Abstract :

· Growth in the euro area is gaining momentum, supported by strong external and domestic drivers and high levels of confidence. The long period of recovery (since 2013) has been accompanied by a steady improvement in the labor market situation.

· However, after peaking in 2017 (the highest level in 10 years), growth is expected to slow down in 2018-2019, according to the European Commission;

· The current recovery remains unusual. Firstly, it remains modest compared with past episodes of recovery, particularly in terms of private consumption. Furthermore, the closing of the output gap and the reduction in the unemployment rate have not yet been accompanied by wage increases that would support inflation closer to the ECB’s target.

In its autumn economic forecasts, the European Commission revised its growth forecasts for the eurozone upwards for 2017 and 2018. GDP growth in the eurozone is expected to reach 2.2% this year (compared with 1.5% anticipated in autumn 2016), slowing slightly to 2.1% in 2018 (+0.4 points compared with forecasts a year ago) and then to 1.9% in 2019. Growth for 2017 has been systematically revised upwards in the last four forecast exercises, a first since the 2009 crisis.

The acceleration of economic activity in the eurozone is part of a global growth trend affecting both developed and emerging countries, and is contributing to the continued decline in unemployment in Europe. Robust domestic demand in the eurozone is driving growth. Investment is picking up pace and external demand for European exports is supporting exports.

Compared with 2016, uncertainties appear to have diminished, as evidenced by high levels of household and business confidence. However, the recovery remains modest by historical standards, and the scars of the crisis are still visible (slower convergence, lower potential growth, persistently low inflation, etc.).

Table 1 – Macroeconomic forecasts

Source: European Commission

Growth in the euro area is accelerating

In the third quarter of 2017, the euro area experienced its18th consecutive quarter of growth. Growth in the euro area is part of a synchronized global growth trend, but it can also count on the support of economic policies and strong domestic growth drivers.

Growth was stronger than expected in emerging countries such as China and in countries emerging from recession (Russia and Brazil), particularly due to the rise in commodity prices. At the same time, advanced economies appear to be reaching a peak in the economic cycle. This synchronization of cycles, including investment, is supporting strong international trade, with non-EU imports expected to grow by 4% between 2017 and 2019.

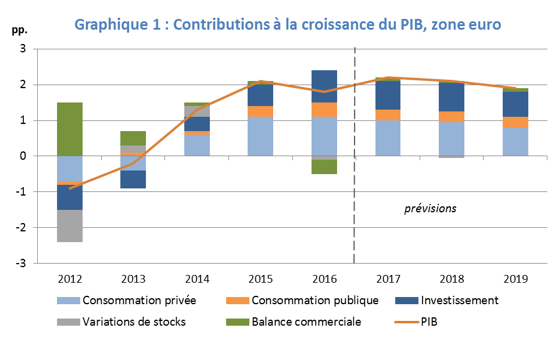

In this context, economic growth in the eurozone remains mainly driven by private consumption, which is accelerating in 2017. The continued rise in employment is supporting private consumption and partially offsetting the loss of purchasing power due to higher inflation between 2016 and 2017. In 2018 and 2019, the slowdown in the decline in unemployment should be offset by wage increases and lead to stable growth in private consumption. Investment finally appears to be picking up, supported by low interest rates and greater business confidence in future demand. Thanks to strong external demand, the euro area trade balance is also expected to contribute slightly to GDP growth in 2018 and 2019, despite the recent appreciation of the euro’s nominal effective exchange rate.

Sources: Eurostat, BSI Economics calculations

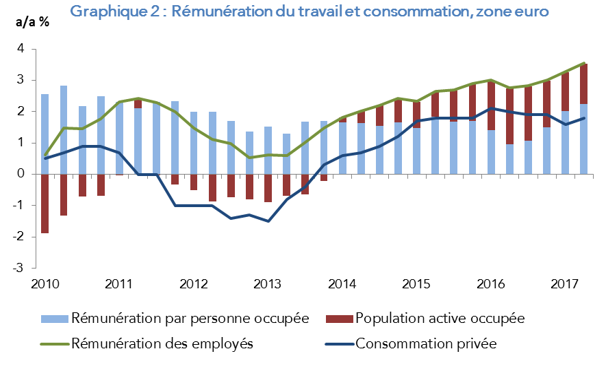

Inflation in the eurozone accelerated sharply at the beginning of 2017, reaching 2% in the spring, but has since been on a downward trend. The peak reached in the first half of the year was largely due to base effects on energy imports, while core inflation is struggling to show signs of acceleration and fell to 1.1% in October 2017 compared with October 2016, after three months of stability at 1.3%. This is due to weak growth in per capita compensation. Despite the continued decline in the number of unemployed, wages are rising too slowly in the eurozone, and many people remain in the « halo around unemployment, » which includes people in part-time or underemployed jobs, people looking for work but temporarily unavailable, and people who are available but not looking for work (discouraged workers). In total, this halo represents more than 9% of the labor force in the eurozone. Inflation in the eurozone is expected to rise to 1.5% in 2017 but slow to 1.4% next year before rising again to 1.6% in 2019, still well below the ECB’s target. The unemployment rate would continue to fall, reaching 8.5% in 2018 and 7.9% in 2019.

Strong growth momentum is also supporting the reduction of public deficits and debt in Europe. The eurozone’s cumulative deficit is expected to fall from -1.1% in 2017 to -0.8% in 2019. In France, the public deficit is expected to fall below 3% in 2017, raising the possibility of an exit from the « excessive deficit procedure » in spring 2018.

The scars of the crisis are still visible

Growth appears solid in the eurozone, economic and political uncertainties have diminished compared to 2016, unemployment continues to fall and the output gap is closing in the eurozone. However, these figures can be put into perspective to provide a more qualitative insight into the macroeconomic situation in the eurozone.

First, the current recovery appears to be modest when compared to previous post-crisis episodes. Compared to the periods 1975-1979, 1982-1986, 1993-1997, and 2009-2011, the period 2013-2017 seems to be suffering from a particularly sluggish recovery in private consumption. The first reason for this is that household debt levels are significantly higher than during previous recoveries, leaving less room for a rapid and strong rebound in private consumption. The weakness of domestic demand is also reflected in the eurozone’s current account, which has been in surplus since mid-2011.

Secondly, investment is being hampered by persistent financial and fiscal weaknesses. The deterioration in the public finances of eurozone countries during the crisis and in the quality of many banks’ assets is weighing on the recovery in public and private investment. The current recovery therefore still appears to be dependent on the support of the ECB’s accommodative monetary policy and on exogenous drivers such as lower oil prices and external demand.

Another feature of the current recovery is the apparent weakening of the relationship between unemployment and underlying inflation. While current growth in the eurozone is above its estimated potential growth, the output gap is closing, and the number of unemployed continues to fall, wages have risen by only 1.4% per year on average since mid-2013, compared with 2.5% per year between 2004 and 2008.

Sources: Eurostat, BSI Economics calculations

Admittedly, the majority of jobs created since 2013 have been in lower-productivity sectors, where wages and employee bargaining power are weaker. However, this seems to explain only a small part of the phenomenon. The European Commission study estimates that low productivity gains do indeed have a negative but marginal impact. Conversely, inflation expectations appear to be strongly influenced by the long period of low inflation.

Beyond the models, we can also look for effects in the transformations of labor market structures in Europe in recent years. Greater international competition through global value chains, the precarious nature of new jobs created (fixed-term contracts, involuntary part-time work, etc.) and the weakening of trade unions’ bargaining power following labor market flexibility reforms also appear to have contributed to the recent weakness in wage growth in the euro area.

Conclusion

The European Commission has revised its growth forecasts for 2017 upwards for the fourth consecutive time, a first since the crisis and a sign of a genuine acceleration in growth. However, the outlook for 2018-2019 seems to indicate that growth in the eurozone peaked in 2017, driven by continued strong private consumption, a genuine recovery in investment, and dynamic external demand.

Nevertheless, the recovery since 2013 appears modest when compared to other episodes of economic recovery in the past. This is due to the high levels of debt among households, businesses, banks, and governments, which limit the scope for maneuver in terms of consumption, investment, and fiscal policy. Furthermore, despite the continued decline in unemployment, wages in the eurozone are rising more slowly than before the crisis, and inflation (particularly core inflation) remains low. Although seemingly robust, economic activity in the eurozone remains fragile and heavily dependent on the support of the ECB’s accommodative monetary policy.

Bibliography:

· European Commission (DG ECFIN), European economic forecast – Autumn 2017, October 2017, Institutional paper 63, Brussels

· European Commission (DG ECFIN), European economic forecast – Spring 2017, May 2017, Institutional paper 53, Brussels