Summary:

- Inflation targeting ( IT) is a framework that is being adopted by more and more central banks today: we clarify its contours;

- Many emerging and developing countries have recently adopted IT (India, Argentina) or are considering doing so (Morocco). We review the reasons that led developed countries to adopt such a framework in the 1990s: academic consensus on monetary issues, instability of money demand, failure of alternative regimes.

- In theory, IT can bring many benefits to a country (such as lower long-term inflation and reduced volatility) if it meets the necessary prerequisites (which we discuss).

- However, empirical research on the issue has struggled to confirm these effects, which we attribute to econometric difficulties.

- For emerging countries, while IT cannot be seen as a panacea, it seems clear that it can nevertheless have positive long-term effects for a country that has the necessary foundation for its implementation.

The subject is one of the current monetary policy issues in many emerging countries (Morocco, India, etc.). Understanding what inflation targeting is helps to understand the current debates and recent or future reforms in such countries.

Inflation targeting, understood here as a monetary policy framework that explicitly sets an inflation target that the central bank gives itself the means to achieve, is virtually taken for granted in economically advanced countries. However, in recent years, many emerging and developing countries have been considering adopting such a framework for their monetary policy.

India recently took the plunge in 2016 (IMF, 2017), as did Argentina in the same year (The Economist, 2016), in a different framework from the one the country is experiencing today. The aim of this article is to take stock ofinflation targeting, its theoretical advantages and disadvantages, and those observed and proven empirically, in order to share information that will help to assess its potential future scope.

IT: what are we talking about?

Inflation targeting, in the form in which it is generally understood, is characterized by the announcement of an official inflation rate target (over one or more horizons) and by the explicit recognition that low and stable inflation is the main goal of monetary policy (Bernanke and Mishkin, 1997)[1]. With this broad definition, other objectives may be recognized in the short term, such as stabilizing GDP, limiting exchange rate volatility, or maintaining financial stability.

A stricter definition of this framework, often used in academic articles for the sake of simplicity or in other contexts, is that the central bank’s quantified inflation target is its sole concern. In reality, such a policy, where no other objective is recognized either implicitly or explicitly, does not correspond to any observed reality[2].

Other intermediate definitions are sometimes considered, allowing certain central banks, such as the ECB, for example, not to officially consider themselves as inflation targeters (Issing, 2003; Paulin, 2006; IMF, 2017).

In general, central banks that have adopted an inflation targeting framework share certain characteristics :

- First, the central bank communicates extensively about inflation trends. For example, when Argentina’s central bank adoptedinflation targeting in 2016, it committed to publicly communicating its Monetary Policy Report, in which it discloses its analysis of recent and future inflation developments.

- Second, ITs generally report publicly and transparently on their activities (press conferences, reports, or hearings on their policy, etc.).

- Finally, ITs theoretically have the technical and physical means (statistical institutes, developed forecasting models) to ensure serious and minimally reliable inflation forecasts.

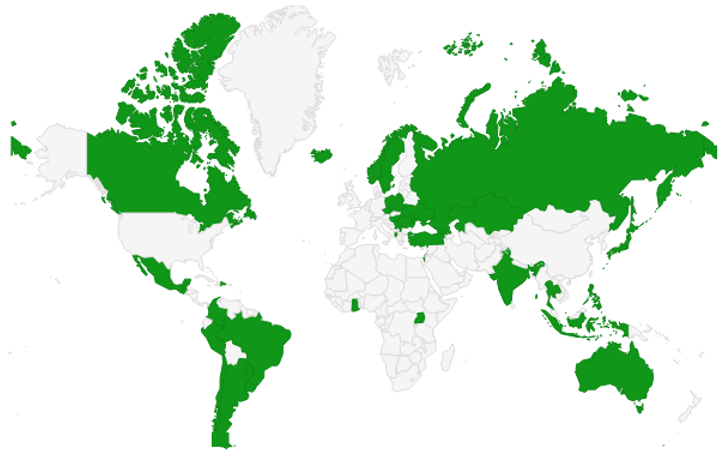

The pioneer in this field was the Reserve Bank of New Zealand, which in 1989 became the first central bank to shift its monetary policy towards achieving a specific inflation target (then between 0 and 2%). Many followed suit: Canada in 1991, the United Kingdom in 1992, followed by Sweden, Finland, and Australia in 1993. Today, the club of « inflation targeters » as recognized by the IMF includes nearly 40 countries. Figure 1 shows the countries that have declared themselves « inflation targeters » to the IMF.

Figure 1: Countries declaring themselves as « inflation targeters » to the IMF

Sources: IMF (2017), BSI Economics

All these countries apply IT with a degree of flexibility that varies from one country to another[5]: inflation targeters are a heterogeneous group.

Why did inflation targeting emerge in the 1990s?

Several factors were central to the decision of many countries to adopt this inflation targeting framework in the 1990s:

- Academic consensus on two issues. First, that monetary policy can only impact real quantities (and therefore economic growth) in the short term, and not permanently as is the case with prices. Second, the recognition of the harmful consequences of « temporal inconsistency » in monetary policy (Kydland and Prescott, 1977), to which a credible commitment to target an inflation level provided a solution[6]. This consensus played a role in making IT appear to be a relevant framework and bringing it to the forefront of public debate as a consensus solution.

- The instability of money demand: before TI, many countries targeted the money supply with the implicit idea that it had a stable impact on economic variables such as the price level. In other words, targeting the money supply was sufficient to control inflation, as monetary developments incorporated all the information needed to anticipate inflation. This relationship between money and inflation proved unstable in the late 1970s, with the emergence of significant technological innovations (creating close substitutes for money), which made monetary targeting less meaningful and made it more meaningful to target the elements on which money had a significant impact, namely inflation. This was a factor that played a key role in countries such as Canada, for example (Bernanke and Mishkin, 1997).

- The difficulties encountered by countries wishing to peg their exchange rates to a nominal value, with the case of the United Kingdom in the early 1990s being a perfect example. Alternatives had to be found to convince actors accustomed to a nominal target that monetary policy would remain « disciplined. » This is a reason cited by Bernanke and Mishkin (1997) with regard to Sweden and the United Kingdom in particular, and also by Walsh (2007).

What are the advantages?

Many advantages are attributed to an IT system:

- If credible, an IT system can bring stability to future price expectations. In countries that have experienced high inflation rates, this advantage is significant: it naturally gives people more confidence to save or invest in projects. Business planning becomes easier, which supports the development of financial markets, investment (and therefore productivity), and economic growth. It also reduces actual inflation, which partially reflects expected inflation (through the impact that the latter variable has on wages, for example). Finally, by generating a smaller response from the central bank to the same positive inflation shock (since expectations are supposed to respond less to this shock), it reduces output volatility as a second-order effect[7].

- If credible, IT also reduces financial volatility. Without a nominal inflation target, the markets and, to a lesser extent, the public remain on the lookout for what the central bank’s intentions might be. For some, the absence of a clear inflation target can create, for example, « inflation scares, » i.e., episodes where markets, following a shock to the economy, anticipate that the central bank will not react « aggressively » to inflation and therefore anticipate higher inflation. This was one of the explanations given by Mishkin (2004) to justify the relevance of an inflation target for the Fed (which it will implement in 2012).

- The IT allows attention to be focused on the price level. In this respect, it enables the central bank to:

1) Communicate clearly on a simple target;

(2) Use the IT as an « educational tool » to explain the costs of expansionary monetary policy to the public (IMF, 1997);

(3) To report more easily, particularly to the government;

(4) Reduce the risks of « fiscal dominance » (budgetary dominance[8]).

If, for example, the central bank is asked to lower rates in the run-up to elections or to finance the government, it will have to clearly explain the implications in terms of inflation, since this is its mandate. Ultimately, it will have to explain why it did not meet its target in a transparent manner. This allows the debate to focus on price levels, the only variable that monetary policy influences in the long term. Eliminating ambiguity about objectives makes it more difficult for politicians to influence the central bank. And according to some studies, by making monetary financing very limited, it even pushes the government to improve its revenue collection system (Lucotte, 2010).

- With all these advantages combined, IT could in theory enable a central bank to reduce inflation and its volatility.

What are the disadvantages?

There are very few economic analyses of the negative effects of IT for a country that would have the necessary prerequisites to adopt it. Often, the disadvantages attributed to inflation targeting stem from confusion about its definition and refer to inflation targeting in its strict form (see above). In general, however:

- It is often criticized for inducing less flexibility (Bernanke and Mishkin, 1997), forcing the central bank to follow an overly rigid rule. This could be a problem, particularly in the event of an oil shock where prices rise sharply: the central bank would be forced to clearly sacrifice economic growth at the expense of inflation, without being able to arbitrate at a minimum. Bernanke and Mishkin (1997) refer to this as « constrained discretion. » As the authors explain, most central banks have some flexibility in inflation targeting. Some can, for example, revise their inflation target, while others, by targeting core inflation, protect themselves in part from the scenario described above. Some can also adjust the time frame over which the inflation target must be achieved, or at least in words, with the most important factor remaining the control of inflation expectations.

- Some criticize it for encouraging non-transparency (Benjamin Friedman, 2004) by focusing attention on price levels. Friedman, for example, believes that central bankers may use monetary policy in part for other objectives without explicitly reporting it, thereby concealing their real concerns. For him, clearly recognizing short- or medium-term concerns about GDP allows the central bank to explicitly admit them when they are relevant to central bank decisions.

- He is sometimes criticized for implementing this in the form of inflation targeting rather thanprice level targeting. With the latter system, too rapid a rise in prices in one year is offset by a smaller rise in prices the following year. With the latter system, the excessively rapid increase is not offset. This implies greater volatility, particularly for companies’ future price forecasts. A price level targeting system would also potentially have certain advantages in the event of a deflationary shock (see Hatcher and Minford, 2014).

- It has been criticized for giving central bank governors too much incentive to focus solely on the desired inflation figure and to overlook other objectives at times when they should be important (Walsh, 2009). Jézabel Couppey-Soubeyran often notes, for example, that before the crisis, central bankers felt less invested in financial stability issues, even though these were often part of their mandate (e.g., Couppey-Soubeyran (2012)).

Empirical evidence

On the empirical side, the results remain mixed. Some studies show that inflation targeting has reduced inflation in countries that have adopted it. Others, using different methods or samples, argue that the effect is not due to inflation targeting per se but to other factors (political and societal) that surrounded its implementation at the same time, or find no effect. The evidence also does not allow for a clear conclusion on the impact of inflation targeting on inflation volatility. In general, econometric analysis that would allow for solid conclusions on this point is very difficult to conduct for a variety of reasons, which may explain the diversity of results.

Ultimately, perhaps the only empirical evidence of the success of inflation targeting in its broad form is the fact that no country that has adopted this framework has abandoned it to date.

Why would an emerging or developing country adopt IT today?

First, a country has an interest in adopting inflation targeting only if such a framework actually gives it an advantage over its current framework. Most emerging or developing countries often follow either a monetary targeting regime (where the growth of monetary aggregates is targeted), or a kind of intermediate regime that does not meet the general definition of IT given in this article but is concerned with inflation and growth, or a regime where the exchange rate is relatively fixed against one or more currencies. Countries with fixed exchange rates are often forced to adopt such a regime. Currencies such as the dollar or the euro are very present in their economies and banking systems, and exchange rate movements can therefore cause significant damage. Such countries therefore do not seem to have a direct interest in adopting an inflation targeting regime. For countries using the other two regimes described above, the adoption of IT is generally open to debate. The only question that seems to arise is that of prerequisites.

Different economists will give different answers on the prerequisites for adopting IT (see the article by Amatoa and Gerlach (2002) on this point). However, a minimum requirement seems to be that the central bank has the means to meet the target set for it. This means, first of all, that it has the means to identify the factors and channels behind price movements. It also means that it is able to use its instruments to influence the key variables behind inflation. The first element implies the existence of both statistical infrastructure and sophisticated forecasting models. The Moroccan central bank is currently working on thissecond point in order to move towards such a system (IMF, 2018). The second element requires the existence of a minimally developed banking and financial system. It also requires that the central bank have a certain degree of independence in choosing its instruments, and that the government exercise a minimum of fiscal discipline (to prevent episodes of debt monetization) and not rely on the central bank as a source of revenue. A consensus that low inflation should be the primary goal of monetary policy is an essential prerequisite for a country to adopt IT and carry out its mission.

Conclusion

Inflation targeting seems to have convinced many developed countries to adopt it, and appears to be winning over a growing number of emerging countries. The advantages of such a framework are, in theory, numerous, even if researchers struggle to demonstrate them empirically, which we have attributed in this article to difficulties that are mainly econometric in nature.

For emerging or developing countries, IT is often seen as a framework with many advantages. By officially establishing inflation as the primary objective of monetary policy, it would create a fruitful dynamic. It would also enable the central bank to build credibility and, in theory, by focusing the debate on inflation and communicating transparently, reduce the likelihood of fiscal abuse by the state.

While the decision to adopt an IT regime must be made on a case-by-case basis, it nevertheless appears that emerging countries (such as Morocco, discussed here) that seek to move towards such a system by ensuring the necessary prerequisites are in place are more likely to reap significant benefits than to incur serious costs.

The author would like to thank Peter S., Victor Lequillerier, and Marc Pourroy for their comments and discussions, which were useful in writing this article.

References:

Amatoa and Gerlach (2002) “Inflation targeting in emerging market and transition economies: Lessons after a decade”. European Economic Review

Alpanda and Honig (2014) “The impact of central bank independence on the performance of inflation targeting regimes.” Journal of International Money and Finance

Bernanke (2004) “Remarks by Governor Ben S. Bernanke At the meetings of the Eastern Economic Association, Washington, DC. The great moderation.” February 20, 2004

Bernanke and Mishkin (1997) “Inflation Targeting: A New Framework for Monetary Policy?”. Journal of Economic Perspectives

Brito and Bystedt (2010) “Inflation targeting in emerging economies: Panel evidence”. Journal of Development Economics.

Couppey-Soubeyran (2012) “Central banks facing the post-crisis challenge.” CEPII.

IMF (1997) “The scope for inflation targeting in developing countries.” IMF Working Paper WP/130

IMF (2017) “Inflation-Forecast Targeting for India: An Outline of the Analytical Framework”. IMF Working Paper WP/17

IMF (2017) “Annual Report on Exchange Arrangements and Exchange Restrictions.”

IMF (2018) “Morocco: A Practical Approach to Monetary Policy Analysis in a Country with Capital Controls.” WP/27

Issing (2003) “Inflation targeting: a view from the ECB”, speech at the St. Louis Symposium on October 16/17.

Kydland and Prescott (1977) “Rules Rather than Discretion: The Inconsistency of Optimal Plans.” Journal of Political Economy.

Hatcher and Minford (2014) “Inflation targeting vs price-level targeting: A new survey of theory and empirics” Vox column.

Lopez-Villavicencio and Pourroy (2017) “IT countries: a breed apart? The case of exchange rate pass-through.” HAL Working Paper.

Lucotte Yannick (2012) “Adoption of inflation targeting and tax revenue performance in emerging market economies: an empirical investigation” Economic System.

Mishkin (2004) “Why the Federal Reserve Should Adopt Inflation Targeting”. International Finance.

Svensson (1997) “Inflation targeting in an open economy: Strict or flexible inflation targeting?”

The Economist (2016) “Argentine central bank adopts inflation targeting regime”

Walsh (2007) “Inflation Targeting: What Have We Learned?”. International Finance

Further reading:

The history of inflation targeting in New Zealand (the pioneer in this field): https://www.rbnz.govt.nz/research-and-publications/speeches/2018/speech2018-04-12

Freedman and Laxton (2009). “Why Inflation Targeting” IMF Working Paper

Knight (2007) Inflation targeting in emerging market economies

Mishkin (1999). “International Experiences with different monetary policy regimes” NBER Working Paper

[1]There is considerable debate about what exactly definesinflation targeting and whether it represents a monetary policy regime in its own right. We will not delve into this debate in depth in this article, but interested readers may consult the end of section 2 of the IMF article (1997).

[2]Some, such as Svensson, refer to this definition as “strict” inflation targeting, as opposed to the “flexible” inflation targeting regime corresponding to the first definition.

[3] Some consider an intermediate definition of inflation targeting, where, in addition to placing the price stability objective at the center of monetary strategy, forecasts of future inflation must play a central role in the monetary policy of the inflation targeter: the central bank bases its decisions primarily on its inflation forecasts (Issing, 2003; IMF, 1997)

[4]The fact that the ECB communicates that it considers a « range of factors » in its assessment of price developments and gives prominence to the analysis of monetary aggregates in its « two-pillar » strategy provides it with a basis for not adhering to the intermediate definition of an inflation targeter given here. In reality, it is difficult to understand why a central bank such as the ECB would not be an « inflation targeter » when banks such as the BoE and the Bank of Canada consider themselves to be so. A former senior international monetary policy official interviewed on this point for this article did not have an answer. It seems to be more a question of form and communication than substance. Generally speaking, since central banks include an inflation target among their main objectives, inflation targeting seems to be more of a label that central banks assign themselves for communication purposes than a designation that they automatically fall under. This paper fromthe Bank of Canada, for example, considers that since 2012 the Fed has fallen into the same category of « inflation targeting » as the Bank of Canada, which declares itself as such.

[5]Generally speaking, the credibility of the central bank prior to IT allows it to have greater flexibility without unduly hindering the effectiveness of its policy (IMF, 1997).

[6]It would be more accurate here to speak of a quasi-consensus, given that a few economists have raised counterarguments on certain points related to these debates. See IMF (1997) for a discussion.

[7]For a very interesting debate on the size of shocks within and outside inflation targeting regimes, see Bernanke (2004) (section entitled “changes in monetary policy could conceivably affect the size and frequency of shocks hitting the economy”). On the impact of exchange rate movements on inflation within and outside inflation targeting regimes, see Lopez-Villavicencio and Pourroy (2017).

[8] See the BSi article on this subject: http://www.bsi-economics.org/125-??-fiscal-dominance-vs-monetary-dominance-de-quoi-parle-t-on

[9]For a review of the literature on this empirical research, see, for example, Alpanda and Honig (2014).

[10]As inflation targeting is generally accompanied by other reforms, it is difficult to isolate its impact per se. Another difficulty stems from the fact that the economic structure, and therefore the link between economic variables, is theoretically changed with a change of regime such as the adoption of inflation targeting (a simple application of Lucas’s famous critique), which complicates econometric analysis. This last point is, for example, left out of the latest major study by Brito and Bystedt (2010). The fact that different shocks affected economies before and after the adoption of IT can also complicate the implementation of certain econometric methods. Furthermore, the effect of adopting IT on economic performance may be non-linear and take time (IMF, 1997): this factor is overlooked in most studies. Another issue relates to the very definition of inflation targeting and non-inflation targeting: comparative studies often confuse the two. And then there are, of course, the recurring problems of selection bias and the potential analysis of a counterfactual.