Abstract:

· As part of its efforts to deepen Economic and Monetary Union, the European Commission is currently considering the creation of securities backed by sovereign bonds;

· The liabilities of these securities would consist of a basket of sovereign bonds, but there would be a distinction between the junior tranche and the senior tranche;

· This proposal appears to be a real alternative to the Eurobonds previously considered, insofar as it does not involve risk pooling;

· The technical framework for this ambitious project will need to be clarified by 2020, along with a strategy to convince the public and investors of the merits of securitization.

The European Systemic Risk Board (ESRB) is considering the creation of sovereign-backed securities (SBS). In a recent discussion paper,as part of a process to deepen Economic and Monetary Union, these securities go further than Eurobonds, which have been categorically rejected by Germany. On paper, by pooling debt, such pan-European bonds should offer a lower rate than that at which Germany borrows.

However, there are real feasibility issues, and the success of such an undertaking would require the budget surpluses of the most solvent countries to cover the deficits of the less successful ones. SBSs therefore appear to be a real alternative, insofar as they do not involve debt mutualization. These would in fact be based on the creation of a financing vehicle—and therefore the issuance of debt (the liability)—backed by a basket of European sovereign bonds (the asset). Such a scheme involves a securitization process, which was heavily criticized during the recent subprime crisis.

What is securitization?

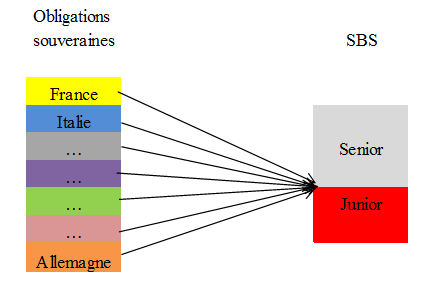

Securitization is basedon a fundamental principle of finance: diversification. The underlying idea is simple: it involves aggregating a multitude of assets to constitute the collateral for a loan. This is precisely the approach that was adopted during the subprime crisis: thousands of mortgage loans were aggregated and then sold to banks and investors. In theory, this kind of « layered structure » dilutes risk, particularly in the event of a credit event involving one of the issuers. This means that if a default occurs, it will only affect a tiny portion of the collateral. The securitization process therefore reduces the risk associated with these assets, since diversification means that the risk of the final portfolio is lower than the sum of the risks of each of the assets used as collateral. In the case of SBS (the asset) proposed by the ESRB, the liability would be a diversified portfolio of sovereign bonds.

Nevertheless, in order to meet heterogeneous demand in terms of risk-return profile and in a desire to emulate the United States in terms of risk-free asset supply, a dichotomy would be introduced within these SBSs, with a junior tranche contrasting with a senior tranche:

· The junior component would comprise the riskiest tranche, accounting for 30% of the total: it would be the first line of defense in absorbing shocks, such as a potential sovereign default by a country. A breakdown of this tranche itself is not ruled out, with a « first loss » portion (also called « equity »), which, as its name suggests, would be the first to be impacted in the event of a credit event, and a mezzanine portion[1];

· Conversely, the senior tranche would be more liquid and should tend towards zero risk. This tranching of SBSs would therefore satisfy the demand of investors with varying risk profiles. The underlying idea is to create a risk-free asset from a portfolio of assets, some of which are risky (heterogeneous because they include debts of varying quality within the zone), and therefore to diversify risk.

The advantages of SBS

The benchmark portfolio should contain debt issued by the central government of each eurozone member country. Non-member states, such as Sweden, could also decide to participate if they wanted to issue debt in euros. The allocation key could thus depend on the country’s GDP or population, the idea being to reflect the contribution to the economy within the zone, in the same spirit as each country’s contributions to the European budget.

SBS would thus offer the same advantages as Eurobonds, while avoiding debt mutualization, which has been a sticking point for the most creditworthy countries, particularly Germany. The creation of such securities, backed by European bonds, should in particular make it possible to standardize financing conditions within the zone, thereby limiting « financial fragmentation » between « central » and « peripheral » Europe. While capital flows to peripheral countries are currently highly dependent on economic conditions, these countries could now participate in the supply of risk-free assets on the markets.

Another key aspect that has been highlighted is the diversification of the portfolios of investors who would hold these securities, particularly banks. Currently, their liabilities are closely linked to their country of origin (with a domestic preference in investment decisions, particularly in terms of bond allocation), which increases the risk of transmission between a country and its financial institutions in the event of a shock. Thus, in the event of a deterioration in a country’s economic situation, the fact that domestic banks currently hold a large portion of this debt may be cause for concern. The introduction of SBSs would therefore mitigate this interdependence at the country level and offer greater diversification of bank balance sheets at the European level, thereby reducing systemic risk.

Furthermore, one of the stated objectives of this venture is to create a risk-free asset with the senior tranche of SBSs in order to compete with US T-bills. Despite its prominent role in the global economy, Europe has not yet managed to achieve sufficient unity, particularly in fiscal terms, to offer investors an alternative. Demand for such assets is growing and is being fueled by regulators. It is also argued that the creation of a safe asset, issued in large volumes, should improve liquidity. Finally, the intervention of this ad hoc entity directly on the primary market should lead to greater transparency, which is a positive step towards removing the stigma attached to collateralized debt obligations ( CDOs).

Areas of uncertainty

On a more technical level, a suitable ad hoc issuing entity needs to be found. There is still a great deal of uncertainty on this subject, according to the recently published EMU white paper, which refers to a « commercial entity or institution. » One thing is certain: for reasons of independence, the ECB could not take on this role, as it could itself be a buyer of SBSs. While in theory the ECB should not be responsible for creating these new financing vehicles, it is conceivable that in an adverse scenario, it could take measures to support the euro (similar to the current asset purchase program), which could be a source of moral hazard. Furthermore, the 30/70% split between the junior and senior tranches respectively still seems somewhat arbitrary and should be based on an in-depth analysis of sovereign default scenarios.

While SBS proponents highlight improved liquidity, it should be recognized that two opposing effects may be at work. Indeed, the issuance of large volumes of SBS could be a good sign in terms of liquidity. Even if, for the moment, the proposals guarantee the circulation of two-thirds of each country’s government bonds, there is a risk that the privilege granted to European bonds, which is already high due to asset purchase measures, will ultimately deteriorate market liquidity. There is therefore a significant risk of a shortage of more « traditional » sovereign bonds in an already tense market.

Furthermore, including the least creditworthy countries in the basket of assets constituting the collateral could discourage the most cautious investors, who may still prefer to hold a German bond rather than such a CDO, for which no valuation method has been developed. Therefore, in order to make them substitutable in the eyes of banks, preferential regulatory measures may be necessary to support the holding of SBSs (which could, for example, be accepted by the ECB in repo transactions, as suggested by a group of economists). For the least creditworthy countries, the risk of polarization between the share of debt in SBS assets and traditional bonds issued by the central government that continue to circulate on the market should not be underestimated.

Finally, the creation of such SBSs must be accompanied by a political will to regulate them, in order to avoid any abuses (such as a surprise redefinition of the distribution key to deal with one-off shocks) and to reassure public opinion. Indeed, securities backed by a large layer of debt, and more generally securitization, are often blamed as the cause of the 2008 crisis. Europe will therefore have the difficult task of de-demonizing SBSs.

Conclusion

SBSs, securities backed by traditional sovereign bonds, are proposed by the ESRB in a bid to increase financial union within the eurozone. In particular, they would reduce the interdependence between banks’ balance sheets and the solvency of their country of origin. With a carefully chosen threshold, the senior tranche could even constitute a risk-free asset, thus satisfying Europe’s ambition to compete with US Treasury bonds.

The launch date, announced for 2020, is far enough away to allow for the development of a solid technical and regulatory framework. The issue of legitimizing the use of securitization, which has been criticized by the general public since 2008, will require a great deal of education. It will probably be more difficult to convince investors to turn away from German debt in favor of these new instruments.

[1] A CDO is generally divided into several tranches with different risk profiles. These include the senior tranche, the mezzanine tranche, and the first loss tranche. In the context of SBSs, the junior portion would therefore consist of the mezzanine and first loss tranches.