Abstract :

- Brazil is suffering from sluggish growth and a worrying deterioration in its public finances, posing risks to the sustainability of its public debt;

- The future president will have to quickly tackle pension reform, as the pension system has contributed significantly to the deterioration of the primary budget balance.

- Brazil remains one of the most unequal countries in the world. Improving the effectiveness of redistribution policies will be crucial for continued social progress.

- Greater openness to international trade, combined with protection for workers and the most vulnerable, could increase the country’s productivity and ensure inclusive growth.

After plunging into recession in 2015, Brazil is still searching for prosperity. With a presidential election that will decide the country’s future just days away, this article looks at the major economic challenges facing the next president.

With just a few days to go before a decisive vote for the country’s future, Brazil is mired in uncertainty. Former President Lula (2003-2011), the Labor Party candidate and clear favorite in the election, was declared ineligible this summer following his conviction for corruption. Since then, no candidate has really managed to emerge, leaving the race wide open. According to the latest polls, far-right candidate J. Bolsonaro is expected to come out on top in the first round.

In a rather unfavorable international context, the next president will have to tackle challenges that are crucial for the country’s future: The decline in commodity prices and corruption scandals involving both the state-controlled oil company Petrobras and Brazilian construction giants have shaken the country, causing the decline of Latin America’s largest economy, which experienced its worst recession in history in 2015 and 2016. Brazil is currently suffering from a lack of growth and a rapid deterioration in its public finances, which has led to a downgrade of its sovereign rating.

1. A country hit by economic stagnation

1.a) An economy that is struggling to rebound

After experiencing its worst recession in 2015-2016 (with two years of sharp recession at nearly -3.5%), Brazil is tentatively returning to growth, with GDP growth of 1% in 2017, driven by private consumption and investment. However, forecasts for 2018 are constantly being revised downward, and growth is not expected to exceed 1.5%. Brazil is indeed affected by the current international context, with investors showing less appetite for emerging countries following the rise in US interest rates and also due to the tense context in which the presidential election is taking place. Potential growth remains relatively weak and is undermined by low investment rates, a deteriorating business climate, and a lack of productivity. According to the World Bank, the average worker in Brazil is only 17% more productive than 20 years ago (compared with 34% in developed countries), while total factor productivity contributed negatively to growth between 2009 and 2015, by -1 percentage point.

In addition, the social consequences of the recent economic contraction remain worrying. Unemployment rose from 6.8% in 2014 to 12.8% in 2017, while 25% of the population lives below the poverty line (USD 5.5/day according to the Brazilian Institute of Geography and Statistics). Job creation tends to be concentrated in the informal sector (even though informality had been reduced from 60% to 40% of total employment between 2004 and 2014), which undermines efforts to reduce income inequality and also weakens the tax base and productivity growth, a major problem for the country. The growth of informal employment disproportionately affects the most vulnerable groups of the population, particularly women, young people, and low-skilled workers in the northern and northeastern regions.

After a year of historically low inflation in 2017, consumer price inflation is expected to accelerate slightly in 2018 (to 3.5%), driven by the depreciation of the real, which is stimulating imported inflation. Since the beginning of the year, the Brazilian currency has depreciated by 20% against the USD. This return of inflation, despite a more modest than expected economic recovery, can also be explained by the unprecedented monetary easing in Brazil since October 2016, which has boosted credit and therefore the money supply. The Brazilian Central Bank has lowered its key interest rate by 775 basis points since October 2016, reaching an all-time low (currently 6.5%).

1.b) Rapid deterioration in public finances

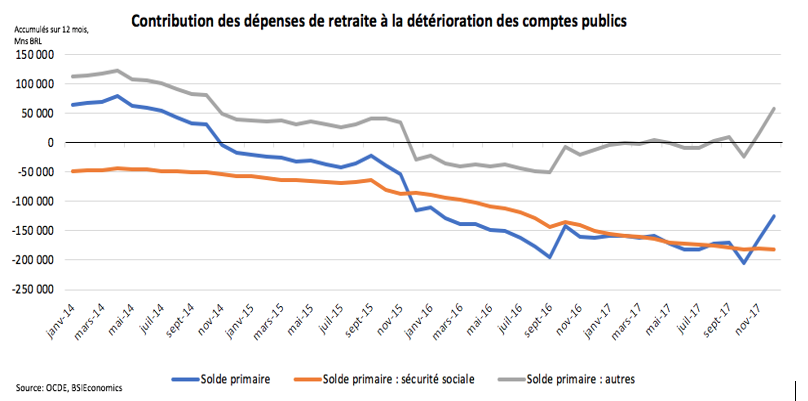

The increase in public spending, combined with the decline in revenues linked to the recession, has severely deteriorated the country’s public finances. After falling to -10.3% of GDP in 2015, the public deficit was reduced to -7.8% of GDP in 2017. The deterioration in public finances reflects an unsustainable trajectory of primary expenditure, which has grown nearly three times faster than GDP over the past decade. Expenditure over which the public authorities have greater control, such as public investment and cash transfers to the most disadvantaged, accounts for only 20% of the central government’s primary expenditure, leaving little room for flexibility.

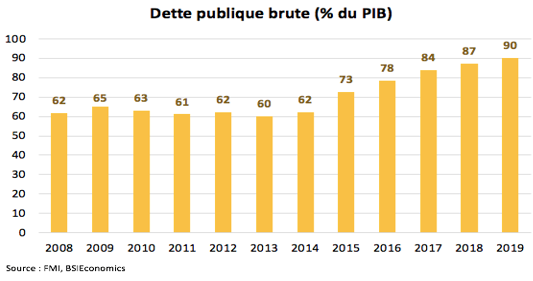

Given the size of the deficit, public debt is on an upward trajectory and is expected to reach 87% of GDP in 2018 (an increase of 25 percentage points in just four years), raising doubts about its medium-term sustainability. If the upward trend in debt continues, the recent rebound in the Brazilian economy could be threatened. In 2016, 16% of the country’s budget was devoted to debt interest payments (the second largest item after social benefits, which are mainly retirement pensions). Thus, the size of the debt burden necessarily reduces the authorities’ room for maneuver.

This deterioration in public finances is weighing on investor confidence in the sustainability of public debt. Combined with uncertainties surrounding the presidential election and the international context of emerging currencies falling behind the dollar, this deterioration has led to a sharp depreciation of the exchange rate. The share of public debt denominated in foreign currencies remains low, however, which mitigates the impact of exchange rate fluctuations. Nevertheless, this inevitably leads to higher sovereign interest rates and tighter financial conditions. In early 2018, rating agencies Fitch and Standard & Poor’s downgraded Brazil’s sovereign rating, citing the large and persistent budget deficit, high and rising public debt, and failure to implement reforms that would improve the structural performance of public finances.

2. What challenges await the next president?

2.a) Reforming an unsustainable pension system

Pension reform is a thorny issue in Brazil, which future ex-President Michel Temer has abandoned, having failed to convince Brazilians of its necessity. This backtracking is forcing Brazil to cut public investment, even though the country is sorely lacking in infrastructure.

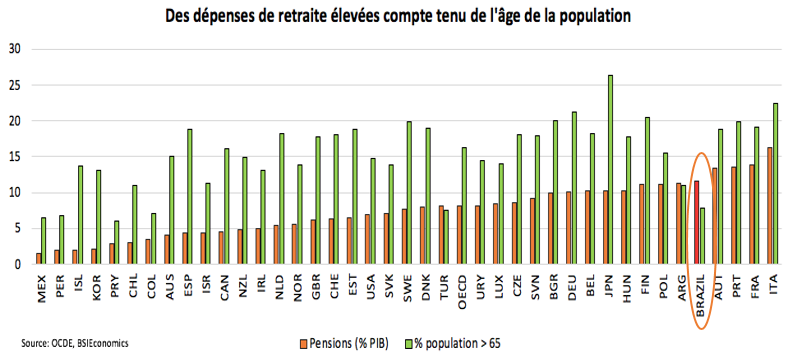

To rebalance public accounts and better control spending, reforming the pension system seems essential. Indeed, the current system could quickly become financially unsustainable. According to the OECD, pension expenditure rose from 4.6% of GDP in 1995 to 12% of GDP in 2018, which is high given Brazil’s young population. In terms of pension costs, Brazil ranks fifth among the rich countries of the OECD (an organization of which it is not currently a member), even though the proportion of people over 65 is one of the lowest. In the longer term, the aging of the population will lead to increasingly high pension expenditures if the current parameters of the system remain unchanged. Without any reform, they could reach 17% of GDP in 2060.

In addition, pension expenditure has contributed significantly to the deterioration of the primary budget balance. All pension benefits are subject to the minimum wage, resulting in high replacement rates, particularly for low-wage earners.

Brazil currently has one of the most unfair pension systems in the world, disproportionately favoring civil servants, who can retire at age 55 while receiving almost their full salary. Reforming this system would be an opportunity to make growth more inclusive through better targeting of benefits. Harmonizing Brazil’s pension rules with those in OECD countries would mean a minimum pension below the minimum wage. Indexing pension benefits to the consumer price index for low-income households would preserve the purchasing power of retirees while improving the sustainability of the pension system. The sustainability of the system would also be enhanced by a formal minimum retirement age, as the effective retirement age of 56 for men and 53 for women is well below the OECD average (65 for men and 64 for women).

2.b) Reducing persistent inequalities

Strong growth and remarkable social progress over the past two decades have made Brazil one of the world’s leading economies (7th in terms of GDP weight in 2017), despite the economic difficulties that followed. A dynamic labor market, combined with improved access to education, has enabled millions of Brazilians to find better jobs and improve their living conditions. As a result, 25 million Brazilians have been lifted out of poverty since 2003.

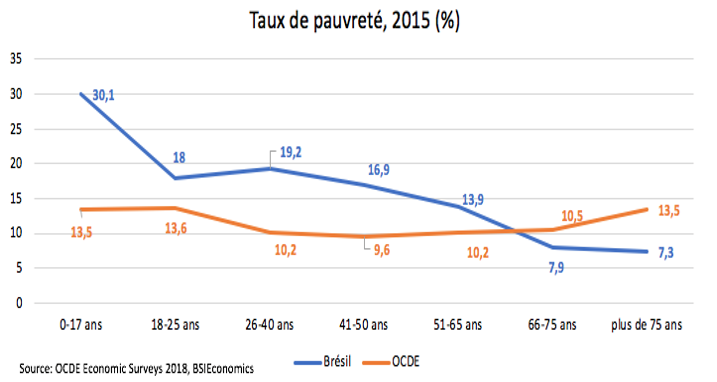

Nevertheless, Brazil remains one of the most unequal countries in the world. Half of the population receives 10% of total household income, while the other half receives 90%. Serious inequalities continue to disadvantage women, racial minorities, and young people. Men are paid 50% more than women, a gap 10 points higher than the OECD average. Poverty is higher among children, and youth unemployment is more than twice the global average. Limiting future increases in social benefits that mainly affect the middle class could help increase social transfers with a strong impact on reducing inequality and a strong focus on children and young people.

Improving the efficiency of public spending, and in particular redistribution policies, will therefore be crucial for continued social progress. Well-targeted transfers, combined with further improvements in education and health, are key to more inclusive growth.

Finally, the widespread corruption practices revealed in recent years highlight the importance of the challenges that exist in economic governance. These practices have hampered the effective redistribution of resources and made the political decision-making process less transparent. Thus, better combating corruption would help reduce income and opportunity inequalities and boost productivity.

2.c) Opening up more to international trade

With exports and imports accounting for less than a quarter of GDP, Brazil is not very integrated into international trade and is less open than OECD countries as a whole. This reflects several decades of protectionist policies and a successful strategy of industrialization through import substitution. Greater openness to international trade could increase the country’s productivity and create new jobs across the economy. Consumers would benefit from more competitive prices, with particularly significant effects for low-income households.

Greater integration into the global economy would be an effective way to increase competition and help the most productive companies and industries succeed, even if a small number of sectors would see their output decline. Well-designed policies that protect workers through better training and greater protection for the most vulnerable would ensure inclusive growth.

Conclusion

Regardless of the election outcome, the new president will need to shake the economy out of its torpor and generate a confidence shock. To do so, he or she will need to tackle the chronic problem of the budget deficit and public debt, while also addressing pension reform. Reducing inequality and the scourge of corruption will also be essential.

Bibliography:

- ECLAC: « Economic Survey of Latin America and the Caribbean, » 2018

- OECD Economic Surveys, Brazil, Overview, 2018

- IMF, Article IV, August 2018

- OECD Policy Memo, Pension Reform in Brazil, April 2017

- Forbes: “Who Can Save Brazil’s Lousy Economy?”, Kenneth Rapoza, August 2018a

- Financial Times: “Brazil’s economy: from zombie to walking dead,” Joe Leahy, March 5, 2018

- French Embassy in Brazil, Regional Economic Service: “Inflation remains moderate for 2018, despite upward pressures linked to the depreciation of the real,” August 2018.

- OECD: “A broken social elevator? How to promote social mobility. How does Brazil compare?”, 2018

- OECD: “How’s life in Brazil?” November 2017

- ECLAC: « Economic growth and income concentration: their effects on poverty in Brazil, » Jair Andrade Araujo, Emerson Marinho, and Guaracyane Lima Campêlo, December 2017

- World Bank: « Productivity: a key issue in combating poverty in Brazil, » Mariana Ceratti, August 2016

- World Bank: “Brazil’s Productivity Dynamics,” Rong Qian, Jorge Thompson Araújo, and Antonio Nucifora, February 2018