Summary

– The creation of the European Economic and Monetary Union helped the least advanced member economies catch up between 2000 and 2008.

– Since 2008, this momentum has been interrupted. Divergences have reappeared between the economies of the eurozone because the construction of EMU carried within it the seeds of profound macroeconomic monetary and financial dysfunctions (changes in real exchange rates, inflation, labor costs, and the real cost of debt for economic agents).

– In this article, we will attempt to identify the key points of these dysfunctions and determine whether the divergences they have caused are fading thanks to the eurozone’s crisis exit strategy (governance reforms, fiscal support, accommodative monetary policy).

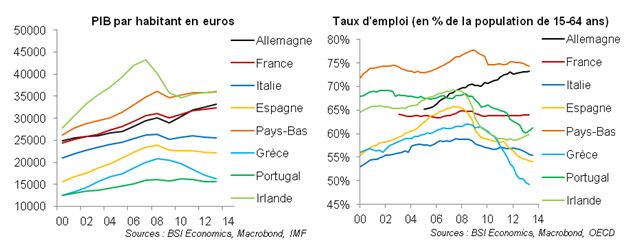

The eurozone is made up of economies that each have their own characteristics. Initially, the goal of convergence was to enable the less prosperous economies of the monetary union to catch up with their more advanced partners. Despite significant structural differences, the early 2000s were a success in terms of convergence in economic activity, with accelerated GDP growth and rising employment rates in peripheral countries.

Unfortunately, this seemingly positive dynamic of convergence in Europe in terms of economic output was accompanied by multiple imbalances: monetary, financial, external, and economic. It is these imbalances, the extent of which we will attempt to assess in turn at the beginning of 2014, that have not only destroyed this convergence dynamic, but have also widened the gaps in GDP per capita within the EMU, which today shows a very high level of convergence between its members.

Aware of the extent of the imbalances that exist in the Monetary Union, European leaders have undertaken significant changes in governance and supervision. The adoption of the Six Packs-Two Packs-TSCG triptych has strengthened the power of the European Commission, broadened the scope of macroeconomic framework, and established a timetable. The Banking Union project provides for the centralization of regulatory, supervisory, crisis resolution, and deposit guarantee powers at the Eurozone level, with the ECB at the center of the game.

In this article, we will attempt to determine whether this work on governance and economic policies undertaken at the national level in the eurozone has helped to stem the mechanisms of divergence that have emerged since 2008. To do so, we will examine the evolution of key variables in the Eurozone crisis: public finances, balance of payments and competitiveness, financing of the economy and agent indebtedness in eight countries: Germany, France, Italy, Spain, the Netherlands, Greece, Portugal, and Ireland.

1 – Public finances

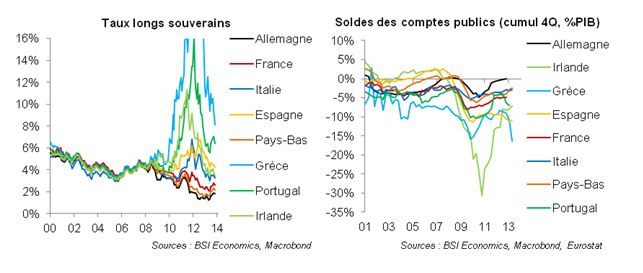

The Eurozone sovereign debt crisis that has been raging since 2011 is characterized by a sharp deterioration in public balances and a rapid increase in the levels of public administration debt. The dynamics of this public debt in Europe have raised doubts about the solvency of peripheral countries in particular.

Since the creation of the eurozone, cases of balanced or surplus budgets have been rare. Despite this, the period of relative economic prosperity that followed the birth of EMU made it possible to limit the dynamics of public debt, the main measure of which is its ratio to GDP.

Financing public deficits was easy at the time, and borrowing conditions on the financial markets were favorable. EurozoneEurozone countries were extremely homogeneous; in 2007, for example, Greek and German long-term rates were identical. This homogeneity did not withstand the financial crisis. However, the peak of tensions on the sovereign debt markets reached in 2011-2012 seems to have passed thanks to the measures taken to compress long-term rates. Although differences remain (which is justified by the financial situation of each country), Italian and Spanish interest rates in particular have fallen back to their pre-crisis levels and are no longer unsustainable. At the same time, the significant rise in German, French, and Dutch rates leads to the conclusion that, overall, there is a return to convergence on this point.

On the fiscal front, the European Commission’s more flexible stance on public balance trajectories has shown that structural efforts should not be undermined by excessive economic downturn. On this point, we can therefore say that the return to fiscal balance is underway and that the eurozone has armed itself with a coherent and credible crisis exit strategy, giving itself the institutional means (significant strengthening of the role of the European Commission) to achieve this objective.

2 – Balance of payments and competitiveness

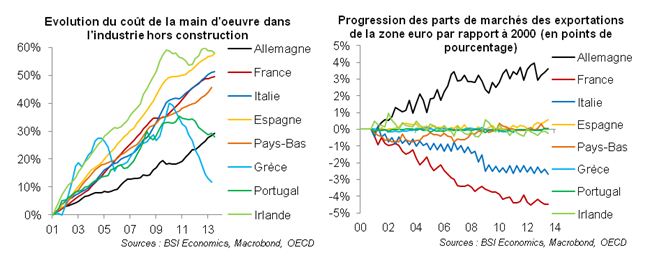

The early years of EMU saw multiple shocks that were very unfavorable to the current accounts of some eurozone countries. On the one hand, differences in price levels, real effective exchange rates, and labor costs penalized exports and stunted the economies of export sectors. On the other hand, economic convergence (and its impact on prices and wages) and the easing of credit conditions thanks to unified money markets stimulated domestic demand and increased the level of imports.

The ease of financing current account deficits between EMU countries and the absence of economic policies capable of reversing this trend have allowed these external imbalances to persist and have contributed to the precariousness of the external positions of deficit countries.

The lack of monetary leverage to regain competitiveness made the fiscal austerity strategy compatible with external solvency constraints by reducing imports. The sharp decline in domestic demand, particularly private demand, quickly enabled the previously deficit-ridden members of the eurozone to achieve current account balance.

This return to balance in external trade with their monetary partners and the rest of the world for most Eurozone economies is therefore mainly the result of a contraction in their activity and domestic demand. Ultimately, it requires the implementation of industrial economic policies capable of promoting export activities.

3 –Financingthe economy and the indebtedness of economic agents

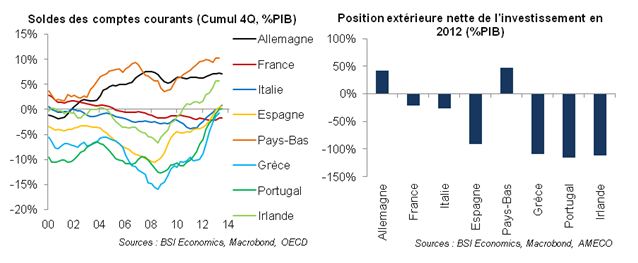

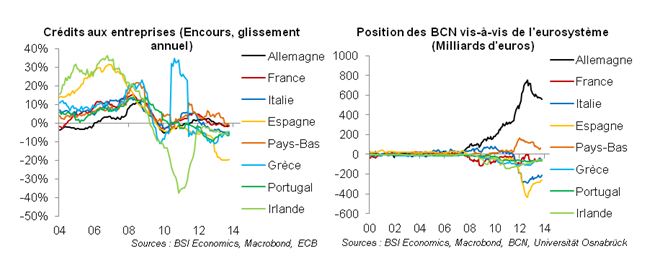

Transnational financial flows between Eurozone countries have been facilitated by the creation of the Eurozone. As we have seen above, their significant increase has made it possible to finance the current account deficits of certain countries without creating monetary problems, and to facilitate access to credit and private debt.

The domestic reflux movements of creditor economic agents from 2008 onwards materialized the risk of financial disintegration following the loss of confidence in the peripheral countries of the eurozone. Their significance is commensurate with the internal dysfunctions of the eurozone, and their consequences for the financing of the economy have been manifold: credit crunch, forced deleveraging by private agents, and divergences in their conditions of access to credit.

Although we are seeing the beginnings of a return to equilibrium in the positions of national central banks vis-à-vis the Eurosystem, the current state of these positions and the size of the amounts involved clearly show that the financial reintegration of the EMU will be difficult (see the BSI Economics article on Target 2 balances). The ECB’s accommodative monetary policies (LTRO, VLTRO) in favor of banks have not enabled the struggling economies of the eurozone to escape the phenomenon of credit rationing.

With credit supply becoming scarcer and lending conditions tighter, the financing of private investment and consumption, which in Europe is overwhelmingly provided by banks, has been blocked, contributing to the fall in private debt. As we have seen above, this is not the case for public debt.

Conclusion

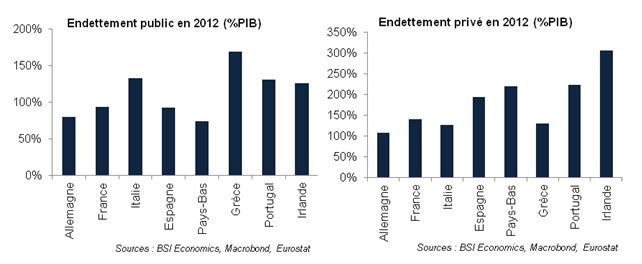

Many imbalances remain between eurozone countries, largely due to the shortcomings of our economic and monetary model (divergences in inflation and real interest rates, labor cost trends and real exchange rates).

The institutional (economic governance reforms) and financial (fiscal support, accommodative monetary policy) measures implemented to remedy this situation are beginning to bear fruit: long-term sovereign bond yields have returned to sustainable levels, and the path towards balanced public accounts, and above all current accounts, has begun.

However, the uneven conditions of access to financing for private agents and the very precarious financial situation of several European countries (notably Spain, Greece, Italy, and Portugal) remain problematic for the return of economic growth.

The notable improvements that have been seen therefore need to be confirmed in order to determine whether the eurozone can once again become a tool for convergence and long-term economic development.