In 2017, several factors could explain a potential slowdown in economic activity in emerging countries: capital outflows in response to rising interest rates in the United States (three increases announced by the Fed), low commodity prices, downward pressure on exchange rates, uncertainty about the rise of protectionism, and a contraction in foreign exchange reserves drawn from export revenues, etc. Everything suggests that the emerging countries that will appear most vulnerable will be those with high levels of short-term external debt.

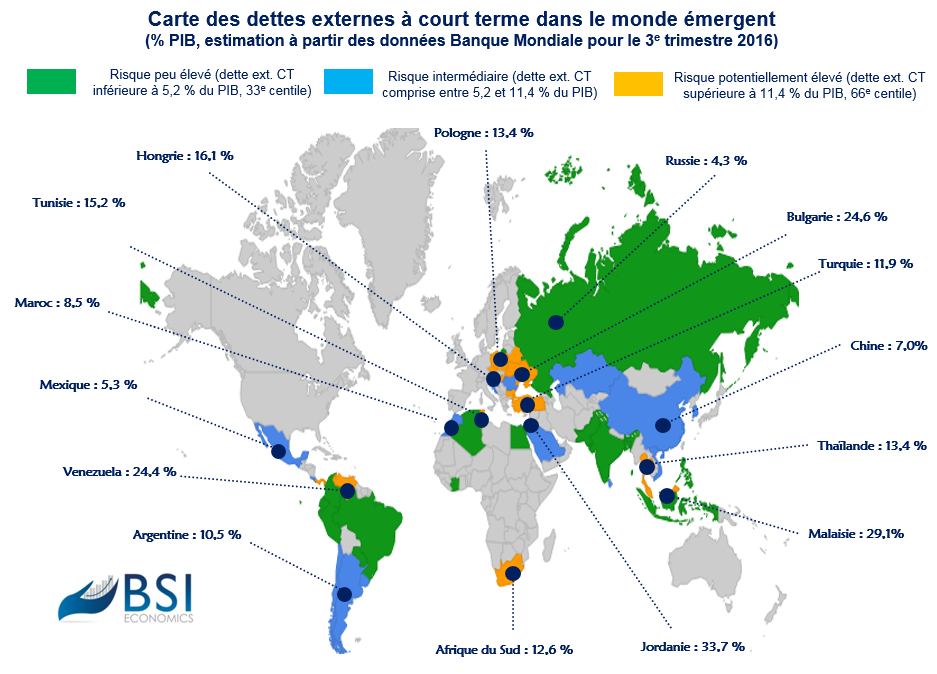

A country’s external debt corresponds to the stock of debt owed by its residents (general government, financial and non-financial institutions, households) to non-residents. Short-term external debt refers to all debt securities held by residents with non-residents that have a maturity of less than one year, i.e., part of the external debt that will have to be repaid within the next 12 months at the latest. Countries with high short-term external debt will be forced to repay a portion of this debt in the coming months, even as economic and financial conditions may deteriorate. They would then face several risks: refinancing risk (the risk of refinancing debt at higher and less favorable rates than in the past), currency risk (for countries with foreign currency debt, which will find it difficult to repay their creditors in foreign currency if their currency depreciates against those currencies), and interest rate risk (when debt is issued at variable rates, although this risk is similar to refinancing risk for short-term debt).

Based on data from the third quarter of 2016, several countries will be affected by these risks in the coming months. This is the case for Venezuela, with short-term external debt of 24.4% (where the risk of default is considered significant in 2017), Turkey (11.9%), South Africa (12.6%), Malaysia (29.1%) and Tunisia (15.2%). Other countries appear less risky at this stage in terms of their short-term external debt as a percentage of GDP, such as Argentina and Egypt, but the sharp depreciation of their currencies in recent months, combined with high inflation and a lack of foreign exchange reserves, would make it difficult for these countries to repay their creditors.

V.L