Employee share ownership: boosting employee savings through stronger tax incentives for companies (2/2)

Summary:

– Since its creation, employee savings have undergone numerous legislative changes, both major and minor, which have improved its functioning but also disrupted employees’ understanding of the system.

– Nevertheless, there appears to be a constant desire to stabilize and perpetuate these schemes.

– The current five-year term is no exception to the rule, and employee savings are once again the subject of debate, particularly in the context of the Macron law on growth.

– In a difficult budgetary context, the aim is to redirect savings flows towards financing the economy.

In a previous article , we laid out the basics for understanding how employee savings work. It seems difficult to change the rules on such schemes, given their various implications for the economy. However, employee savings are constantly changing, which also makes them difficult to understand. Their overhaul appears necessary in view of their stagnation in 2014.

Recent legislative developments in employee savings

These schemes have always been subject to various legislative changes, making the system difficult to understand. Since the ordinance of January 1959, these laws have initiated and improved the sharing of profits and savings at the collective level in order to stabilize the company’s capital. Some of these changes, and sometimes a little opportunism, have weakened a system that is nevertheless viable. Hence the need for reform.

The latest wave of changes, which was no exception to the rule, dates back to 2001-2008. In 2001, the Fabius law initiated a genuine social project by introducing pension funds and thus creating a voluntary long-term employee savings plan as a supplement to retirement pensions. It imposed new forms of investment in the social and environmental fields. This allowed for tax-deductible employer contributions, exempt from social security contributions. The aim was to encourage small businesses to enter the employee savings system through a tax exemption mechanism. The results for small businesses were mixed, hence the more recent concerns.

Since 2006, other exemption measures have been added, such as lower taxation for taxpayers subject to the ISF (wealth tax), lower social security contributions on withdrawal of savings, etc. However, this only applies to profit-sharing in the form of employee savings; if the profit-sharing is paid directly in cash, the exemption does not apply. Finally, 2008 saw the creation of COPIESAS (the Advisory Council on Profit-Sharing, Incentive Schemes, Employee Savings, and Employee Share Ownership), but it only began operating last June when it was commissioned to produce a report for the Macron law, symbolizing the slow pace of change. At the same time, in November 2014, the IPS[1]think tank published a white paper in connection with the responsibility pact, proposing solutions to secure, streamline, and perpetuate this employee savings system.

But let’s return to COPIESAS, an organization that brings together experts, social partners, and institutions. The aim of this committee is to act as a lever on corporate management and improve the financing of the economy. It places less emphasis on the fundamentals of the system, namely building employee savings with the help of companies. Their report was published on November 26, 2014, and includes 31 proposals for expanding and simplifying employee savings with a view to improving the financing of the economy and the governance of its companies.

The report’s guidelines are: to simplify its mechanisms, develop employee savings in SMEs and micro-enterprises, and contribute to the financing of the economy. Within the framework of the LOLF (Organic Law on Finance Laws), the Senate had planned to accelerate the abandonment of a measure from Sarkozy’s last reform, which had been called the « dividend bonus » because of its unequal nature. This preliminary report is intended to lay the foundations for reform and prompt a comprehensive review aimed in particular at harmonizing profit-sharing with incentive schemes. The idea is to create a « collective performance contract » without merging the two systems. Another measure emerges from the report: if employees do not specify how they wish their profit-sharing bonus to be paid, whereas previously it was paid in cash, the current preference is for a return to employee savings. These new guidelines therefore seem to reflect a renewed desire on the part of companies and employees to develop employee savings schemes.

These various measures in the past have left a generally confused impression, but they nevertheless give way to a reaffirmed desire to stabilize and perpetuate employee savings, both socially and fiscally. The objective is therefore to orient the system towards a solidarity-based economy with diversified investments. It remains to be seen what approach to adopt and what fiscal support is needed to make this effective.

It is in this context that recent discussions on a potential update of employee savings schemes have taken place. Launched two years ago, these discussions were resumed at the Social Conference in June 2013. In particular, there was talk of a temporary release (between July and December 2013) of part of the employee savings, but only for consumption purposes in order to boost the country’s growth. The aim was to increase employees’ purchasing power for a few months by completely exempting these savings from taxation, provided that they were reinjected into the economic circuit. However, this exceptional release is only a temporary measure and can be considered harmful. It can be seen as a government incentive to substitute employee savings for wage increases, a tool particularly used by large, established companies, thereby increasing inequalities in the entrepreneurial fabric. Above all, the taxation of this release is not the same, hence the criticism of this type of decision, when the very essence of employee savings is to appear as a risk-free and stable alternative investment.

Following the presidential announcement, an inter-professional negotiation plan was launched in 2014, led by the General Inspectorate of Finance and the General Inspectorate of Social Affairs. No report has been made public to date and little progress has been made, although the main idea put forward so far is that the tax and social security framework for employee savings is undergoing constant change, with its specific tax features.

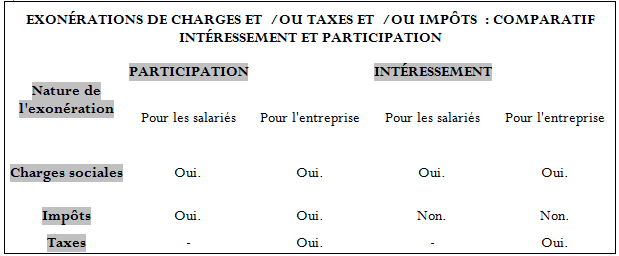

Figure 1

Sources: ComprendreChoisir, Fine Media, BSI Economics

Tax exemptions currently apply to social security contributions when matching contributions are made to an employee savings plan, but also to income tax depending on how the savings are used (only if they are invested in a plan).The problem with the development of these employee savings plans is precisely the fiscal and social uncertainty that works against them, particularly for small businesses. They are undeniably attractive, but this comes at the cost of exacerbating problems within the company, particularly through tax mechanisms.

However, care must be taken to ensure that the development of these schemes does not result in employee savings replacing salaries due to the numerous exemptions. It appears that profit-sharing is closest to salary, as the other two remain blocked for at least five years.[2]. Apart from payment ceilings, there is nothing to prevent a distortion of the remuneration structure. It is possible to reduce salary amounts in order to promote financial participation.

The primary objective of these reforms is therefore to facilitate access to these financial participation schemes for small businesses[3]without going too far in the opposite direction. It is difficult to assess the impact of these tax measures, even though they make it possible to take stock of the implementation of schemes involving employees in the company for more than 50 years. In any case, this renewed tax initiative is clearly intended to channel savings toward businesses rather than money market funds, which are a priori more attractive[4].The aim is therefore to maintain an appropriate legislative framework while simplifying its implementation.

Strengthening the system through tax incentives: a real challenge in the current context

The history of employee savings is in fact the history of shared capitalism, but it is not neutral for the economy due to its significant fiscal cost. On the other hand, for companies, all sums paid in respect of profit-sharing, incentive schemes, and employer contributions to company savings plans are tax-neutral: they are deductible from profits for corporate tax purposes. According to the Court of Auditors, the tax and social security exemptions associated with these participatory schemes are estimated to amount to approximately €6.5 billion (for employers and employees combined), or around 1.4% of total tax revenue in France (in 2013).As we have seen, these internal savings plans are very attractive to beneficiaries because they are pre-tax savings, i.e., investments that are not subject to income tax. Employer contributions are not subject to taxation, nor are the capital gains generated by these investments. This makes it possible to reward an employee without the increase being irreversible and subject to social security contributions for the employer. However, the incentives vary depending on how long the savings are held, because the objective that must not be lost sight of is thatthey are a means of strengthening the company’s equity capital .

The current government has announced, as part of the Macron law on growth, a comprehensive reform of employee savings schemes. As of 2015, the « Sarkozy bonus » introduced in 2011 is set to disappear[5]. This bonus was paid to employees when the company had two consecutive years of dividend increases. Its abolition will allow wealth to be distributed more equitably[6]. The aim is to implement the recommendations of Copiesas[7] to broaden and simplify profit-sharing and incentive schemes. Indeed, apart from the complexity of the various savings arrangements, the explosion in social security contributions is also a problem. The question is therefore how to make these employee savings, deposited in corporate mutual funds, more effective. However, employee savings are already the financial product with the most tax and social security privileges. The question is therefore whether it is possible to go even further. Various options are nevertheless being considered by Copiesas and the government to re-establish social dialogue:

Modulating the social security contribution so that it penalizes companies less.

Employer social security contributions on salaries, which grew exponentially between 2009 and 2012, have discouraged the choice of employee savings. The challenge is therefore to send a signal via the public authorities to encourage employee savings by adjusting tax rates and exemptions. While it was set at 2% in 2009, it has risen sharply since then, reaching 20% in 2012. This is one of the largest tax increases ever seen, which, in addition to the gloomy economic climate, did not encourage these investments and exacerbated legislative and fiscal instability, and therefore confidence in this type of scheme. Efforts are being made to adjust the flat-rate tax, but it remains a significant source of revenue that the government is ignoring in these difficult budgetary times. The application of different rates (exceptional or normal) complicates the system by weakening the possibility of strengthening equity capital through employee share ownership. At a pinch, we could consider completely exempting companies with fewer than 50 employees when the employee savings scheme is first introduced. This is in line with our second point.

Seek to reduce constraints on SMEs, in particular through targeted tax exemptions.

To do this, an appropriate profit-sharing agreement (via the social security contribution) should be established, in line with the tax credit introduced by the law of December 2008. The aim is to simplify and expand the system while affirming the principles of justice and solidarity (see the responsibility pact). The impetus has therefore already been given to roll out these measures, targeting SMEs. However, it is all the more difficult for them to grant financial benefits as they are not listed on the stock exchange. Various ideas are therefore emerging: seeking to negotiate together in a « collective performance contract, » promoting « turnkey agreements, » emphasizing inter-company savings plans, or even creating an « E savings account » that allows the sums paid in to be kept in cash for five years, with a return for the employee « slightlyabove the Livret A rate. » The aim is to provide incentives without being restrictive.

Free shares can also be a real challenge for business management, especially if they are tax-exempt.

Measures may be proposed for these schemes, especially since the taxation of stock options and free shares has already changed with the amended finance law of July 2012. The Macron law is set to further modify the taxation of these shares, which will no longer be taxed under the income tax scale but as investment securities. The allowance will then be more attractive.

In reality, taxation is not everything; we must also consider issues of governance, information, best practices, etc. In particular, there is a lack of coordination between participatory systems. The aim is therefore to consolidate the complementarity of these schemes. For example, it is considered that profit-sharing must be coupled with the PEE (employee savings plan) in order to be effective. This complementarity must be taken into account by companies through incentives, matching contributions, and communication. The literature is relatively vague in this regard: should we stabilize the legal mechanisms and benefits, or introduce differentiation and tax the mechanisms differently to optimize investments? Furthermore, there is a difference between the existing tax system and its actual use in the economy, so the aim is to provide an incentive framework for consolidating these savings, which are vital for the long-term functioning of the company. This is very much in line with the well-known trend towards simplification. In this vein, the government’s latest proposal is feedback on social security contributions on capital gains since 1997. The government has backtracked on its intention to impose higher taxes on employee savings products. Employee savings are considered to be a truly virtuous investment for the real economy.

But alongside the push for widespread and generalized employee savings, there is also the promotion of employee participation in corporate decision-making, which can play a role in investment policy. We are moving away from the traditional, individual-based system to change corporate practices more generally. This raises important issues of investment management and efficiency.

The initial reactions to the government’s latest proposals seem interesting, but they do not sufficiently satisfy the stakeholders. We should therefore note that the social security contribution must evolve, but over a period of time that does not completely eliminate the uncertainty that employees find so « frightening. » From a cash management perspective, profit-sharing will no longer be paid in cash, but half will go to the PERCO and the other half to the PEE. It could also be extended to the public sector. A savings account for very small businesses, called the E account, is also being proposed, with interest at the Livret A rate +1.5%, again with a view to preserving cash flow. Finally, training and advisory services will be offered to employees and employers to help them make the most effective use of these schemes.

Conclusion

Reforming employee savings, which is presented as a means of regulating financial capitalism, is in line with the current trend of promoting social and productive performance. It is more relevant than ever in the quest for dynamism, participation, and performance in France: innovation and value creation are the two watchwords. And yet, all successive governments for nearly 20 years have tackled this issue without conclusive results in the face of legislative inflation. The problem is that the objectives sought are multiple and contradictory: encouraging savings for retirement, releasing funds to increase consumption, seeking stability for French companies’ capital, etc.

Today, it appears to be an issue as much for the problems relating to the responsibility pact as for those of the new Macron law, the search for French-style competitiveness, the reaffirmation of the values of the social contract, the search for flexibility, the sharing of company profits between employees and companies, etc.

However, the discourse surrounding these measures is not particularly clear, either for companies or for employees. Above all, constant changes never really alter the way the system works. Furthermore, care must be taken to ensure that these measures do not become mere tax breaks. The objective is therefore clear: to strengthen legal and fiscal stability in order to meet the need for sustainable measures and fiscal commitments from the State. In the background, there is also a desire to reconcile the French people with the market economy and to abolish the image of privileged senior executives.

In conclusion, it should be noted that things are likely to change in the coming year, particularly following the publication of various reports and the evolution of the government’s growth bill.

References:

– « How can employees be involved in company performance? », CroissancePlus report Grandir ensemble, January 2011.

– « What new reforms for employee savings? », La Tribune, May 2014.

– « Increasing a company’s economic performance by improving its governance and employee participation, » monitoring note, Centre d’analyse stratégique, June 2010.

– « Employee participation and social performance: new challenges for French companies as they emerge from the crisis, » analysis note, Centre d’analyse stratégique, January 2011

– « How the government will reform employee savings, » Les Echos, November 17, 2014.

– « Copiesas wants to expand access to employee savings plans for SMEs, » l’AGEFI, November 18, 2014.

– COPIESAS report, November 26, 2014: Proposals for reforming employee savings

– Reform of employee savings: the Copiesas draft report, NatixisInterépargne, November 28, 2014.

– Employee savings reform: good but could be better, Les Echos, February 10, 2015.

Notes:

[1] Institute for Social Protection

[2] However, the 1959 ordinance had anticipated this substitution trend and prohibited it from the outset, under penalty of having to pay the contribution base on remuneration again. The problem is that this rule has been relaxed: the challenge cannot exceed 12 months, the end of the mandatory wage agreement for profit-sharing.

[3] The issue of employee share ownership is not so recent, as the laws of February 2001 and December 2006 already allowed unlisted companies to use it.

[4] Even though their appeal has declined significantly since 2013.

[5] Which worked on profit sharing, the methods for calculating the tax credit (increased to 30%) and various adjustments (particularly to the tax base).

[6] This measure had also been deemed ineffective because it did not combine well with the mechanisms already in place and, above all, was too focused on employees of large companies, who are better paid. It represented amounts of €403 million in 2012 and €340 million in 2013.

[7] A committee made up of social partners, experts, and government representatives.

[8] The idea was to tax all capital gains made through employee savings schemes at a rate of 15.5%, retroactively (since 1997). Normally, the tax rate varies depending on when the profit was made. This single rate was seen as a real cause for concern. Fearing that employees would turn away from these schemes altogether, the government withdrew its proposal.