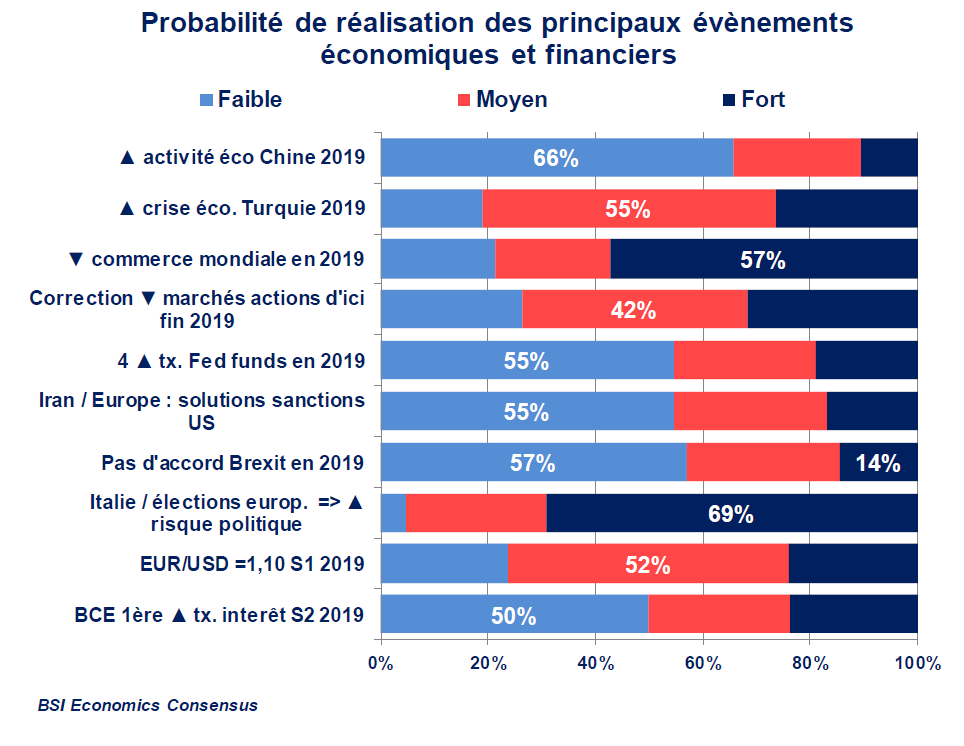

At the time of our survey, an increase in US tariffs on Chinese products was still expected on January 1, 2019, but this has since been postponed to March 2019. Based on the responses to this Consensus, three outcomes stand out: (1) global trade is expected to contract in 2019 (high probability for 57% of respondents), with significant export volumes already having been achieved in anticipation of this; (2) this slowdown in global trade would also be due to the slowdown in Chinese economic growth (likely for 66% of respondents) and (3) the decline in global trade would imply a moderate risk for equity markets: 42% anticipate a medium probability of a decline in global equities, while 26% anticipate no effect.

However, the expectation of a more cautious Fed and resilient equity markets despite the slowdown in Chinese growth is contradictory. In 2016, financial markets were cautious about the number of rate hikes by the Fed, encouraging a shift of flows to emerging markets, particularly Chinese markets. In this sense, if a pessimistic scenario for Chinese growth and a trade war were added to the 2016 scenario, then a stabilization of equity markets or even an increase would seem difficult to achieve.

The slowdown in global trade is likely to weigh on activity in the eurozone. The majority consensus is therefore that the European Central Bank will not raise interest rates before 2020. At the same time, while there is strong conviction about institutional risks with the conclusion of a Brexit agreement (57% of economists) and increased political risk in Italy ahead of the European elections (69%), there is no consensus on the trajectory of the euro against the US dollar. Only 24% of economists believe it will fall to 1.10 (currently 1.14 at the beginning of December, 1.18 on average for 2018). In the event of a contraction in global trade and continued US economic activity, economic and cyclical factors (growth and inflation differentials) would support the depreciation of the euro.

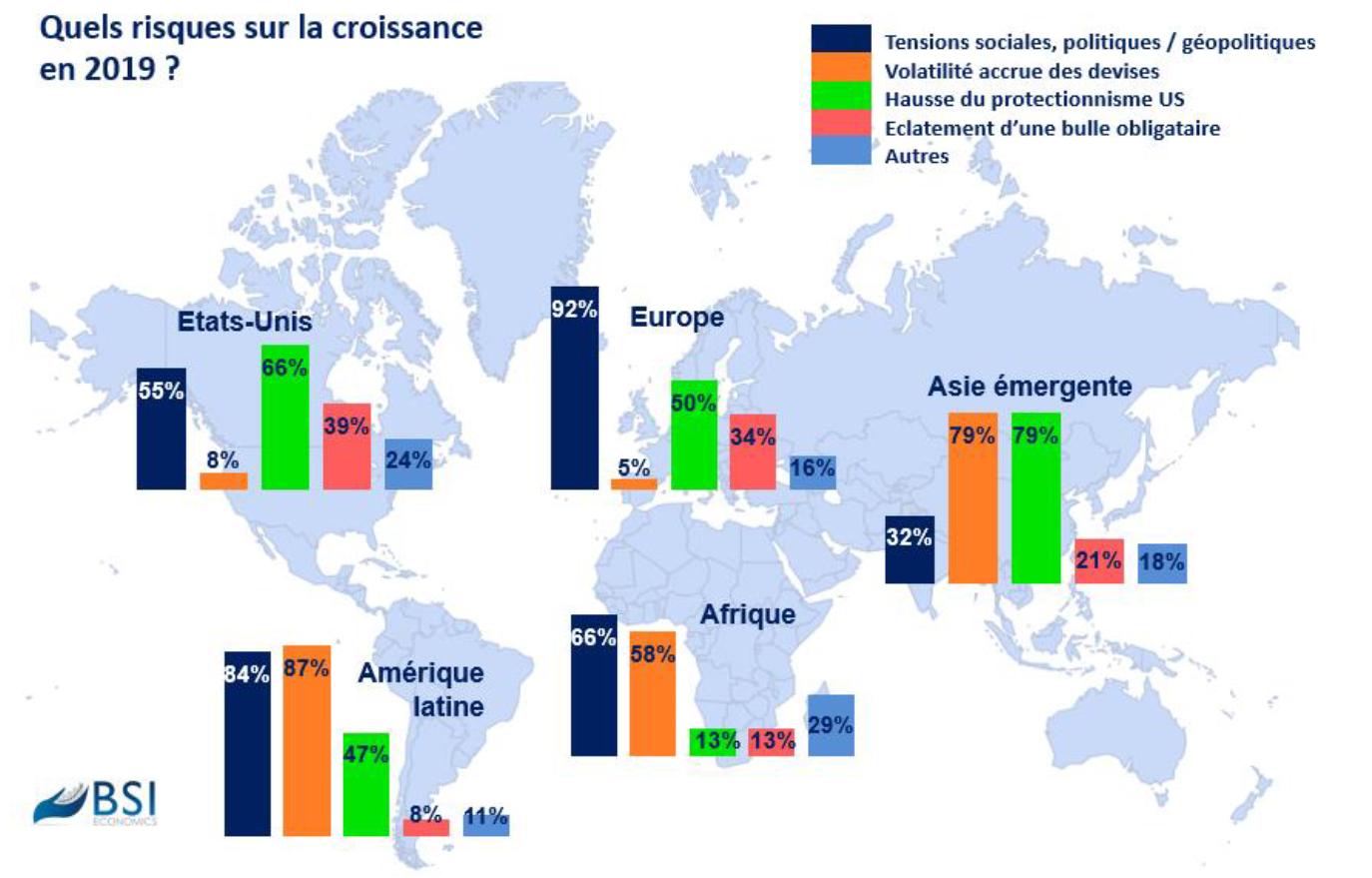

Social, political, and geopolitical tensions are identified as a significant risk to growth in developed countries in 2019, with a large majority (92%) agreeing this is the case for Europe. The situation in the United Kingdom, which will leave the European Union at the end of March 2019, continues to raise questions about both the details of Brexit and its economic impact. The European Union and Italy are still unable to agree on a budget, a situation that does not bode well with the European elections just a few months away in May 2019. Similarly, uncertainty remains in Germany, and recent social unrest in France reflects a delicate political and economic context. In the United States, it is more geopolitical factors that lead 55% of respondents to believe that this type of risk will weigh on growth in 2019. The highly unpredictable nature of US diplomacy under President Trump is causing considerable tension, with significant repercussions for global trade in particular. In Latin America, this risk is also significant (84% of respondents), fueled by several factors: the management of Venezuelan refugees, the political crisis in Nicaragua, the arrival of President AMLO in Mexico, which is worrying the financial markets, and the general elections in Argentina in October, at a time when the country is likely to be in economic recession. In Africa, this risk will remain high according to 66% of the panel, with important electoral and political issues at stake in South Africa, Nigeria, Algeria, and Tunisia.