Purpose of the article: The purpose of this note is to outline the various possible scenarios for sovereign bond and FX (foreign exchange) markets for the remainder of 2019 and to identify the risks that could increase volatility in the equity, bond, and FX markets.

Summary:

- The likely slowdown in the global economy is expected to be a major challenge for central banks and sovereign bond and foreign exchange (FX[1]) markets in 2019. In the eurozone, while the latest economic data has shown signs of a slowdown, the ECB is adopting an increasingly less accommodative monetary policy.

- After four rate hikes in 2018, the Fed is now exercising caution and is likely to slow the pace of future rate hikes in light of economic uncertainties. Key interest rates are in the 2.25%-2.50% range. The market does not anticipate any further rate hikes this year, and the Bloomberg consensus[2] is for only one rate hike in 2019, compared with three last November.

- Between trade tensions between the United States and China, central bank caution, and economic slowdown in advanced countries, sovereign bond yields are likely to rise slightly. The rise in rates in the eurozone will also be sensitive to the Eurosystem’s policy of reinvesting maturing bonds.

The end of 2018 was marked by the risk of a global economic slowdown. Core inflation remained stable and below forecasts in the eurozone, even though most of the economies in the Economic and Monetary Union are at full employment.

As a result, 2019 is beginning with the theme of a global economic slowdown, as reflected in economic surveys. Finally, global risks continue to increase uncertainty and market corrections are to be expected.

1. Macroeconomic developments and possible market reactions

1.1) Growth is expected to continue at a pace above its potential: the theory ofa soft landing in the United States and the eurozone

Despite the disappointing macroeconomic situation in 2018 (Chart 1), which took the markets by surprise, the economic climate remained positive, with growth figures still above potential (1.8% in 2018 for the eurozone, compared with an estimated potential growth rate of 1.5% according to the European Commission). However, confidence among companies that generate most of their revenue from exports has fallen sharply in recent months, particularly in Germany, due to trade tensions and the introduction of new anti-pollution standards in the automotive industry. This is beginning to be reflected in macroeconomic « hard data.« For example, Germany and Italy recorded negative growth in the third quarter of 2018 ( -0. 2%and -0. 1% respectively), while Spain remained buoyant (0.7% in Q3 2018 and 2.4% year-on-year). The composite PMI index for activity in the eurozone (flash) fell again in January (-0.4 points to 50.7), but less significantly than in December. The index declined in services (-0.3 points to 50.8) and more sharply in industry (-0.9 points to 50.5). While a global economic recession is not one of the central scenarios at present, the announcement of new tariffs could weigh on the global economy, and the slowdown in economic growth in the eurozone could be due to a decline in external demand.

Chart 1 – Eurozone: PMI trends, quarterly GDP growth, and 10-year German interest rates

Sources: Bloomberg, Markit, Eurostat, Macrobond, BSI Economics

1.2) In the United States, the government has widened the deficit at the end of the cycle, limiting the positive effect on growth

US growth is expected to slow to around 2.2% this year, compared with 2.9% forecast in 2018. Fears over trade tensions are weighing heavily on business sentiment. In addition, surveys point to a slowdown in business investment. Core inflation is expected to remain stable (2.0% in 2019 according to the consensus) and is even beginning to show signs of slowing (excluding an increase in trade tensions that could push up the prices of imported goods). Finally,the partialshutdown of federal services will likely have a significant impact on growth figures for the first quarter of 2019. Its weekly cost is estimated at USD 5-10 billion. The effects of the US administration’s fiscal policy, which improved after-tax profits and household disposable income, will fade significantly in 2019 and are likely to disappear in 2020. With a deficit of 3.9% of GDP in 2018, the government has less room for maneuver than before, particularly with the new Democratic majority in the House of Representatives. The consensus forecast is for the deficit to worsen to 4.6% of GDP in 2019.

The application of tariffs is likely to weigh on growth throughincreased uncertainty for businesses, disruption to supply chains, and higher import prices, which could reduce household purchasing power. Finally, according to a Bloomberg poll, the probability of a recession within the next 12 months rose from 15% in December 2018 to 25% in February 2019.

1.3) In the eurozone, economic growth will be driven more by domestic demand due to rising wages

At the start of the year, the IMF, private sector economists, and the European Commission revised their growth forecasts for the eurozone in 2019 downwards. According to the European Commission, GDP is now expected to grow by 1.3% this year, compared with 1.9% previously. According to a Bloomberg survey, the probability of recession within the next twelve months rose from 16.5% in December to 20% in February.

The components of domestic demand (particularly employment and wages) remain buoyant, but theoutput gap probably closed in 2018, which should be followed by a slowdown.

Growth will be supported by moderate fiscal policy (at least in Germany and, temporarily, in France, while the effect of the measures taken in Italy should be offset, at least in part, by higher bond yields).

2. Tightening of monetary policy in advanced economies amid economic uncertainty

Weaker and divergent growth, as well as signs that the cycle is coming to an end, have complicated the task for central banks. Whereas previously the macroeconomic conditions were clearly in place for normalization: (1) improvement in core inflation; (2) a further decline in unemployment; (3) higher wage growth; and (4) lower public deficits allowed central bankers to justify normalization. The signals are now pointing in different directions: political uncertainty, trade tensions, slowing growth, and finally the recent downward adjustments in financial asset valuations are leading to much greater caution.

This year will be a challenging one for central banks, which must manage normalization alongside the economic slowdown. The Fed is gradually moving towards a slowdown or even an end to its normalization and remains data dependent, while the ECB is shifting towards an increasingly less accommodative monetary policy. Nevertheless, depending on economic developments and market volatility, the ECB will have to adapt its communication to the markets regarding its monetary policy intentions.

2.1) Signs of a slowdown as the ECB adopts an increasingly less accommodative monetary policy

In December, the European Central Bank ended its Expanded Asset Purchase Program (EAPP). From now on, maturing sovereign bonds held by the national banks of the Eurosystem and the ECB will be reinvested at least until the ECB begins to raise key interest rates. Reinvestment flows will keep the stock of assets held at a constant level, and the stock effect (bonds held on the ECB’s balance sheet) will maintain downward pressure on interest rates.

The first rate hikes are not expected to take place before September 2019 or December 2019, as clearly communicated by the ECB in its forward guidance in June 2018 (« at least until the summer of 2019 »)and reaffirmed at the last Governing Council meeting in January. The first rate hike could be on the deposit rate, followed by an increase in all key rates at the end of 2019.

In the event of a more rapid slowdown in the eurozone economy, disappointing core inflation (Chart 2) or a sharp decline in credit growth, the ECB could announce new TLTROs (targeted longer-term refinancing operations) before June, but also postpone the first rate hike until 2020, as currently anticipated by the market.

The main argument in favor of announcing new TLTROs is the repayment by commercial banks of previous 4-year TLTROs that mature in the summer of 2019. In addition, nearly 80% of the amounts concern Italian and Spanish banks, which are currently experiencing difficulties in complying with the increase in macroprudential ratios that is taking place this year. The announcement of these new measures could therefore provide them with some relief.

At the last Governing Council press conference on January 24, the ECB acknowledged a certain deterioration in the economic outlook[7] (« if the impact of some of these factors were to fade, short-term growth momentum is likely to be weaker than previously anticipated »), pointing to a downward revision of its risk balance (« the risks to the euro area growth outlook have shifted to the downside »). The ECB will publish its new macroeconomic projections on March 7 at the next Governing Council meeting.

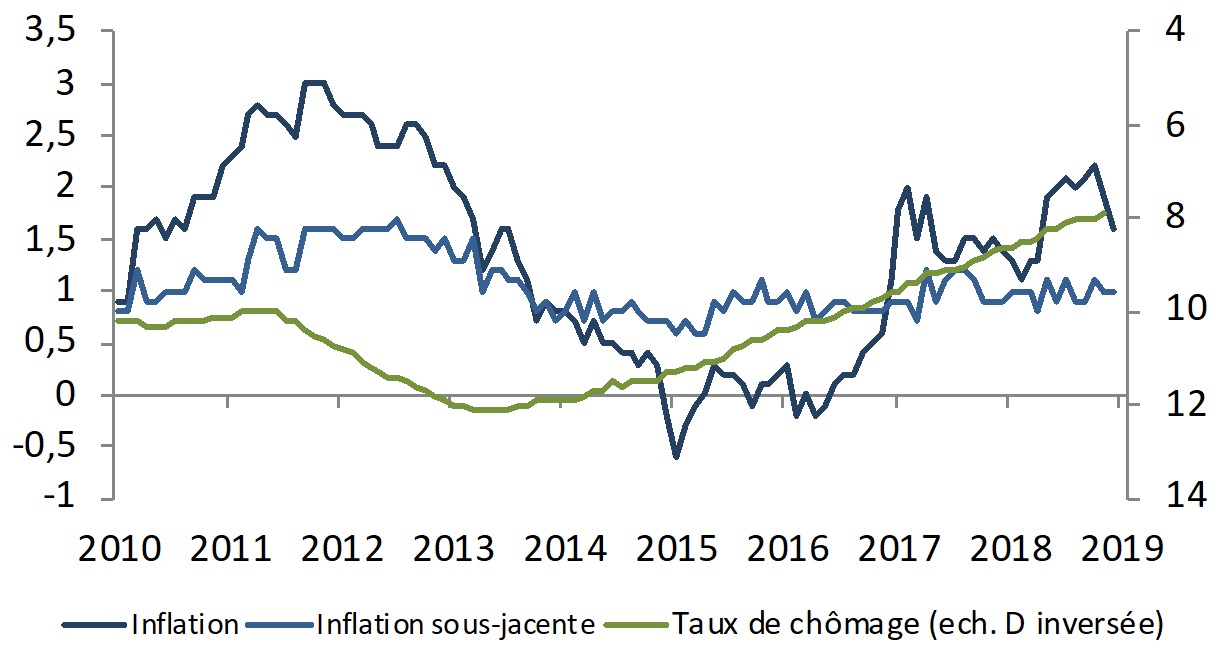

Chart 2 – Eurozone: Inflation, core inflation, and unemployment rate

Sources: Bloomberg, Eurostat, Macrobond, BSI Economics

2.2) Fed: towards a slowdown in monetary policy tightening and a » data-dependent » approach

Fed Chair J. Powell recently mentioned that, given stable inflation, the FOMC would be patient and was prepared to change the direction of monetary policy if necessary. He also believes that the markets are too pessimistic about economic data, which remains encouraging (« The markets seem to me to be pricing in downside risks, and they are clearly going well beyond the activity data »).

At the last FOMC meeting in January, the Fed dropped its reference to further gradual rate increases, meaning that the next move is just as likely to be a rate cut as a rate hike.

In line with market expectations, the FOMC decided to maintain the status quo, leaving the target range unchanged at 2.25% to 2.50%, and indicated that it would be patient in determining its next move « in light of global economic and financial developments and subdued inflation pressures. »

During the press conference, Chairman Powell explained why the Fed had made gradual changes to its statement and mentioned that the international environment, which was considered a cause for concern, could weigh on the US economy. This argument may have come as a surprise, as the US economy is less open than the eurozone economy (degree of openness at 15% of GDP compared to 45% in the eurozone in 2017), so it is less sensitive to situations in the rest of the world in the event of a shock.

3. Developments in sovereign bond markets and the EUR/USD

The pace of monetary policy normalization, macroeconomic data, and ongoing trade tensions will be the main factors studied by financial markets in 2019.

3.1) US rate trends:

At the start of the year, US rates fell significantly due to the Fed’s shift to a more dovish stance.

Treasury bills finally played their role as a safe haven, with yields falling 67 basis points from a peak of 3.23% on November 8 to a low of 2.56% on January 3.

US rates are likely to rise gradually, according to the Bloomberg consensus, from 2.8% at the end of Q1 2019 to 3.1% at the end of Q4 2019.

In this scenario, the Fed would pause its rate hike cycle and the upward movement in yields would mainly come from higher inflation expectations (which could be driven by higher oil prices or higher core inflation).

However, they will depend on:

(1) the number of rate hikes by the Fed;

(2) Treasuryissuances by the US Treasury;

(3) external demand for bonds;

(4) the economic outlook, which is expected to be less favorable than before.

While US growth is expected to slow in 2019, estimates of neutral rates[8] are expected to remain close to 2.75% to 3%, i.e., close to current levels. Stable inflation should keep the term premium[9] under control.

3.2) European rate trends: a limited rebound

In 2018, the Bund[10] benefited from a rally ( shift to these bonds during a bear market) due to:

(1) weaker-than-expected economic growth at the end of the year

(2) core inflation below expectations in 2018 (1.0% versus 1.1% expected for the year);

(3) concerns about the Italian budget since May;

(4) a more dovish tone than anticipated from the ECB, which highlighted certain uncertainties

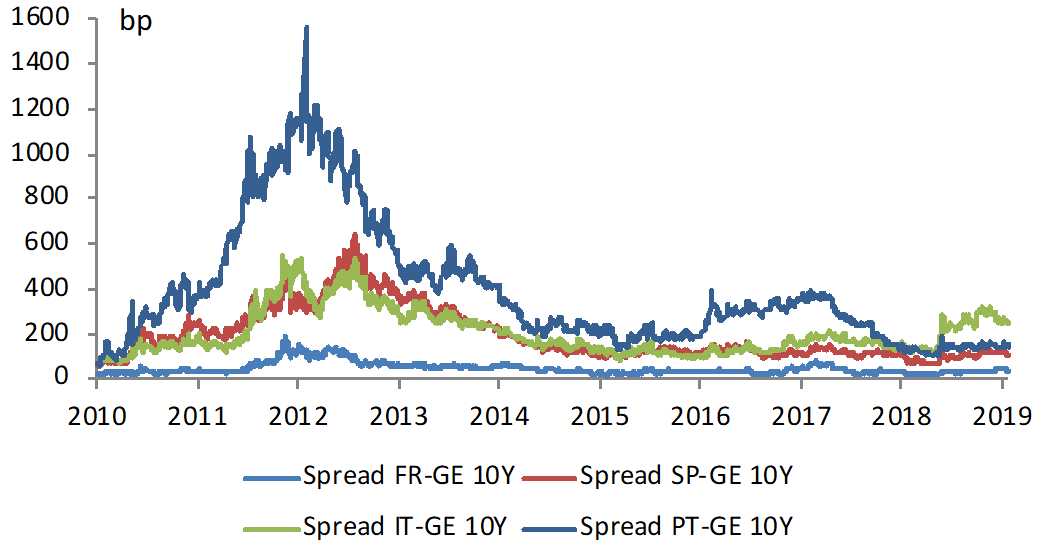

In 2019, a year marked by an increasingly less accommodative monetary policy (in the scenario of a first rate hike in September 2019), sovereign rates in core (Germany) and semi-core (France) Eurozone countries are expected to rise gradually, along with a slight widening of sovereign spreads (Chart 3).

Economic activity in the eurozone slowed in 2018 and the latest data show no encouraging signs for 2019 (declining economic sentiment index, declining PMI, IFO surveys). If the situation deteriorates more significantly than anticipated by the markets, the ECB may be forced to delay or even cancel its normalization, which could limit the upside potential for 10-year Bund yields. In addition, the political agenda for 2019, particularly the European elections in May and early elections in Spain and Italy, could cause European sovereign rates to fluctuate. The Bloomberg consensus forecast is for the German 10-year yield to rise from 0.34% at the end of Q1 2019 to 0.71% at the end of Q4 2019.

Chart 3 – Change in sovereign spreads relative to 10-year German rates

Sources: Bloomberg, Macrobond, BSI Economics

3.3) Focus on Italy: Italy is not immune to renewed tensions on BTPs (see: Italy and the European Commission: the final showdown)

Italian bonds have been the main driver of movements affecting spreads between eurozone sovereign bonds (between core and peripheral countries) since the second quarter of 2018. However, volatility has decreased (the 10-year BTP-Bund spread fell from 327 basis points on November 20, 2018, to 277 basis points on February 11, 2019) since the government revised its public deficit forecast downwards to 2% of GDP from the 2.4% initially forecast for 2019 and reached a compromise with the European Union.

To avoid further market pressure, the Italian government will need to strengthen its fiscal credibility. Italian sovereign spreads could narrow again, but only up to a certain limit of 250 basis points (10-year BTP-Bund spread) due to (1) a strong need for bond issues in 2019 (around €250 billion), (2) the risk of early elections, (3) the approach of the European elections in May, and finally (4) the weakness of the Italian economy.

Focusing on the Italian budget, the market considers the growth forecasts in the 2019 budget to be overly optimistic (1% of GDP in 2019 versus 0.4% for the consensus). As a result, there is a very high risk that budget targets will be missed due to lower tax revenues (caused by weaker growth). It is possible that Italian sovereign bonds will come under pressure again in the middle of the year from markets that already reacted strongly in 2018 during the elections, the formation of the government, and negotiations with the European Commission. Several factors support the hypothesis of renewed tensions: (1) the publication of first-quarter 2019 figures, (2) the European elections, (3) the European Commission’s review of budgetary stability programs, and (4) the revision of sovereign ratings by rating agencies.

3.4) EUR/USD trend: less upside risk for dollar appreciation

The euro did not appreciate gradually in 2018 as anticipated by the markets. Italian risk, as measured by the 10-year BTP-Bund spread, was the main factor determining the level of the euro in 2018(Chart 5), showing that the issue surrounding the Italian budget was the main source of risk for the market.

Chart 4 – EUR/USD and 10-year BTP-Bund spread

Sources: Bloomberg, Macrobond, BSI Economics

Several factors could weigh on the US dollar:

- Uncertainty surrounding the Fed’s normalization policy is likely to weigh on the USD, and the flattening of the US yield curve could accentuate this decline.

- The real effective exchange rate suggests that the dollar remains overvalued;

- After a very expansionary fiscal policy in 2018, the expected slowdown in economic growth, the rise in the US budget deficit, and the increase in the current account deficit in 2018 and 2019 are likely to weigh on the dollar in 2019. It should also be noted that the US net external position has been deteriorating further since 2011.

In the long term, the EUR/USD pair could return to an upward trend due to the expected normalization of the ECB’s monetary policy. Some short-term stability for the EUR/USD around 1.15 seems a likely scenario, given the ECB’s cautious stance and the possible announcement of TLTROs. Subsequently, the pair could appreciate to around 1.20 once the Fed has clearly communicated to the market that it has ended the normalization of its monetary policy.

However, if markets become turbulent during the rest of 2019 with an increase in risk aversion, the dollar could benefit from its role as a safe-haven currency in the same way as the yen.

3.5) Upward volatility in 2019

A number of factors are likely to increase volatility in the equity, foreign exchange, and bond markets.

- Trade tensions between China and the United States may resurface as early as March. Although an agreement was reached between the two countries at the last G20 summit, it is only temporary. Trade tensions have already had a negative impact on the global business climate. Several investment projects have been postponed, which could further slow global growth, posing a new challenge for central banks.

- Economic uncertainty in the eurozone could exacerbate the slowdown. The main question regarding the eurozone economy is when the slowdown will end. A rebound was already expected in the fourth quarter of 2018. However, at the beginning of 2019, there are still few signs of recovery. There are fewer and fewer monetary policy tools available to deal with a slowdown, and coordinated fiscal stimulus within the eurozone would be very difficult to implement due to the European institutional and political environment. Finally, a further slowdown could be negative for European assets as well as for the EUR/USD.

- The fragility of the Italian economy, marked once again by a technical recession in the last quarters of 2018, has further moderated the current Italian coalition’s stance in its budget negotiations with the European Commission.

- Other minor risks exist, such as the uncertainties surrounding Brexit.

Chart 5 – Volatility indices

Sources: Bloomberg, Macrobond, BSI Economics

Conclusion

Between new risks of trade tensions that could weigh on global growth, ongoing political risks, and the economic slowdown, various catalysts in advanced countries could lead to a general deterioration in financial markets and increased volatility in equity, bond, and currency markets.

Central banks (Fed and ECB) remain very cautious about managing the end of the cycle in a context of economic and political uncertainty that could increase risk aversion.

[1] Foreign exchange market

[2] Consensus of economists established by Bloomberg

[3]« Hard data »: data provided by government statistical agencies, used in the calculation of real gross domestic product (GDP). « Soft data »: data provided in surveys of businesses, concerning consumer confidence, for example.

[4] Estimates based on studies of the cost of the fall 2013 shutdown and reproduced in a study by BNP Paribas. See Committee for a Responsible Federal Budget (2013), The Economic Cost of the Shutdown.

[5] Dalbard, J., Le Bihan, H., Vives, R. (2018), « The end of net asset purchases does not mean the end of quantitative easing, » Bloc-notes Éco, Banque de France

[6] However, there has been no official communication from the ECB on this subject.

[7] The downward revision of the risk assessment is seen as a first step by the ECB towards acknowledging a sharper slowdown in growth than anticipated by its services, and a revision of macroeconomic projections could change market expectations regarding possible monetary policy measures.

[8] This is the policy rate that would have no effect on an economy in equilibrium and meeting the Fed’s two objectives: full employment and 2% inflation.

[9] The term premium is the additional return that investors receive for duration risk. Duration is the period after which the yield on a bond is no longer affected by interest rate changes.

[10] 10-year German sovereign bond

Purpose of the article: The purpose of this note is to outline the various possible scenarios for sovereign bond and FX markets for the rest of 2019 and to identify the risks that could increase volatility in equity, bond and FX markets.