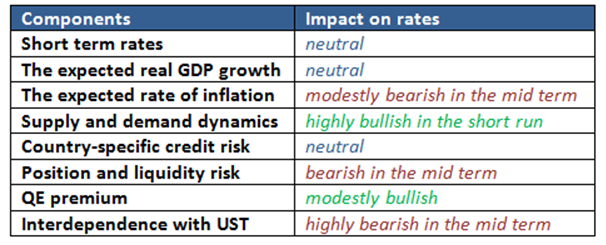

Long-term sovereign bond yields are linked to a wide range of factors, including:

– short-term interest rates;

– expected real GDP growth;

– expected inflation;

– supply and demand dynamics in the bond market;

– risk premiums.

The « risk premiums » factor includes: country credit risk (i.e., default risk), liquidity risk, term premium [1], and compensation for unexpected inflation. In a context of financial market globalization, interdependence with US interest rates is also a very important factor to consider.

II- How low can interest rates in the eurozone go?

1- Short-term interest rates

The European Central Bank (ECB) is responsible for defining and implementing monetary policy in the eurozone. The ECB sets the key interest rates for the eurozone banking system [2]. The institution can directly influence money market interest rates and indirectly influence the rates on loans granted by banks, as well as deposit rates. By controlling short-term interest rates, the Central Bank can also influence medium- and long-term interest rates [3]. Given the ECB’s reluctance to further reduce rates (at least for the time being) [4], the German 2-year rate is expected to remain in the range of -0.5% to -0.4%.

2- Expected real GDP growth

The latest economic indicators point to stable growth of around 0.4% in the first quarter of 2016. Generally speaking, the stronger the economic growth, the easier it will be for the country to repay its debt. All other things being equal, a rapidly growing economy generates more public revenue (via VAT and corporate tax) than a stagnant economy.

3- Expected inflation rate

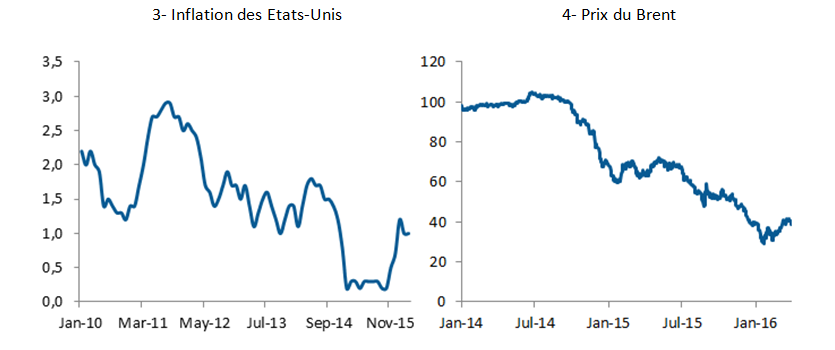

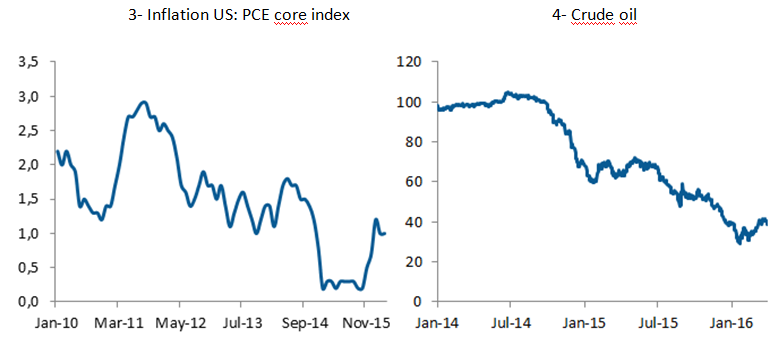

The 5-year forward inflation rate is a key indicator monitored by the ECB to assess investors’ inflation expectations [5]. The collapse in oil prices has caused market participants’ inflation expectations to fall well below the ECB’s 2% target (see appendix). While oil prices may have bottomed out, a massive rebound is unlikely in the coming months. However, the risk of inflation is not zero. Indeed, as Alan Greenspan suggests, « the return of inflation is a growing concern »[6] in the United States. Thus, the resurgence of US inflation could reignite fears of a stronger-than-expected acceleration of inflation in the eurozone. Any significant surge in US inflation would then be interpreted as the result of the Fed’s successful experimental monetary policy (« quantitative easing » ).

4- Supply and demand dynamics in the bond market

The amount of net sovereign debt issuance (the size of new issues minus coupon payments and redemptions of old bonds) after QE-related purchases (net issuance minus ECB purchases) is expected to be extremely negative in April, at around €120 billion. Assuming that these huge maturities will be reinvested in sovereign bonds, the dynamics of supply (new debt issues) and demand (reinvestment of maturities) are very favorable for eurozone bond yields.

5- Risk premiums

Country credit risk: there is no risk of imminent default, despite political instability in certain countries (Spain, Portugal, Ireland). Furthermore, European institutions now have powerful tools at their disposal (OMT, ESM, etc.) to alleviate fears of a new sovereign debt crisis. However, the case of Greece remains a concern in the medium term (but not in the short term). The government and its creditors are still negotiating the conditions necessary to unlock the new bailout program, and neither side has any interest in « playing with fire. »

Liquidity risk: it is difficult to accurately assess investor positioning, but it is reasonable to assume that low liquidity and significant investor positioning could easily exacerbate the rise in yields (i.e., a shock causing a rise in yields could quickly be magnified tenfold).

The « QE » premium: the ECB’s massive debt buyback program has created an unprecedented distortion between the quoted prices of bonds and their true economic value (fundamental value). Last year, investors hastily overestimated the negative premium associated with the scarcity of bonds bought back by the ECB. As a result, the sharp correction in bond yields last spring was largely due to the revaluation of this scarcity premium. Today, the ECB’s new measures seem to have been properly assimilated by the markets and should have a limited impact on bond yields.

Interdependence with US interest rates: a further rise in the Fed’s key rates in June could push European rates higher. This factor is closely linked to the trajectory of US inflation.

Conclusion

Overall, the sharp rise in sovereign yields is unlikely to be repeated in the short term. However, a resurgence of US inflation could trigger a rapid rebound in bond markets.

Appendices

Notes

[1] Term premium: refers to the excess return demanded by investors for holding long-maturity bonds instead of buying a series of short-maturity bonds. For example, the lender can either buy a 10-year bond or decide to buy a 1-year bond every year for 10 years. The term premium is generally positive.

[2] https://www.ecb.europa.eu/stats/monetary/rates/html/index.en.html

« The Governing Council of the ECB sets the key interest rates for the euro area:

o The interest rate on main refinancing operations (MROs), which provide most of the liquidity to the banking system.

o The deposit facility rate, which banks can use to make overnight deposits with the Eurosystem.

o The marginal lending facility rate, which offers overnight credit to Eurosystem banks. »

[3] https://www.ecb.europa.eu/mopo/intro/transmission/html/index.en.html

« Expectations of future key interest rates influence medium and long-term interest rates. In particular, long-term interest rates depend in part on market expectations of future developments in short-term rates. »

[4] Mario Draghi, March 10, 2016: « Finally, the Governing Council, taking into account the current outlook for price stability, expects the ECB’s key interest rates to remain at their present or lower levels for an extended period of time, well beyond the horizon of our net asset purchases. »

[5] Five-year inflation swap rate in five years: refers to the fixed rate of an inflation swap triggered in five years with a maturity of five years. One counterparty agrees to pay a fixed stream while the other pays a variable stream tracking the cumulative increase in the inflation index. Therefore, in order to achieve a fair agreement, the fixed rate is determined in such a way as to balance average inflation expectations over the investment period.

[6]http://www.bloomberg.com/news/articles/2016-03-17/greenspan-oil-slump-tied-to-demand-as-supply-is-building

[7]http://greece.greekreporter.com/2016/03/29/greece-needs-measures-worth-e5-5-billion-to-complete-bailout-review/

Can Eurozone yields experience another sharp setback?

News: Last spring, the 10-year Bund yield dipped to a record low buoyed by an aggressive ECB. The German 10-year rate fell as low as 0.07% before bouncing back sharply to close to 1% a few weeks later. Similarly, in February 2016, the 5-year German yield dropped to -0.4%, an all-time low. How far can Eurozone government bond rates fall? What are the drivers of sovereign yields?

I- What are the drivers of sovereign yields?

Long-term government bond yields are related to a broad spectrum of determinants, namely:

– short-term interest rates;

– expected real GDP growth;

– the expected rate of inflation;

– supply and demand dynamics;

– risk premiums.

Risk premiums capture the combination of: country-specific credit risk, liquidity risk, term premium for holding longer-dated bonds [1] and compensation for unexpected inflation. Interdependence with US interest rates is also a key driver of Eurozone yields as developed markets have become more integrated than ever.

II- How far can Eurozone government bond rates fall?

II- How far can Eurozone government bond rates fall?

1- Short-term rates

The ECB sets the key interest rates for the Eurozone banking systems [2]. It can directly influence money market interest rates and indirectly banks’ lending and deposit rates. By controlling short-term interest rates, the Central Bank can also affect medium and long-term interest rates [3]. Since the ECB seems reluctant—for the time being—to cut rates further [4], the 2Y German bond should remain range-bound between -0.5% and -0.4%.

2- Expected real GDP growth

The latest Eurozone surveys are consistent with steady GDP growth (approximately 0.4% q/q in Q1). The faster the economic growth, the easier it is for the country to pay back its debt. Indeed, all things being equal, a fast-growing economy generates stronger public revenues (through higher VAT and corporate taxes) than a stagnant economy.

3 The expected rate of inflation

The 5Y5Y inflation swapforward is the key market-based indicator used by the ECB to gauge investors’ inflation expectations [5]. Tumbling oil prices have dragged down inflation expectations significantly well below the ECB’s 2% target (see appendix). While oil prices may have bottomed out, they are not expected to soar materially in the coming months. Yet, Alan Greenspan highlighted that « we’re going to watch the inflation issue coming back » [6] in the US. The resurgence of US inflation may add upward pressure to Eurozone inflation expectations. In fact, any significant rise in actual and expected US inflation could be perceived as a success of QE experiment.

4- Supply and demand dynamics

Net government supply (issuance minus redemptions and coupon payments) after QE purchases (net supply minus ECB asset purchases) is projected to be extremely negative in April at around -€120bn, taking into account the €20bn increase in the asset purchase program. Assuming coupons will be reinvested in sovereign bonds, supply and demand dynamics are very supportive for Eurozone government rates.

5- Risk premiums

Country-specific credit risk: No imminent threats despite some political noise (Spain, Portugal, Ireland). In addition, European institutions have sufficient tools (OMT, ESM, etc.) to alleviate any sovereign debt crisis. Finally, the Greek case may resurface, but not in the short term (the government and its creditors are still negotiating conditions to unlock the new bailout program) [7].

Position and liquidity risk: Positioning is hard to assess accurately, but one can reasonably think that thin liquidity and heavy positioning could easily exacerbate the rise in yields.

QE premium: Bonds are trading significantly well below fundamental valuation mainly due to the ECB’s expanded asset purchases. Last year, the pricing of the scarcity negative premium went too far and too rapidly. In fact, the sharp setback in yields was largely driven by the repricing of the QE premium. The newly announced measures by the ECB seem already priced in; hence the downward impact on yields may be limited.

Interdependence with US long-term rates: Another Fed rate hike in June could put upward pressure on Eurozone sovereign bond yields. This component is closely linked to the path of US inflation.

Conclusion

All in all, another sharp setback is unlikely in the short term given supply dynamics and the ECB’s additional set of policies. By contrast, the resurgence in US inflation could trigger a rapid bounce back in government bond yields.

Appendix/Annexes

Notes

[1] Term premium: refers to the excess return required by investors to hold longer dated bonds instead of buying a series of shorter dated bonds. For instance, the lender can either buy a 10-year security or decide to invest in a new 1-year bond each year. The term premium is usually positive.

[2] https://www.ecb.europa.eu/stats/monetary/rates/html/index.en.html

“The Governing Council of the ECB sets the key interest rates for the euro area:

– The interest rate on the main refinancing operations (MRO), which provide the bulk of liquidity to the banking system.

– The rate on the deposit facility, which banks may use to make overnight deposits with the Eurosystem.

– The rate on the marginal lending facility, which offers overnight credit to banks from the Eurosystem.”

[3] https://www.ecb.europa.eu/mopo/intro/transmission/html/index.en.html

“Expectations of future official interest-rate changes affect medium and long-term interest rates. In particular, longer-term interest rates depend in part on market expectations about the future course of short-term rates.”

[4] Mario Draghi 03/10/2016:“Let me say that rates will stay low, very low, for a long period of time, and well past the horizon of our purchases. From today’s perspective, and taking into account the support of our measures to growth and inflation, we don’t anticipate that it will be necessary to reduce rates further. Of course, new facts can change the situation and the outlook.”

[5] 5Y5Y inflation swap forward: refers to an inflation swap starting in 5 years with a maturity of 5 years. One counterparty agrees to pay a fixed amount while the other pays the cumulative increase in the inflation index. Hence, in order to get a fair deal, the fixed rate is set to be the market expectation of the average inflation rate over the period, usually referred to as the breakeven inflation rate.

[6] http://www.bloomberg.com/news/articles/2016-03-17/greenspan-oil-slump-tied-to-demand-as-supply-is-building

[7] http://greece.greekreporter.com/2016/03/29/greece-needs-measures-worth-e5-5-billion-to-complete-bailout-review/