News: The ECB’s monetary policy meeting on December 8 will be a major event. The monetary authority is expected to make a series of announcements concerning the evolution of its monetary policy in 2017.

Why does the ECB need to announce new measures on December 8?

Three factors are likely to prompt the ECB to adjust its monetary policy.

First, its quantitative easing (QE) program is set to continue « until the end of March 2017 or beyond if necessary. » However , inflation, expected to be around 1.3% in the middle of next year, is likely to remain well below the target in 2017 and 2018. An extension of QE therefore seems necessary, especially since, as March 2017 approaches, a lack of announcement from the Frankfurt-based institution could have caused tension in the markets and led to an undesirable tightening of financial conditions.

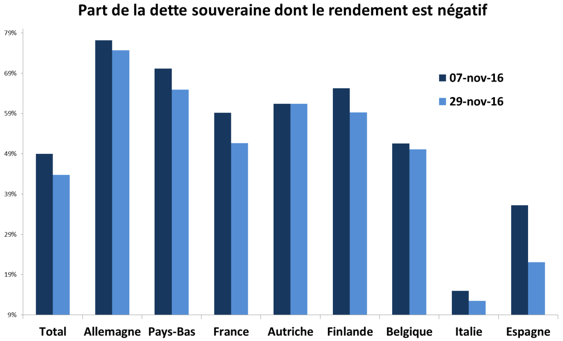

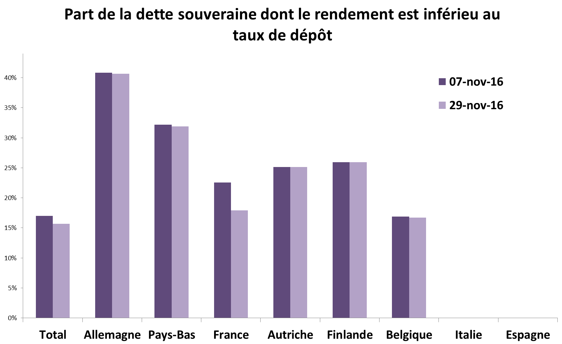

Secondly, the ECB must modify the parameters of its QE program to ensure its sustainability. From mid-2017 onwards, it risks facing a shortage of eligible treasury bills, particularly for Germany, Finland and Portugal, due to the constraints associated with QE (prohibition on purchasing securities with yields below the deposit rate, 33% limit per issue and sovereign issuer, and allocation of purchases according to the capital key). The recent rise in rates has certainly reduced the proportion of sovereign securities with yields below the deposit rate. However, it has also led to a fall in the prices of these securities, enabling the ECB to acquire a higher nominal amount for the same purchase volume, at the risk of reaching the limits more quickly. The ECB’s purchases are also high compared with issues. At the current rate, the Eurosystem is acquiring some €190 billion per year in German securities, including nearly €130 billion in sovereign debt. By comparison, German issuance is expected to be €154 billion in gross terms and -€16 billion in net terms in 2016. This exacerbates the shortage of risk-free assets in a context of excess demand for this type of security[1].

Finally, the benefits of monetary heterodoxy tend to be diminishing, unlike their costs. Negative interest rates and the phenomenal flattening of yield curves have penalized banks’ profitability and increased the cost of their capital. They would pose a threat to the balance sheet stability of insurers and pension funds if they were to persist. The ECB will have to adjust its policy in order to minimize the harmful effects and improve transmission.

Sources: Bloomberg, PBF, BSI Economics

Sources: Bloomberg, PBF, BSI Economics

What might the ECB announce on December 8?

It would be best for the monetary authority to seek to maintain an exceptional level of monetary support in 2017, while maximizing the flexibility of its QE program and minimizing its side effects. With this in mind, the ECB should:

1. Strengthen its forward guidance: To avoid any volatility, Mario Draghi should adopt a very accommodating tone and strengthenforward guidance to reassure markets that monetary support will continue.

2. Maintain constant reference rates: It also seems highly likely that benchmark rates, which have reached an « economic floor, » will be kept at their current levels and will not be lowered further unless there is a major shock to growth, inflation, or exchange rates.

3. Strengthen credit easing: This strategy could be stepped up to stimulate still-hesitant credit growth, for example by extending TLRO operations beyond March 2017, lengthening their maturity, or including real estate loans in the benchmark calculation.

4. Extend QE: QE is likely to be extended by six or even nine months, until December 2017, just after the German elections. The ECB should seek to maintain its presence in the markets, which acts as a safety net for investors (the famous « Draghi put »), particularly in a year with numerous elections. This will have the merit of continuing to reduce the cost of sovereign debt for countries whose debt remains stratospheric, and of alleviating the need for fiscal adjustment measures.

How would the parameters of QE be changed?

1. The allocation key: Abandoning the current allocation rule seems difficult given the institutional configuration of the eurozone. However, the ECB could allow itself occasional deviations from this allocation key.

2. The deposit rate: Occasional purchases below the deposit rate seem more likely than abandoning this rule, which could push short-term rates down by removing the indicative floor.

3. The purchase limit: An increase in the purchase limit to 50% for issues without collective action clauses (CACs) or AAA-rated issuers also seems likely.

4. Other measures: The ECB has demonstrated significant capacity for innovation. The probability of unanticipated measures remains high. Certain exotic options, such as the acquisition of bank debt or rate targeting, as practiced by the BoJ, seem very difficult in the current institutional configuration of the eurozone.

Is a reduction in the amount of purchases likely?

Technical adjustments and rising rates should allow the ECB to buy some time. Nevertheless, a reduction in the amount, the famous « tapering, » seems likely for two reasons:

1. The degree of unconventional monetary support justified by zero inflation is not the same as that required for inflation slightly above 1%.

2. The cost-benefit analysis of unconventional monetary policy would argue for a reduction in the intensity of support.

Nevertheless, tapering that is openly acknowledged could lead to an undesirable tightening of financial conditions. But the ECB has a very broad capacity for innovation. Thus, any tapering could be offset by replacing the calendar-based approach to QE (« until March 2017 ») with a data-dependent approach ( until inflation reaches X%), a process similar to that of the Fed. The ECB could also carry out a disguised tapering. For example, it could include the reinvestment of maturing securities in its portfolio, which should begin in March 2017, in the overall purchase envelope. It could also remove the reference to a monthly amount and replace it with an annual envelope, the execution of which would be adjusted according to changes in data or market conditions. Some form of reduction in the amount of purchases could occur as early as December. However, it is also possible that the ECB will postpone this announcement until January or March 2017 to avoid any market volatility. Have the markets already factored this possibility into their pricing? Nothing is less certain, hence the difficulty of the communication exercise that the ECB will have to undertake in December and over the coming months.

[1] See Safe Asset Scarcity and Aggregate Demand, Caballero, Farhi and Gourinchas, January 2016, https://ideas.repec.org/a/aea/aecrev/v106y2016i5p513-18.html