Relevance:This article seeks to structure the necessary public debate on the effects of a possible (and increasingly inevitable) official devaluation of the Lebanese Lira. On the one hand, the peg is unsustainable. On the other hand, the peg is necessary to maintain inflation and the purchasing power of poorer households. A devalued exchange rate will hurt sensitive group more in the short, but embeds in it the opportunity for more inclusive and sustainable growth in the medium to long run. The government has a key role to play in smoothening the transition, but the Lebanese are used to less than ideal public service provision, and might as well have to rely on private1 safety nets, yet again.

Summary:

- Lebanon is in the midst of a sovereign, banking, economic and exchange rate crisis.

- The country’s fixed exchange rate regime is a central theme to its problems, while floating it, along with a large devaluation, are one part of an increasingly likely solution.

- Lebanon also suffers from acute inequality in its income distribution –some estimates rank it at par with the most unequal countries in the world– exacerbating the resolution of the current crisis.

- A better understanding of the effects of an (inevitable?) official devaluation on the inequality is key to the sustainability of any crisis resolution.

Lebanon is in the midst of multi-faceted crisis2 that has been in the making for many years. Even before the corona crisis further aggravated it, Lebanon was in turmoil, as manifested by the eruption of social unrest on October 17, and recently culminated in the government’s default, a first in its history. At the root of the problem, a Ponzi-like scheme3 in which the government borrows from local banks at high interest rates, based on which they can attract fresh deposits at attractive rates, both from local savers and abroad. The rock on which all this scheme rests is a peg to the US dollar, that the central banks has defend since December 1997. This peg has been essential to give confidence in the Lebanese government, maintaining its borrowing costs at (high) but affordable rates, the Lira and the Lebanese economy.4

While government borrowing was absolutely necessary to rebuild the country’s infrastructure after 15 years of civil war, it had the unintended consequences of exacerbating inequality and crowding out private investment in the local productive economy.5 It is important to note that this has been going on in a context of rampant corruption that further complicates matters6.

The government is currently preparing its reform program to deal with debtors, the international community (International Finance Institutions and donor countries), and its own people. The reforms unsurprisingly include a planned devaluation of the Lebanese Lira, after the stabilization of the economic situation. Thus, it is urgent to have a transparent public debate about who will bear the costs of the default, of the restructuring of the government debt, and of the economic hardships that the crisis is going to result in.

In the absence of such debate, indirect redistribution of the economic costs will happen, through the devaluation and the implied inflation, in ways that might hurt unevenly the lower part of the distribution, and puts in serious question the sustainability and the viability of the economic recovery, on top of the instability from continuous social unrest7. Given the scale of Lebanon’s inequality,8 good public policy has never been more urgent.

1. Direct Effect of Devaluation on Inequality

The problematic of the devaluation lies in its intertemporal dimension. In order to assess its effects on inequality, and understand what is an equitable and thus a sustainable way forward, it helps to understand who benefited from the overvaluation, and who will lose most from the devaluation. As I will argue in the next section, the devil is in the detail.

1.1 Who benefited from the overvaluation? Everyone

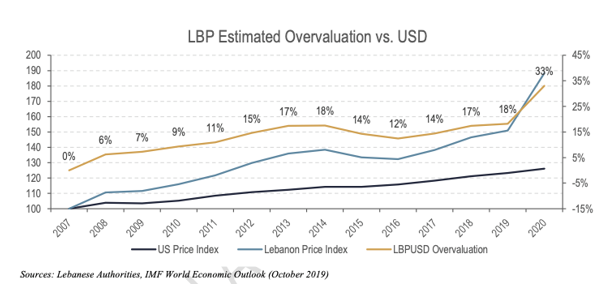

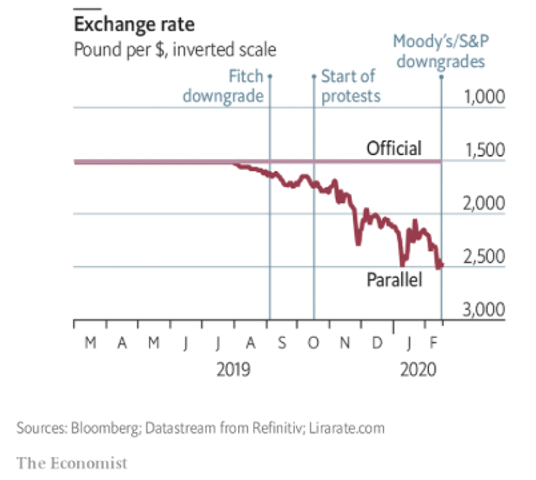

According to the Lebanese Authority’s estimates, the official Lebanese Lira rate is overvalued by 33% in 2020.9,10 These figures are optimistic, at best, with the IMF putting the overvaluation at 50 %. The reality of a future official devaluation hit with the secondary foreign exchange markets operating at an alarmingly decreasing rate, with the US dollar trading at 3950 LBP on April 25.11 All this points to years of external imbalance in Lebanon that would have inevitably lead to devaluations, and was only postponed by (socially) costly interventions from the central bank (Banque du Liban, henceforth, BDL).

It is no doubt that the peg has been the root cause of stability in Lebanon. The benefits from this stability, however, have been highly asymmetric. On the one hand, the elites could afford ever more opulent lifestyles12 due to the inflated purchasing power of the Lebanese, aggravating inequality. As The Economist puts it: “The glamorous Lebanon of tourism ads and diaspora fantasies was always a veneer. A clubgoer wearing designer labels tosses her Mercedes keys to a valet earning a few hundred dollars a month.” (April 11th 2020 Edition) On the other hand, the peg has been essential to the economy. A telling example is the dependence of Lebanon on food imports: more specifically, striking examples of domestic consumption reliance on these imports are measured by ratios of imports to consumption ratios of 80 % for major categories such as cereals (World Bank database, FAO statistics, Abou Zaki, 2020). This issue is further amplified by the fact that Lebanon is not thought by experts to be able to be auto-sufficient in food provision and that local agriculture producers rely heavily on government subsidies. This, among many other factors, have lead the World Bank (2019) to warn that poverty might hit 50% of the population.13 Drawing a picture of how the asymmetric benefits of the peg varied across in the income distribution, helps us better understand the losers from the large de facto devaluation Lebanon is going through.

1.2 Who will lose more from the devaluation?

What makes the topic of the devaluation such a thorny issue is the economic reality that while richer households had larger welfare gains from the overvalued exchange rate, poorer households will disproportionally hurt more from the devaluation. The international experience has shown that following large devaluations, the cost of living for the bottom income decile increases almost 1.5 times more than for the top income decile – based on the 1994 Mexican devaluation, two years post-devaluation (Cravino and Levchenko, 2017). The intuition behind this asymmetry is the fact that poorer households spend relatively more on tradeable goods in their consumption basket. Given that Lebanon’s economy is structurally different than Mexico’s, in that it has smaller industrial and agriculture sectors, this estimate is a conservative minimum.

A more recent and geographically closer example is that of Egypt: following its decision to float its currency, the Egyptian Pound lost half its value, inflation was soon running at 30%, hitting the buying power of companies and consumers alike.14 While the floating of the Egyptian pound was orderly, mismanagement of the flotation will prove very costly for Lebanon, in terms of possibly more devaluation than warranted, accelerating inflation, and finally a deeper recession, due to the erosion of purchasing power crippling private consumption. It is important to note that Lebanon relies heavily on imports to produce, risking an inflationary spiral, via imported inflation, leading to higher deficits, more devaluation, and again.

Further complicating the matter, households and firms have borrowed in US dollar, and this mismatch will heavily burden their balance sheets. The Association of Banks in Lebanon estimates that the dollarization rate of loans of the banking sector to the private sector (retail, commercial and corporate loans) stands at 67% at the end of January 2020. This paints a gloomy picture: absence a restructuring of private debt, households and firms will have an increasingly difficult time paying their USD denominated debt, doubly hit by the devaluation and the recession. The direct implications on inequality are not clear cut: households not at the top of the income distribution could have taken loans in USD, backed up by USD deposits from remittances. The current context means a dry up of inflows (global crises, low oil prices affecting the Gulf, mistrust due to capital controls, and lack of confidence in the banking sector, insolvent from its exposure to government debt), who would have normally helped cushion the blow.

2. Indirect Effects of Devaluation on Inequality

It is not entirely clear in the economic discipline what is the effect of the exchange rate regime on inequality (Berg and Kpodar, 2019). Having discussed the direct effects of the devaluation, I move now to a discussion of the mechanisms through which floating the exchange rate can affect inequality in the medium to long-run: those range from its effect on growth sustainability, volatility and inflation. For policy makers, it is important to remember that floating is an opportunity that comes with its own risks, and develop buffers in order to limit its distributional consequences.

- Growth

The effects of a devaluation on growth is usually positive in the medium to long-run: devaluations adjust the price of exports with respect to the price of imports, making them more attractive to both local consumers as well as foreigners. Even though the devaluation will be accompanied by a deep recession (further aggravated by the corona pandemic), a devaluated exchange rate could help the economy bounce back, after productive capacities have been given enough time to adjust.

In the case of Lebanon, the devaluation would tackle the root of inequalities: crowding out of private investment by government debt, and would correct the cumulative loss in price competiveness of local producers. Though no one expects Lebanon to become an industrial powerhouse, many among its educated multilingual workforce could benefit from growth opportunities in the tech sector or high-end manufacturing, as well as in agriculture and tourism (The Economist, 2020). The bottom line is moving from a rentier state dependent on inflows as an economic model to a productive economy will be key to address inequalities.

- Inflation

As mentioned before, the burden of the devaluation will fall more heavily on the poorer households, as their living costs increase more than better-off households. In a sense, the peg in countries like Lebanon with weak institutions, helps control inflation. Once a floating regime is adopted, fluctuations in the exchange rates will pass-through to inflation: this will have distributional effects, given that poorer households have less access to sophisticated financial instruments to hedge currency and inflation risks, and less savings to fall on to smooth their consumption. The distributional concern should be of first order to the government in its reform agenda, and a less costly policy than the peg should be put in place to protect the purchasing power of the poorest.

3. Total effects on inequality: short-run vs long-run

Thus, the effects of the devaluation have an important time dimension: in the short-run, and before the economy can adjust, the burden of the devaluation will mostly fall on the lower end of the income and wealth distribution. The interaction between the peg and the Ponzi-like scheme between local banks and the government –enabled by the peg– have resulted in dramatic levels of inequality. In the medium to longer run, floating the exchange rate is a key ingredient to the return to a sustainable and equitable growth path. This is what economic theory predicts, however the reality will depend crucially on the ability of the central bank to maintain inflation at reasonable rates (using the interest rate channel), while limiting the devaluation of the domestic currency – in the short run and on temporary basis, this could be achieved via legal capital controls, but in the medium run, by rebuilding its reserves. Given the current context of financial markets, the central bank has several options for the transition into a fully flexible exchange rate regime (a managed float or a peg with bands) or just peg at a devalued rate. The central bank should consider the liquidity and sophistication of financial markets – offering hedging instruments – in this decision, and aim at deepening Forex market, not least via proper regulation and oversight.

Conclusion

An official devaluation is inevitable, and part of the leaked draft of the government reforms. It will definitely hurt poorer households most, in a time where the crisis is expected to dramatically increase poverty rates. The government15 should not postpone any plan to float the exchange rate and use the limited central bank reserves to smooth out the transition. Floating the exchange rate will be a key ingredient in the recovery and an important factor in leading the economy to a path of sustainable and equitable growth. This, however, will come at high distributional costs, and its own set of risks, from the volatility of exchange rate and its consequences on inflation: redistributive policies should be prioritized in the reform agenda, and the capacity to withstand future shocks rebuilt.

A transparent public debate would help make the tough economic choices more accepted, and ease social pressures that would threaten the recovery.

References

Abou Zaki, S. (2020). “Lebanon needs to lower its import dependency.” Retrieved April 13, 2020, from https://www.executive-magazine.com/agriculture/lebanon-needs-to-lower-its-import-dependency?fbclid=IwAR0cXtgr4AcKKym0wV5n3PZvKc4xJDHj7rBHfQNQYdeCqhtgyIElwQJ0_Vc

Abed , G. (2016, November 18). “Egypt and the IMF: a good start, but only a start.” Financial Times. Retrieved April 27, 2020, from https://www.ft.com/content/9241b005-191c-33cb-8a73-a5ce6942d2e4

Aridi, S. (2018, February 26). “A Glimpse Into the World of Lebanon’s 1 Percent.” Retrieved April 26, 2020, from https://www.nytimes.com/2018/02/26/lens/a-glimpse-into-the-world-of-lebanons-1-percent.html

Association of Banks in Lebanon. Research & Statistics Department. The Economic Letter. January 2020. Retrieved April 26, 2020 from

https://www.abl.org.lb/Library/Assets/Gallery/Documents/Economic%20Letter%20January%202020%20new.pdf

Berg, A., and Kpodar, R. (2019). “Exchange Rate Policy and Inequality”. Banque de France Seminar presentation.

Berthier, R. (2020, April 14). “Grand Theft Lebanon”. Retrieved April 26, 2020, from https://synaps.network/post/lebanon-finance-economy-ponzi-bankrupt

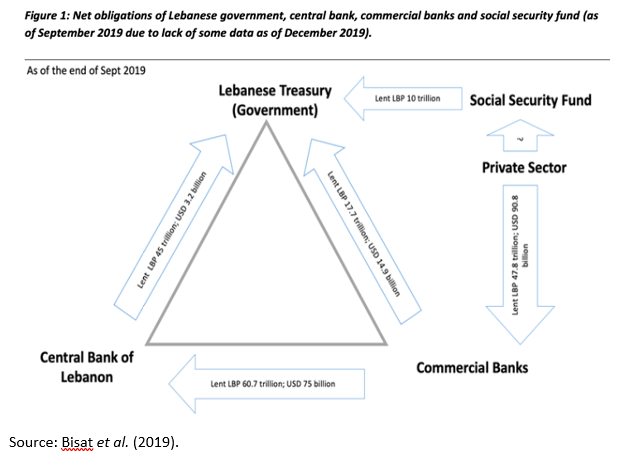

Bisat, A., Chaoul, H., Diwan, I., El Zein, S., Nader, S., Riachi, J., Saidi, N., Salti, N., Shehadi, K., Yahya, M., Zouein, G. (2019). “Saving the Lebanese Financial Sector: Issues and Recommendations”. Working Paper.

Burstein, A., and Gopinath, G. (2014). “International Prices and Exchange Rates.” Handbook of International Economics, 4th ed., 4: 391-451. Elsevier.

Chaaban, J., (2016). “I’ve Got the Power: Mapping Connections Between Lebanon’s Banking Sector and the Ruling Class”. Economic Research Forum. Working Paper Series No. 1059.

Cravino, J., and Levchenko, A. A. (2017). “The Distributional Consequences of Large Devaluations.” American Economic Review, 107 (11): 3477-3509.

Dacrema, E. (2020). “Lebanon: The Long Path to Default”. Italian Institute for International Political Studies. Retrieved from https://www.ispionline.it/it/pubblicazione/lebanon-long-path-default-25363

El-Halabi, B. (2020). “Between Famine and a Pandemic: Lebanon Is a Ticking Time Bomb.” Italian Institute for International Political Studies. Retrieved April 13, 2020, from https://www.ispionline.it/en/pubblicazione/between-famine-and-pandemic-lebanon-ticking-time-bomb-25689

Nabha, M. (2020). “Le Liban en pleine crise.” BSI Economics.Retrieved April 13, 2020, from http://www.bsi-economics.org/1115-la-liban-pleine-crise-mn

Saleh, H. (2017, December 12). “Egypt fights inflation after its currency devaluation”. Financial Times. Retrieved April 27, 2020, from https://www.ft.com/content/dc2871fe-d4f9-11e7-8c9a-d9c0a5c8d5c9

Saliba, E., Sayegh, W., & Salman, T. F. (2017). “Assessing Labor Income Inequality in Lebanon. Findings, Comparative Analysis of Determinants, and Recommendations.” United Nations Development Program and Republic of Lebanon Ministry of Finance.

The Economist. (2020). “Lebanon embraces sweatpants during the outbreak.” Retrieved from https://www.economist.com/middle-east-and-africa/2020/04/11/lebanon-embraces-sweatpants-during-the-outbreak

The Economist. (2020). “For the first time, Lebanon defaults on its debts.” Retrieved from https://www.economist.com/middle-east-and-africa/2020/03/12/for-the-first-time-lebanon-defaults-on-its-debts

World Bank. (2019). “Lebanon is in the Midst of Economic, Financial and Social Hardship, Situation Could Get worse.” Retrieved April 13, 2020, from https://www.worldbank.org/en/news/press-release/2019/11/06/world-bank-lebanon-is-in-the-midst-of-economic-financial-and-social-hardship-situation-could-get-worse

Notes

1These include: remittances, private NGOs, political parties, and the solidarity of the international community.

2A more exhaustive summary of the recent Lebanese crisis has been published in BSI Economics: http://www.bsi-economics.org/1115-la-liban-pleine-crise-mn

3 A Ponzi scheme is defined by Investopedia as: “… a fraudulent investing scam promising high rates of return with little risk to investors. The Ponzi scheme generates returns for early investors by acquiring new investors.”

4For a more detailed on the history of how the Ponzi-scheme started and the role of the peg in it, please refer to “Lebanon: The Long Path to Default” by Eugenio Dacrema. https://www.ispionline.it/it/pubblicazione/lebanon-long-path-default-25363

5In effect, banks and the top of the income and wealth distributions have been channeling their savings into profitable government debt instead of riskier investments. This has been highlighted by the study Salti (2019).

6Berthier (2020) documents the history and dynamics of corruption, using a novel datasets compiled by https://shinmimlam.com on the creation of businesses of all kinds as recorded in the commercial register. Furthermore, Chaaban (2016) documents the connections between Lebanon’s banking sector and politicians, highlighting flagrant conflict of interests.

7For a recent description of the scale of the possible social unrest, refer to El-Halabi (2020).

8A recent study by Saliba Sayegh and Salman (2017) shows that the top 2 percent of the private income distribution earns a share of income comparable to that of the bottom 60 percent.

9The official rate stands at 1507 LBP/USD. It is still the one practiced on the interbank market.

10These calculations are based on the assumption that the exchange rate of the Lebanese Lira to the US dollar was fair valued in 2007, and takes into account the differential between inflations in Lebanon and the US, as implied by the Relative Purchasing Power Parity Theory.

11 The exchange rate is quoted on www.lirarate.com.

12 The New York Times recently delved into this matter, documenting the lives of Lebanon’s top 1%: Aridi, S. (2018, February 26).

13More recent estimates by the Ministry of Finance expect the poverty rate to increase to 45%, while that of extreme poverty to 22%.

14Source: Financial Times November 18,2016 and December 12,2017.

15Lebanon is the third most indebted country in the world after Japan and Italy, with a debt to GDP ratio at 158% in 2019. It has very limited fiscal scape, making the reforms context very difficult.