Summary:

- Bitcoin is a digital asset based on blockchain technology, which it pioneered. Its value and popularity have grown rapidly, driven both by interest in this innovation and its ecosystem, and by speculation surrounding bitcoin and other crypto-assets[1];

- In the wake of Bitcoin, alternatives and innovations using this technology have emerged, offering better performance (energy, speed) and new features compared to Bitcoin.

- Among these are decentralized application platforms, the best known of which is Ethereum, which enable the creation of smart contracts.

- Blockchain technology is now the subject of numerous projects with extremely broad potential applications.

In the wake of Bitcoin, the crypto-asset market has experienced extremely rapid growth in recent years, fueled by both technological enthusiasm and strong speculative appetite. On the technological front, this has been driven by the democratization of the blockchain concept, while on the financial front, it has been driven by a rapid increase in valuation levels.

For a long time, the crypto-asset market remained the preserve of a community of insiders and IT innovation enthusiasts, before experiencing a meteoric rise and exceeding $800 billion in valuation at the end of 2017. Many observers see this phenomenon as a speculative bubble that will eventually burst (see a previous article by BSI Economics here). Others, however, see it as the emergence of assets, and more certainly of a technology, that are set to last and take up an increasingly important place in the economy.

1. What is bitcoin?

The firstborn of a very (too?) large family, Bitcoin has long dominated the crypto-asset market unchallenged. Bitcoin’s « dominance, » i.e., its weight in market valuation, fluctuated around 90% for a long time before declining significantly (it is now below 50%).

At the same time as a very rich ecosystem was developing around Bitcoin, alternatives emerged that far exceeded its technical performance and functionality. Now, its status as the first mover and its reputation seem to be Bitcoin’s main assets in remaining the benchmark asset around which the entire market revolves. However, this position is increasingly being challenged.

Blockchain technology was born on January 3, 2009, with the validation of the first block (called « block genesis ») of the Bitcoin chain, whose network was then in its infancy. Since then, the ledger has been enriched with a new block at an average rate of 10 minutes per block, reaching a total of 500,000 blocks by the end of 2017.

Created shortly after the subprime crisis, Bitcoin was intended as a response to the failure of the global monetary and financial system, and developed around an anti-authoritarian community, the cypherpunks, before becoming popular. It is based on disintermediation (transactions are peer-to-peer), a public transaction ledger (which makes them traceable, meaning that Bitcoin is not fungible), and a decentralized governance model based on consensus among the actors responsible for validating blocks (the « miners »).

2. Fund miners

The meteoric rise in the price of Bitcoin has given rise to new vocations. Long reserved for insiders in its community, the validation of blocks in the Bitcoin chain, which is remunerated in Bitcoins, has become more sophisticated, professionalized… and concentrated. It is interesting to understand why a project initiated on the basis of decentralization and monetary self-management of a community has led to a concentration of means of production and decision-making, a scenario that has been tried and tested many times since the emergence of capitalist economies.

The validation of a new block of bitcoin transactions is carried out by the « proof of work » provided by the activity known as « mining. » Mining consists of using the computing power of computer hardware to discover the « hash »[2]that will validate a block being written. The discovery of the hash by one of the network’s participants is rewarded with newly created bitcoins. The number of bitcoins that rewards the « miner » who provided the hash is predetermined. Originally set at 50 bitcoins, it is halved every 200,000 blocks and is now 12.5 bitcoins. In 2140, when the last block rewarded by bitcoin issuance has been reached, mining will only be rewarded by the fees associated with network user transactions. This feature makes bitcoin, whose maximum supply is limited to 21 million and whose issuance rate is decreasing, a deflationary asset. The higher the computing power deployed by a miner (known as the « hashrate »), the more likely they are to be the first to discover the hash of a block and pocket the associated bitcoins.

However, the validation of blocks and the governance model of the Bitcoin network, based on proof of work, are showing their limitations. The meteoric rise in the price of Bitcoin has led to massive investments in extremely energy-intensive mining equipment. This frantic race for computing power has led to the creation of mining farms and mining cooperatives. The resulting concentration of hashrate is both a departure from the original Bitcoin project (which aimed only at institutional decentralization) and a potential threat to the strength of its blockchain.

Paradoxically, what could ensure Bitcoin’s invulnerability actually makes it potentially weak. Modifying the content of the blocks in the chain becomes more difficult and more expensive as the computing power deployed increases, but since this increase is accompanied by concentration, it theoretically makes the Bitcoin chain vulnerable to attack. This threat is known as a « 51% attack, » which is a situation where a group has enough computing power to validate a modified blockchain. Solutions (increasing the number of confirmations, Bobtail method) limit but do not eliminate the possibility of a modified version of the blockchain by a user (or group of users) with high computing power.

Alternatives have emerged. They are based, for example, on a consensus mode based on proof of work that is « resistant » to energy-intensive mining equipment and limits the escalation of energy costs associated with the increase in asset value and the concentration of computing power. More disruptive still, other assets operate without the use of proof of work in the block validation process, replacing it with, for example, proof of stake (consensus based on the mass owned by network users).

3. A common global « currency »?

Bitcoin is sometimes mentioned as a possible universal means of payment. As things stand, its technical performance makes it completely incapable of assuming such a role. Over time, bitcoin has acquired a role as a benchmark for parities and a store of value in the crypto-asset ecosystem, which makes it more comparable to gold than to a means of payment.

Bitcoin’s (current) technical limitations in this specific area point to a major challenge: scalability, i.e., the ability of a blockchain network to support a large number of transactions.

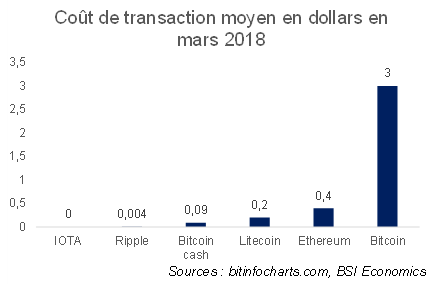

In the case of bitcoin, the size of a block is currently capped at one megabyte, which significantly limits the number of transactions that its network can support (currently around seven per second, a capacity that is hardly compatible with its role as a large-scale means of payment, whereas the Visa network can support tens of thousands). The Bitcoin network is therefore frequently saturated: on average, the size of a block has now reached 99.9% of its maximum size during the last months of 2017. Several avenues have been explored to remedy this:

- The adoption of the segwit process (which reduces the amount of information in a transaction, in this case by removing the signature) lightens the weight of a transaction and therefore increases the capacity of a block;

- Increasing the size of blocks: doubling the size was abandoned with great fanfare in November 2017 due to a lack of consensus;

- The « lightning network, » which consists of creating temporary peer-to-peer channels outside the blockchain.

Some of the players in the Bitcoin network consider that the original purpose of Bitcoin is to serve as a means of exchange, and a « hard fork »[3] took place on the Bitcoin chain in the summer of 2017, giving rise to a new asset, Bitcoin Cash, whose block size is no longer 1 megabyte but 8 megabytes, limiting congestion problems and rising transaction fees.

Litecoin also has better scalability than Bitcoin, not because of a larger block size, but because of a block validation frequency that is four times higher than that of Bitcoin, which increases the capacity of its network accordingly.

Protocols that differ more significantly from Bitcoin now offer more efficient performance (scalability, transaction time, energy cost) thanks to blockchain technology, relying on a simpler and less energy-intensive validation process (the most common being proof of stake), or even using a technology other than blockchain (IOTA, one of the highest market valuations, uses a directed acyclic graph, or DAG). In the international transfer segment, for example, the Ripple and Stellar protocols (which use proof of consensus), which are also among the leaders in terms of valuation, now offer extremely efficient solutions in terms of cost, speed, and scalability. This has enabled the Ripple Foundation to sign numerous partnerships with financial and banking institutions.

4. New features for blockchain technology: in the wake of Ethereum, the emergence of decentralized application platforms

Bitcoin’s main competitor as a benchmark asset is now ether, which has established itself as the second largest market capitalization.

The Ethereum project was initiated in 2013 by the young Vitalik Buterin, now a key figure, who published the project’s « white paper » at the age of 19 with the aim of raising the necessary funds to finance it. In July 2015, the first block of the Ethereum blockchain was mined.

Incidentally, this fundraising effort gave rise to a new form of financing called Initial Coin Offering (ICO), analogous to Initial Public Offerings (IPO). In exchange for funds, often contributed in bitcoins (or now in ethers), ICO participants receive tokens that give them a right of use.

Technically, Ethereum retains the principle of decentralization and (for now) proof-of-work validation. Proof-of-stake validation, which delegates governance to ether holders rather than miners, could replace it.

The Ethereum network offers better scalability and shorter block validation times, but its main contribution lies elsewhere. It offers the possibility of creating smart contracts that enable the creation of decentralized applications or « dapps. »

As the first to arrive and the most valuable, Bitcoin has established itself as a benchmark: a small portion of assets are directly denominated in fiat currencies (euros, dollars, Korean won, etc.), and the vast majority are in Bitcoin. The innovative strength of projects that have leveraged the possibilities of applications and uses of its network makes Ethereum the center of gravity of a thriving ecosystem and gives it great legitimacy. It is still too early to say whether these arguments will be enough to make it the successor to Bitcoin as a benchmark asset.

Like Bitcoin, Ether has also seen the emergence of competitors, but like its predecessor, it has the advantage of being the first to establish itself in its field of development, even if its technical performance is not the best. Among the (non-exhaustive) list of these new competitors are EOS (which offers unparalleled scalability and could prove to be the successor to Ethereum), Lisk (which offers new accessibility to a range of application development on a network operating with a main blockchain and other subsidiary chains), and Neo, a platform often referred to as « the Chinese Ethereum » thanks to its great capacity for innovation and which hosts a growing number of applications on its network.

5. What does the future hold for crypto-assets and blockchain?

Technological advances in « altcoins »[4] now make Bitcoin seem technically outdated. The foundations of its development around a community of users using their personal computers to form a decentralized network appear largely disconnected from the financial evolution of Bitcoin and the speculation surrounding it, as well as its technological capabilities, which have evolved much more slowly than its popularity.

The alternatives to Bitcoin that have emerged in recent years now appear to be more effective (in terms of transaction speed and cost, energy cost) in fulfilling certain functions of Bitcoin, offering new ones, and, even more so, pursuing the goal of a digital value whose governance process is decentralized, and not just institutionally.

However, its creation has enabled blockchain technology to emerge and make extremely rapid advances. Ultimately, blockchain technology could find its way into many economic sectors, a largely incomplete list of which is provided here:

- Value transfer: since Bitcoin, alternatives have emerged. These range from Bitcoin offshoots to digital currencies that are more disruptive in terms of block validation or based on other technologies, such as DAG, mentioned above.

- More broadly, beyond value transfer and payment methods, most traditional financial services are potentially affected by blockchain;

- Decentralized application and smart contract platforms, such as Ethereum or EOS, which offer the possibility of raising funds;

- The fight against counterfeiting and product traceability.

- Secure data exchanges, for example in the medical field or the Internet of Things, voting, etc.;

- Decentralized data storage, on which several projects are currently being built;

- The rapidly growing field of artificial intelligence also has much to gain from blockchain technology, which enables the creation of vast databases and highly developed smart contracts.

Conclusion: beyond bitcoin

Both a technological innovation and a « currency » of protest, Bitcoin has given rise to numerous alternatives, which either embrace or bury the dreams of its early supporters as a store of value and means of transfer.

The development of blockchain use in successive waves, first in this segment and then in platforms, is now giving rise to a wide variety of projects. Blockchain technology is proving to have a surprising wealth of applications in a large number of potential areas. These emerging projects in the crypto-asset and digital asset ecosystem could therefore affect many sectors, although it is still too early to say which projects are truly innovative and will lead to improvements on the existing situation and mass adoption.

[1] For convenience, we will use the umbrella term « crypto-assets » to refer to digital assets based on blockchain technology or resulting from ICOs. The widely used term « cryptocurrencies » corresponds to functions that only some projects aim to achieve, and is also subject to debate.

[2]A hash is a fixed-length string of letters and numbers that corresponds to the algorithmic transformation of the information contained in the block’s transaction log.

[3] A hard fork is a split in a blockchain that results in the creation of a new asset. In contrast, a soft fork is a modification of the rules of a protocol.

[4] Alternatives to Bitcoin