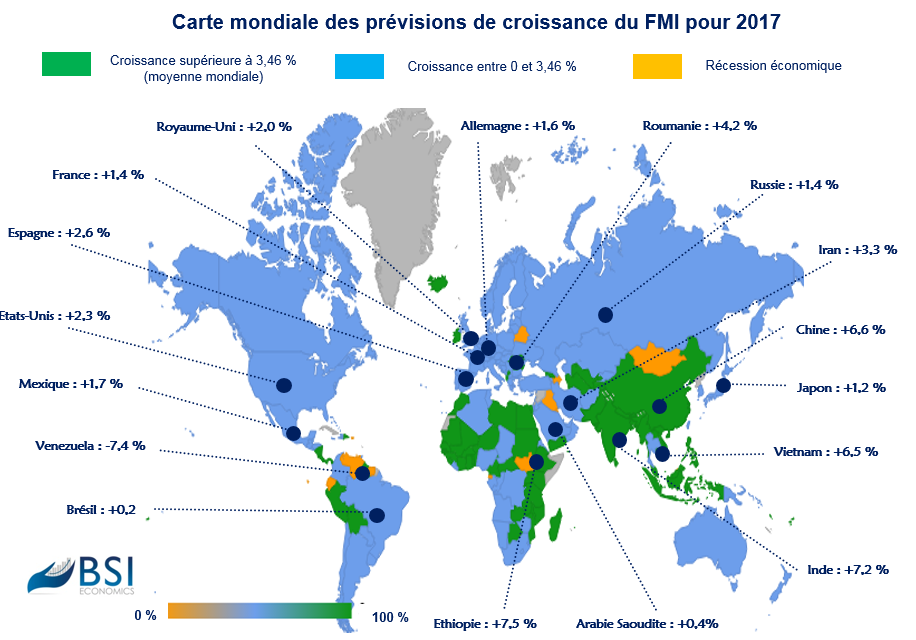

The International Monetary Fund (IMF) released its latest annual GDP growth forecasts in its April WEO (see map above). Global growth in 2017 is expected to increase compared to 2016, rising from 3.11% to 3.46%. Although growth will be stronger on average in emerging countries (4.49%) than in developed countries (2.01%), year-on-year growth was more than twice as high in the latter. Twelve countries are expected to be in economic recession in 2017, including Venezuela, Ecuador, Belarus, and Mongolia. After a difficult 2016, countries that were in recession, such as Brazil and Russia, will return to growth in 2017. Apart from Asia and, to a lesser extent, Africa, few countries in the rest of the world are expected to grow above the global average in 2017.

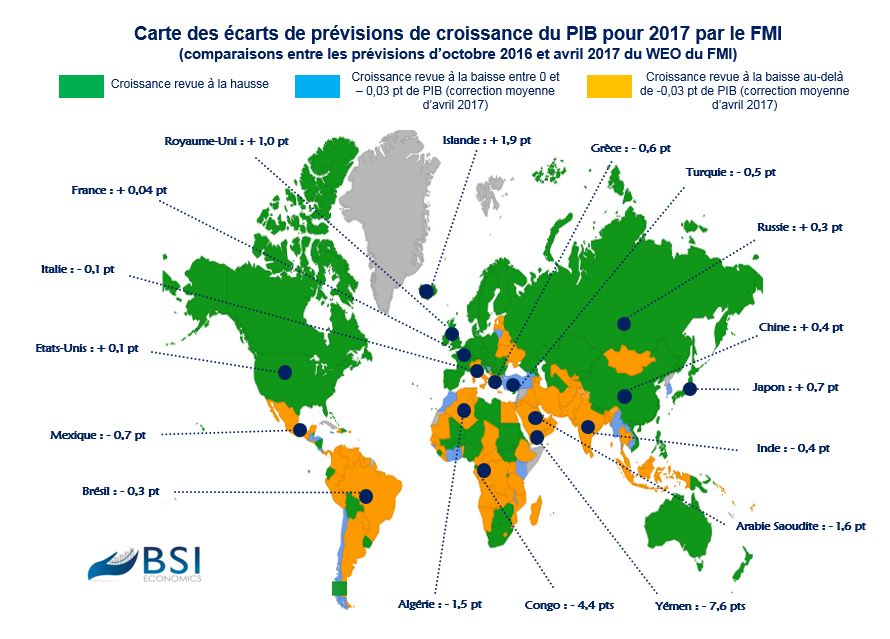

Between the IMF’s previous growth forecasts for 2017 in October 2016 and those in April 2017, it is interesting to note that an average downward adjustment of -0.03 percentage points of GDP has been made (see map above). A year ago at the same time, this adjustment for 2016 was more pronounced (-0.7 points on average). The IMF is more optimistic than it was six months ago in developed countries, particularly in the United Kingdom (adjustment of +1 point of GDP), where the conditions for a hard Brexit do not seem to be in place. In the eurozone, the combination of falling unemployment, rising private consumption and the European Central Bank’s (ECB) continued expansionary monetary policy gives hope for higher growth in 2017, even if many uncertainties remain (the banking situation in Italy, public finances in Greece, political risk in France, etc.). In emerging countries, the sluggish rise in oil prices (and its impact on fiscal policy, current account deficit financing, and exchange rate fluctuations) explains the downward revisions to growth in exporting countries (Saudi Arabia, Venezuela, UAE, Kuwait, Gabon, Angola).

Further adjustments are expected in October, particularly to assess the impact of the economic situation in the United States ( Fed funds rate hike, no fiscal stimulus in 2017, rise or fall of protectionism) and China (slowdown or not in Chinese growth and demand) on the rest of the world.

V.L.