Usefulness of the article: This article is a follow-upto an initial post on sovereign debt restructuring in emerging countries. The aim here is to identify the main tools and complex issues involved in debt restructuring and also to set out a line of thinking that could facilitate such operations.

Summary :

- Debt restructuring generally takes three forms: extending maturities, reducing interest charges, or canceling debt. These three options can be implemented simultaneously or separately.

- While solutions exist to facilitate restructuring (e.g., through collective action clauses), the diversity of creditors and the high level of opacity surrounding the actual level of debt in certain countries and their commitments to creditors are significant obstacles to implementing restructuring processes.

- Recent initiatives by the G20 and the IMF (common framework) have improved the multilateral framework for sovereign debt restructuring. However, these measures appear insufficient at this stage to achieve greater transparency.

- In order to encourage countries to be more transparent, they could benefit from preliminary relief or even other forms of aid. The establishment of an incentive framework would be useful to complement the initiatives of the G20 and IMF. It would be possible to better identify sources of vulnerability and thus anticipate restructuring needs while providing visibility to creditors.

The increase in public debt in emerging and developing countries has been a cause for concern for several years, a sentiment reinforced by the explosion of public debt caused by the Covid-19 crisis. As a result, the most fragile countries are facing the risk of over-indebtedness, with some already in default (Lebanon, Zambia). This raises the question of debt restructuring and how it should be carried out.

An initial short article identified the various creditors of emerging countries and explained how changes in the structure of this debt (with the rise of China and private creditors) were creating new challenges in the event of restructuring.

This note will provide some answers as to how the debt of emerging economies can be restructured, presenting the main scenarios and the tools available to countries and their creditors for a successful restructuring.

What types of restructuring are there?

There are three main debt restructuring tools for sovereign states:

- Extending maturities;

- Reducing interest charges;

- Partial cancellation of the debt amount.

These restructuring methods can be implemented simultaneously or separately, and can take place before or after a default. However, restructuring appears to be more effective (in the sense that it leads to a significant reduction in debt and has a limited economic and financial impact) when it is implemented prior to default (Asonuma, 2020).

Extending maturities involves extending due dates[1] and leads to a deferral of the cash flows received by creditors, without the latter having to bear any losses. For an indebted country in difficulty, extending maturities allows it to spread its debt repayments over a longer period of time and thus smooth its debt amortization, enabling it to meet its deadlines and avoid accumulating arrears or even defaulting.

Whether the debt is in the form of loans (as is mainly the case with official creditors) or bonds (more commonly with non-official creditors[2]), the first repayments are generally interest payments. A reduction in the interest burden through a lower interest rate can be used to ease the weight of repayments. For a creditor, this necessarily involves losses in relation to the initially expected cash flows, as their investment is always remunerated (by interest, a coupon, etc.). However, with this process, a creditor would not suffer any loss on the principal, which remains the most important part of their investment. For the country benefiting from such relief, the advantage is also that it avoids having to seek new sources of financing on unfavorable terms in order to meet its interest payment commitments. While this option can help address the debtor’s liquidity problems, it seems to have limited scope in cases of insolvency.

Cancellation, also known as a haircut, is a process that allows for much more significant debt relief for countries. The nominal value of a debt security is then reduced to a greater or lesser extent, depending on the percentage of the haircut. As a result, the total amount of debt can be significantly reduced. This type of restructuring may also consist of an exchange of debt securities on terms more favorable to the borrower (nominal reduction, lower interest rates, currency changes, inclusion of clauses, etc.). Cancellation inevitably exposes creditors to high losses, but such an agreement ensures that at least part of the funds committed will still be recovered.

A study by the European Stability Mechanism(ESM) shows that, on average, countries that benefited from haircuts did not experience a marked slowdown in activity in the two years following the restructuring (before a sharp acceleration two years later); while in countries that opted for another type of restructuring, real GDP growth was weak, even beyond two years. According to the ESM, while the decline in the debt-to-GDP ratio was high in countries benefiting from a haircut, the public deficit tended to widen rapidly one year after the restructuring. The opposite was observed in countries that did not opt for a haircut, with a rapid reduction in the public deficit and even primary surpluses after two years. The method of restructuring therefore appears to have significant ex post implications in terms of growth prospects on the one hand and fiscal discipline on the other.

What avenues are available at this stage to facilitate restructuring with private creditors?

The increased involvement of non-official creditors in restructuring has become necessary for emerging countries given their growing share of public and publicly guaranteed external debt (nearly 40% in 2020 compared to 33% in 2006). The greater the diversity of profiles[5] and the larger the number of creditors[6], the more complicated it becomes to implement a restructuring. Indeed, recalcitrant creditors can block an agreement, even if it has been approved by a majority of creditors.

Furthermore, the development of collateralized debt (particularly on future commodity revenues) is an additional obstacle to restructuring. These financial arrangements provide significant leverage to creditors and do not encourage them to accept a restructuring denial.

The involvement of private creditors plays a key role. In this regard, the inclusion of collective action clauses (CACs) in public debt securities since the early 2000s offers new prospects for restructuring[8]. According to the European Parliament, « a CAC allows a qualified majority of bondholders to agree to a debt restructuring […] that will be legally binding on all creditors. » It would therefore be easier to impose the terms of a restructuring, even if a minority of creditors opposed it. CACs notably facilitated the restructuring of Argentina’s bond debt in 2020. According to the IMF, while 91% of new sovereign bond issues have been accompanied by CACs since 2014, the share of sovereign bonds with CACs represented only 50% of the global stock in 2020.

Countries experiencing severe sovereign stress could arrange swaps of their bonds without CACs for new bonds with CACs with their creditors (external or even domestic[10]) even before defaulting, in order to alleviate, at least partially, the issues associated with the absence of CACs[11] and focus on negotiations around their non-bond debt.

The participation of private creditors also remains heavily dependent on the involvement of multilateral and, above all, bilateral creditors, where the contours of debt vis-à-vis non-Paris Club countries (the Gulf countries but also, and above all, China) remain a thorny issue (see first post published on BSI Economics).

While the IMF is working to get the various creditors to define a common framework for resolving insolvency situations, only three countries (Ethiopia, Chad, and Zambia) have come forward at this stage to benefit from debt relief under this framework, and none has yet been successful. This initiative must be complemented by an incentive framework, which does not yet exist, to encourage countries to be more transparent about the quality of their budget data.

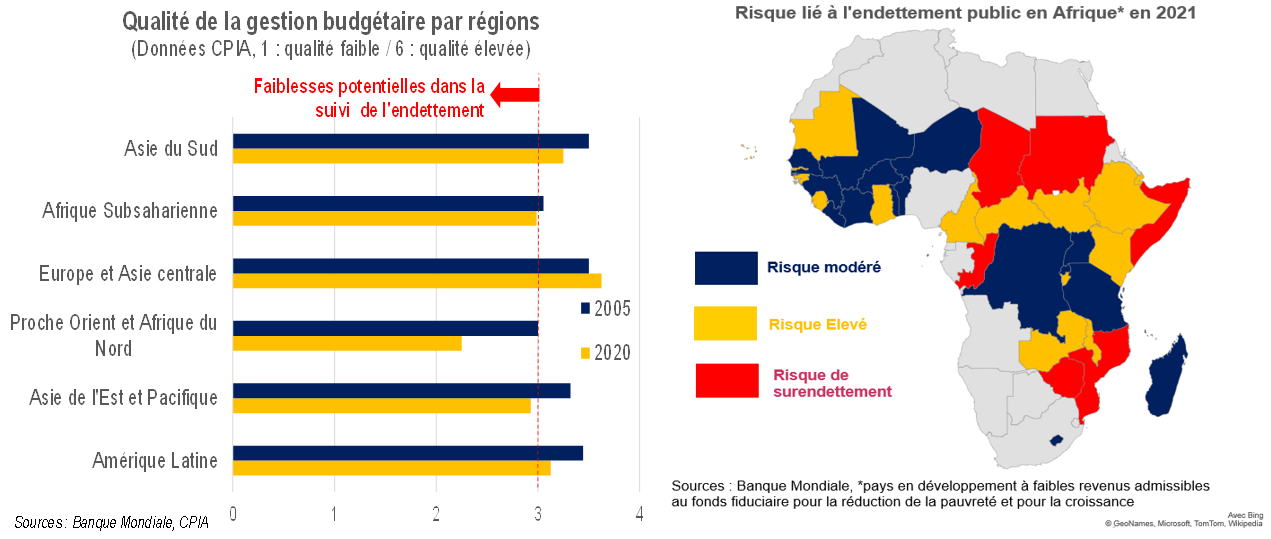

The transparency of public finance data is particularly worrying insub-Saharan African countries, where the quality of public finance management is among the lowest in the emerging world and has even deteriorated slightly over the past 15 years (see chart below left). This situation is all the more worrying given that several countries in the region[12] face a significant risk in terms of debt, or are even in a situation of over-indebtedness (Congo, Mozambique, and Chad, for example; see chart below right).

Proposal for an incentive framework to promote greater transparency

Only an incentive framework would be effective in encouraging countries to disclose comprehensive information about their debt. If countries remain opaque, it is because this « strategy » is actually more advantageous to them than revealing the true state of affairs. The provision of reliable information should therefore be rewarded. For a given country, this « reward » would consist of relatively more favorable treatment in the context of debt reprofiling compared to a country in default that has not made any prior effort to be transparent.

In such a framework, a country could be given a certain amount of time (e.g., less than one year) to provide as much additional information as possible on the state of its public finances to the Paris Club and the London Club. In return, this country would benefit from a preliminary agreement on an initial phase of uniform debt relief (i.e., all its creditors would « suffer » this relief, in an amount proportional to their share of the total debt of the country in question). To ensure that this preliminary agreement is not too detrimental to creditors, it could take the form of a simple deferral of maturity rather than a cancellation of interest charges or partial non-repayment of principal.

This pre-agreement could also open up rights to targeted transfers of Special Drawing Rights (SDRs). With the IMF having allocated USD 650 billion in new SDRs in August 2021, opening up such rights to countries in difficulty would be perfectly in line with the IMF’s approach. Indeed, the IMF wants developed countries to transfer their SDRs to emerging and developing countries to help them absorb the shock of the pandemic. Countries signing the pre-agreement could thus invoke their rights and benefit from SDR transfers. This would provide them with funds to repay their creditors while continuing to pursue the public policies necessary for their development. To strengthen fiscal discipline, a percentage of these SDRs could be mandatorily allocated to specific measures, as is already the case under IMF programs: establishment of a land registry, digitization of the tax collection process, substitution of certain subsidies (on energy prices, for example) with social transfers targeted at low incomes, etc.

This preliminary agreement could facilitate restructuring efforts with the possibility of swap operations (see above regarding CACs). Exchanges with new forms of instruments, in the form of contingent debt, could be considered for both the « bond » and « loan » segments. The idea is to offer countries the opportunity to convert part of their debt into contingent debt, the repayment of which is indexed to easily measurable socio-economic variables[15] (growth in GDP per capita, growth in public revenue, structural primary public balance as a percentage of GDP, etc.). This would give countries greater flexibility in lean times by allowing them to defer maturities, but also to repay more quickly in the opposite scenario.

This preliminary agreement could also provide for specific debt arrangements with multilateral creditors (amounts of interest charges eligible for deferral, grace period for interest repayments, percentage reduction in the average interest rate, etc.). To strengthen the incentive effect, these arrangements should be regressive, so that a country that has made sufficient efforts toward transparency within the allotted time frame would enjoy conditions that are necessarily more favorable than those of a country that is opaque or slow to do so, beyond the deadline.

To reinforce discipline and also encourage creditors to be more transparent and involved, this framework could provide for « sanctions » for creditors who have contributed to maintaining opacity. For example, they would automatically lose their pari passu status in a restructuring and would therefore have to comply with the conditions set by the other creditors, or even have less favorable conditions automatically applied to them.

Prevention is better than cure

Despite the experience gained from practical cases and innovations since the 2000s, public debt restructuring remains an extremely delicate exercise that is difficult to replicate from one country to another.

Although proposals are emerging from the IMF, they seem insufficient to facilitate the efforts of emerging countries or to provide a clear framework for certain creditors.

Only the establishment of an incentive framework would trigger a more virtuous and transparent process. The increased visibility provided by such a framework would make it easier to identify restructuring needs upstream, while involving the various creditors more closely. Such a framework would also offer greater flexibility, allowing intervention even before a default occurs. Prevention and adaptation can only have beneficial effects compared to scenarios of forced and disorganized restructuring, and would protect countries in difficulty and their populations from deep crisis.

[1]In addition, the extension of maturities may be accompanied by a grace period of varying length for new loans, during which the first repayments would be deferred.

[2]Official creditors include bilateral and multilateral creditors, see previous post on BSI.

[3]For example, with a haircut of 40%, a bond with an initial value of 100 will now be worth only 60.

[4]Under the HIPC and MDRI initiatives, where debt cancellation was granted, the debt ratio of sub-Saharan African countries fell from an average of 66% of GDP in 2000 to 24% in 2008. This debt cancellation was granted by official creditors (bilateral and multilateral).

[5]See previous note on this subject. The case of domestic creditors is another special case, as the debt is governed by local law and the restructuring of these domestic actors generally has a more profound impact on the real economy.

[6]Depending on the status (senior, pari passu clause , etc .) and the divergent interests of the various creditors. For example, the restructuring of syndicated loans requires the agreement of all participants.

[7]See the example of Chad’s sovereign restructuring in 2017/19.

[8]In reality, there are several ranges of CACs, and these have tended to evolve, with some CACs no longer allowing an individual creditor to block an agreement if they do not hold 25% of the debt stock rather than 25% of a bond issue as was previously the case.

[9]A 45% haircut on foreign currency bond debt under foreign law, allowing for a reduction in principal repayments of USD 37.7 billion over 10 years.

[10]According to the IMF, domestic public debt accounts for an average of 46% of total public debt in emerging countries.

[11] In particular, the risks associated with potential litigation when securities are recovered by vulture funds.

[12] Data for low-income developing countries eligible for the Poverty Reduction and Growth Trust.

[13] And more specifically, the amounts of debt owed to China and the collateral required in the case of collateralized debt.

[14]SDR allocations are distributed among countries according to a quota (defined in particular by: GDP weight, degree of openness of the economy, foreign exchange reserves), which de facto makes developed countries the largest recipients of new SDRs.

[15] Or in relation to climate criteria, as was the case with Grenada, which has a specific clause linked to natural incidents that trigger payment suspensions and maturity extensions.