Abstract :

· Equity capital continues to strengthen in the recent period, but at a slower pace than in previous years;

· The capital requirements of growth companies appear to be relatively well covered by venture capital;

· The venture capital and development segments appear to be relatively well developed in France, but in the downstream segments and for large-scale transactions, France still lags significantly behind other major markets;

· It seems important to encourage the emergence of larger funds in order to meet future challenges.

.jpg)

After a slight downturn in 2014, the venture capital market (supporting the growth of innovative companies that are either newly created or not yet profitable) returned to growth in 2015 (see a previous article reviewing the state of private equity in France on the BSI Economics website). However, the venture capital segment remains largely dependent on public intervention, due to the structuring effect of Bpifrance on the upstream segments of private equity and the introduction of tax incentives favorable to the financing of SMEs, particularly innovative ones[1].

Nevertheless, several challenges remain. These include:

– Support and development of innovative SMEs and mid-cap companies[2]: The small size of the funds does not allow them to invest very large amounts. However, large-scale investments in venture capital/technological development in the « downstream » phase are an essential alternative to enable French companies to become global leaders.

– Integration and attractiveness of the European private equity market: a cross-border strategy would enable managers to benefit from a wider flow of business;

This note attempts to clarify the qualitative and quantitative challenges facing the private equity market.

1) Companies’ equity capital requirements still quite difficult to determine

Determining the equity financing needs and potential shortfall of SMEs remains difficult because, while estimating these needs requires simultaneously assessing the supply and demand for equity capital, only the result is observed. In its report on the financing of businesses and the French economy[3], Paris-Europlace estimates the intermediary equity capital needs of French companies at around €15 billion in 2015.

When compared to debt, the level of equity provides an indication of a company’s robustness and its ability to withstand external shocks. The Banque de France[4] estimates a company’s equity needs as the amount of equity required to reduce its debt to a ceiling of 200% of its equity[5]. This would thus constitute an accepted standard for concluding that the debt incurred by this company is sustainable in the medium term. In the SME segment, it estimates an additional need of €19 billion in total.

This calculation must be interpreted with caution since, on the one hand, certain sectoral and organizational specificities allow for different levels of sustainable debt; and on the other hand, this approach leads to treating very different companies in the same way: companies in difficulty that have used up a significant portion of their equity and companies that have a potentially high need for equity (for growth, etc.). For the latter, in addition to providing collateral for creditors, equity also serves to finance part of their investments.

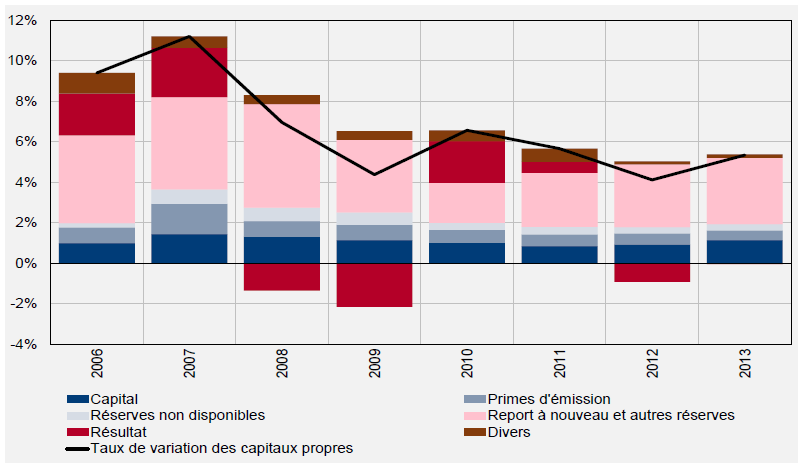

More specifically, SME equity capital grew by an average of €10 billion per year over the period 2007-2011. Assuming that 50% of this equity is accessible to investors (i.e., the portion of capital not derived from retained earnings, see Graph 1), it appears that approximately €5 billion of SME equity is accessible to external financing, including venture capital and development capital.

Equity capital has continued to strengthen in recent years, but at a slower pace than in previous years (+2.6% for all companies in 2013, after +2.8% and +4% in 2012 and 2011). Annual growth appears to be more dynamic for SMEs (+5.6% after -0.6%). It should be noted, however, that reserves and retained earnings play a more important role in strengthening equity than the results generated. This practice, already observed before the crisis, was confirmed afterwards, allowing for average equity resilience. Looking ahead, this trend could continue if reserves and retained earnings were to compete with potential dividend payments.

Figure 1: Change in SME equity and its components (2006-2013), in %

2) Venture capital and development capital for growth-oriented SMEs appear to be sufficiently provisioned in France

A normative approach to intermediary financing « needs » consists of analyzing the penetration rates of private equity in different national markets (measured as the amounts invested in a given year relative to GDP). While this approach does not strictly speaking allow us to estimate the financing needs of SMEs, it does enable us to assess the scope for growth of private equity in France compared with more mature private equity markets (Sweden, the United Kingdom, the United States, and Israel).

If we only take into account the upstream stages of private equity (i.e., excluding transfer transactions, particularly LBOs) intended to finance the development and growth of SMEs, the differences in penetration rates in France compared to other countries generally considered more mature in terms of private equity development appear to be low.

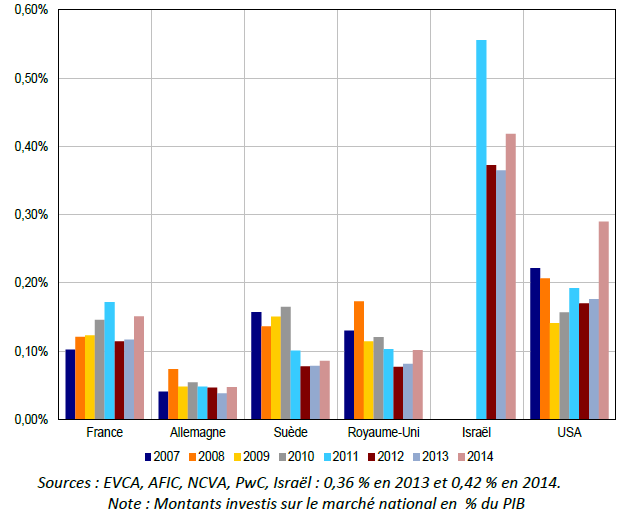

Until 2009, the share of French innovation capital and development capital (0.12% of GDP in 2009, see graph 2) was similar to that observed in the United Kingdom (0.11% of GDP in 2009), but lower than that observed in Sweden (0.15% of GDP in 2009) and the United States (0.19% of GDP in 2010). However, the relative resilience of investment observed in France contrasts with that observed in other countries[7]. From 2013 onwards, the average penetration rate of venture capital and development capital observed in France (0.13%) could even exceed that observed in Sweden (0.08%) and the United Kingdom (0.09%).

The equity needs of growth companies seem to have been relatively well covered by venture capital and development in recent years, thanks in particular to the public measures put in place, especially for small investments (the average investment was around €2 million in 2014).

Figure 2: Venture capital and development penetration rate[9]

Sources: EVCA, AFIC, NCVA, PwC, Israel: 0.36% in 2013 and 0.42% in 2014.

Note: Amounts invested in the domestic market as a percentage of GDP

3) However, large transactions are relatively few in France

The French private equity market as a whole is, relative to the size of the French economy, less developed than the more mature markets mentioned above. However, it is more developed than in Germany. In 2014, private equity financing for French companies represented approximately 0.41% of GDP, compared with 0.25% in Germany, 0.4% and 1.3% in the United Kingdom and the United States, respectively, and 1.6% in Israel. Furthermore, the private equity penetration rate in Sweden has fallen in recent years to an average of 0.3% of GDP since 2013, compared with 0.8% at the end of 2011. In terms of value, the average gap between the French penetration rate and the average for these markets was estimated at around €10 billion in 2014.

The venture capital and development segments appear to be relatively well developed in France. However,in the downstream segments and in large-scale transactions, France lags significantly behind these markets (for comparison, the average investment in the venture capital and development segments in the United States in 2014 was around €5.5 million per year, according to the NVCA).

The reasons put forward to explain this shortfall can be found on both the demand and supply sides for this type of financing:

· On the demand side, the number of « target » companies for « large » innovation capital (funding rounds of around €50-100 million) is low. Some managers of growth SMEs would prefer to be bought out and backed by a large group rather than grow independently. Others, on the contrary, would be reluctant to accept private equity backing, which could lead to a risk of the historical managers losing control of the company. This would ultimately contribute to the low number of mid-sized companies in France, some of which are also potential « targets » at the top end of the capital transfer segment (capital transactions of €100 million to €1 billion).

On the supply side for this type of financing, the relatively limited overall investment capacity of domestic funds would limit their participation in these large-scale transactions.

4) Quantitative and qualitative challenges

Ultimately, the challenges facing private equity in France can be approached in two different ways:

· Quantitative issues: The French private equity market, like the national productive fabric, which is mainly composed of micro-enterprises and SMEs, is a market mainly composed of small tickets (size of funds received by financed companies). In 2014, 56% of financed companies received less than €1 million (52% on average over the period 2009-2014) and 80% received less than €3 million. Investments of more than €15 million accounted for only 5% of companies in 2014, but 67% of the amounts injected by AFIC members. It therefore seems important to encourage the emergence of larger funds[12].

· Qualitative issues: In the most upstream segments, momentum is fueled by the presence of public players, while in the most downstream phases, the presence of investors, beyond the mere contribution of funds, is an essential aspect of the added value provided by the quality of support (participation in strategic development choices decided by companies).

Conclusion

While the most upstream segments of private equity appear to be well covered in France, supporting a significant number of companies (Europe’sleading market for venture capital), the financing of large-scale growth operations remains below the levels observed in more mature markets.

For example, in international comparison, the penetration rate of private equity remains far below the rates observed in the United States or Israel. It is therefore in the downstream segments, aimed at supporting the scaling up of companies, that France lags significantly behind these markets. In this regard, beyond maintaining sufficient investment capacity, the main challenges for the sector today appear to be more qualitative (quality of teams, size of funds, cross-functional operation of the business, etc.).

[1] FCPI and FIP schemes are an important channel for equity investment in SMEs, particularly innovative ones, by providing an incentive for individuals to subscribe to these dedicated funds. After declining steadily since 2008 (cumulative decline of 44%), FCPI and FIP fundraising increased in 2013 (€683 million after €628 million, +9%).

[2]There are around 5,000 mid-sized companies in France, compared with nearly 9,000 in Germany and 6,000 in Italy (source: Crédit Agricole).

[3] « Financing businesses and the French economy: towards a return to sustainable growth, » report by the FINECO working group of Paris EUROPLACE, December 2012. The method used is based on an assumption of private equity growth of 5% per year (corresponding to the average rate observed between 2005 and 2008) from 2010 (reference year) to 2020. This implies an increase in the penetration rate of private equity in France, reaching the current level of more mature countries by 2020.

[4] « SMEs in France in 2011: despite positive business activity, profitability is stagnating and financial structures remain heterogeneous, » Banque de France bulletin, No. 189, 3rd quarter 2012.

[5] Equity capital corresponds to funds from shareholders, reserves, and profits.

[6]Source: Report by the Business Observatory on the economic and financial situation of SMEs (January 2014).

[7]Eudeline et al. Will business investment pick up again in France in 2014? (2014)

[8]i) Call for projects « incubation and seed capital for technology companies » launched in 1998,

ii) The creation of the National Seed Fund, part of the Investments for the Future program, aims to continue this initiative.

iii) The establishment, in 2013, of the Public Investment Bank (Bpifrance), which quickly played a structuring role in the upstream segments of private equity, with growing market shares. As Bpifrance’s preferred mode of intervention (two-thirds of assets under management), fund of funds activity has, over the past 15 years, helped to irrigate and structure the French private equity market, particularly venture capital.

[9] These amounts should be interpreted with caution due to significant methodological differences in the calculation of aggregates. The AFIC definition of venture capital is similar to the EVCA definition of venture capital, which includes seed, start-up, early stage, and later stage; the AFIC definition of development capital is similar to the EVCA definition of growth capital. The US segmentation is slightly different: venture capital covers the seed, early stage, expansion, and later stage segments, where « expansion » does not quite correspond to AFIC’s « development. »

NVCA definition of « expansion stage »: « the stage of a company characterized by a complete management team and a substantial increase in revenues »; AFIC definition of « development capital »: « the company has reached its break-even point and is generating profits. Funds will be used to increase its production capacity and sales force, develop new products, finance acquisitions and/or increase its working capital. Financing relays have been included in this stage. »

[10]Based on a target private equity penetration rate of 1% of GDP, representing an investment of close to €20 billion.

[11] Which represents, outside of crisis periods, 60% to 80% of the volume of private equity in France. In 2013, only two innovation capital transactions of more than €15 million took place out of 469 transactions, and five development capital transactions of more than €30 million out of 802 transactions.

[12] Boosting digital startup financing in Europe.