DISCLAIMER: The opinions expressed by the author are personal and cannot in any way be considered as reflecting those of the institution that employs her.

This article was written as part of our partnership with ANCRE.

Following Russia’s invasion of Ukraine in February 2022, the European Union (EU) has been working to free itself as much as possible from its dependence on Russian energy sources, notably through the introduction of sanctions. After significantly reducing its imports of Russian oil and gas during 2022, by 54% and 68% respectively, and cutting itsenergy consumptionby around 18% in thesecond half of 2022, it is worth questioning the interest of European countries in continuing to reduce their energy dependence and their ability to diversify their sources of supply in the coming months and years.

The value of energy independence

In 2022, in response to the war in Ukraine, the EU gradually imposed numerous restrictions on energy imports, planning to reduce its oil imports by 90% andits consumption of Russian gas bytwo-thirds over the course of the year. Russia accounted for a significant share of the EU countries’ energy supply: 31% in Germany in 2021, 23% in Italy, and up to 98% in the most exposed countries (6% in France). There are several reasons why a government might want to become completely independent of imports from a particular country for strategic goods such as energy.

Economically, a state must be able to meet the needs of its industry in order to maintain domestic production and avoid any shortages from outside, as Germany risked this winter when it had to abandon more than half of its gas imports , which dependedon Russia before the war. Although France faced the situation in a more comfortable position, being less dependent on gas, it was nevertheless not entirely spared from difficulties, particularly due to the high share of nuclear energy in its energy mix at a time when many of its power plants were shut down for technical reasons in 2022.

Furthermore, ensuring its independence makes it possible to limit the potential for diplomatic relations to become subservient to commercial relations. It does indeed seem inconsistent for Europe to continue to purchase a significant portion of its energy from Russia, thereby financing its domestic economy on the one hand, while imposing financial sanctions on it and supporting Ukraine in its defense efforts on the other.

External supply

While most European countries have managed to break their energy dependence on Russia and gas stock levels are at their highest, it is necessary to continue the diversification effort so as not to recreate this risk with another supplier.

The advantage of geographical diversification of energy supplies includes the possibility of transferring energy from one country to another in the event of an asymmetric supply or demand shock. Having multiple suppliers offers more alternatives to compensate for a reduction in trade following such a shock. Following the imposition of sanctions, EU gas imports from Norway and the United Kingdom have surged. While these countries are considered « allies » from a diplomatic standpoint, it cannot be ruled out that a paradigm shift or external shock[3] could prompt them to limit their exports to the detriment of the rest of Europe. The tensions between Algeria and Morocco are one example, having led to the suspension of Algerian exports via the gas pipeline crossing its neighbor, which supplies Spain. In the medium term, Norway’s efforts to move away from fossil fuels in order to combat climate change could also compromise its ability to supply energy to its trading partners.

Natural gas imports from Norway (left) and the United Kingdom (right) to the EU

Source: Bruegel. Maximums and minimums are calculated over the period 2015-2020.

Avoiding this risk requires signing supply contracts with other countries, particularly in the Middle East, the Caucasus, and the United States. Between 2021 and 2022,gas imports from theUnited States doubled, while those from Qatar increased by 23%,which should ensure the sustainability of liquefied natural gas (LNG) supplies in the medium term.

However, the increase in LNG supplies is hampered by a lack of infrastructure in some countries, including Germany, which had no terminals before the invasion of Ukraine. Numerous projects have since been planned to expand capacity alongEuropean coasts.

Diversifying the energy mix

Diversifying the sources of energy consumed in Europe is also an important focus, to avoid replacing one dependency with another.

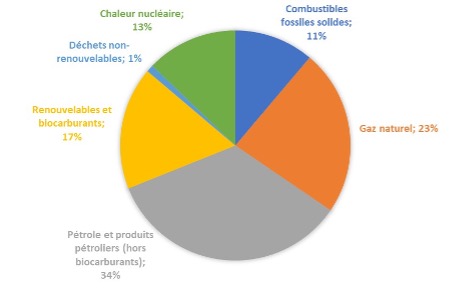

Gross available energy in Europe by source in 2021

Source: Eurostat

France, whose domestic production covers more than half of its energy consumption, particularly thanks to its nuclear power plants, has been able to mitigate the impact of sanctions on energy supply within its territory. Germany, having decided to phase out domestic nuclear energy production in 2011, was more vulnerable due to its less diverse energy mix. As a result, the increase in electricity prices in France over the whole of 2022 was limited to 7%, while it reached 20% in Germany over the same period, according to Eurostat.

In the context of the fight against climate change, the European Commission seized the opportunity presented by the Russian invasion to accelerate efforts towards energy transition and independence. Beyond abandoning Russian energy imports, the planalso aimsto significantly reduce the use of fossil fuels in its economy by increasing the production and imports of biomethane and renewable hydrogen, improving energy efficiency, and increasing renewable energies and electrification.

Furthermore, with the expected development of the emissions trading market, it will also be beneficial to diversify sources in order to limit the impact of the expected rise in carbon prices in the coming years, which will mainly affect fossil fuels. The system provides for total greenhouse gas emissions to be increasingly restricted over time, thereby increasing the price that emitters must pay to continue producing. Among the gases targeted is carbon dioxide, of which the fossil fuel sector is a major emitter and is therefore vulnerable to the reduction in quotas and the associated increase in carbon prices.

The need to go further and avoid further price increases

The benefits of ensuring energy independence through diversification of energy sources and resources are undeniable. While the efforts made in 2022 enabled Europe to get through the winter without shortages, even greater efforts will be needed in the future, especially if temperatures are not as mild, given that Russian energy is already unavailable.

However, increasing the diversity of energy sources may mean reducing the supply of the cheapest energy, thereby driving up inflation. The rise in inflation observed since the end of 2021, triggered by higher energy prices, has put the European Central Bank in a difficult position after years of fighting deflationary pressures. Inflation then spread to other sectors of the economy, raising fears of a loss of control over price stability and leading to an unprecedented rise in interest rates, against a backdrop of economic slowdown.

While the EU is seeking to develop its « green » energy sector with a view to achieving energy sovereignty, it faces competition from the United States, where the adoption of the Inflation Reduction Act raises the risk of companies relocating in order to benefit from US funds. Brussels’ response, the Green Deal Industrial Plan, has reopened the debate on the relevance of public subsidies within the EU. This policy risks, on the one hand, benefiting the largest economies and, on the other hand, being insufficient in the face of the United States’ infinite possibilities to subsidize its industries without risking market fragmentation.

The dichotomy between short-term energy needs and medium-term diversification plans is likely to continue to generate tensions between different sectors of the economy, as well as at the political and geopolitical levels, in the months and years to come. These challenges require strong coordination within the EU, which proved solid during the first year of the war in Ukraine but remains vulnerable to the slightest dissent.

[1] Source: Eurostat, imports of oil and petroleum products and natural gas from Russia to the EU by volume.

[2] Source: International Energy Agency (IEA); imports of coal, natural gas, and oil relative to total domestic consumption.

[3] For example: decision to suspend exports following a sharp decline in domestic production (such as after the destruction of production facilities due to a natural disaster).

[4] https://www.trade.gov/country-commercial-guides/france-energy-eng