Usefulness of the article: To tackle the COVID-19 epidemic, national and European authorities have relaxed bank capital requirements. This countercyclical response aims to prevent the economic crisis from spreading to the financial system. This article reviews the challenges of banking capital regulation and some of the reforms introduced since the 2008 crisis: the strengthening of bank capital and the creation of countercyclical instruments.

Summary:

- The 2008 financial crisis revealed two weaknesses in banking regulation: banks were undercapitalized, and their procyclical behavior amplified the crisis.

- The banking system is now better capitalized, although the optimal level of capitalization remains a subject of theoretical and empirical debate.

- The introduction of the countercyclical buffer allows national regulators to adjust capital levels according to the cycle; its relaxation, together with that of other requirements, allows authorities to respond countercyclically to the COVID-19 crisis.

As impressive as they may be, current economic statistics mechanically reflect the effects of lockdown and the concomitant fall in production. A key factor in ensuring that the impact of this crisis does not go beyond the direct effects of lockdown will be to prevent it from degenerating into a financial crisis. Regulators have taken the lead. Among the most symbolic measures, national and European authorities have relaxed bank capital requirements.

But what do these measures mean? To better understand the issues at stake, this article reviews the logic behind bank capital regulation and the debate over the calibration and procyclicality of requirements that has been raging for the past ten years.

A global regulatory framework set by the Basel Accords

Bank capital corresponds to a bank’s equity, i.e., the accounting difference between what the bank holds (notably loans to businesses and households) and what it owes (notably deposits from households and businesses). Regulation of bank capital consists of limiting the debt ratio of banks. While such rules might seem strange in other sectors of activity, they are justified in the banking sector by the existence of public deposit guarantees: a guarantee on household loans to banks (their deposits) up to €100,000, which aims to prevent bank runs [Note 1]. This guarantee amounts to subsidizing bank deposit financing with public money: households no longer have to price in the risk of their bank defaulting and can be satisfied with very low rates on their savings since they are safe. This is referred to as moral hazard, in the sense that households behave differently than they would if they themselves bore the risk of their bank defaulting. It is therefore logical that the government should require a minimum amount of bank capital in order to limit recourse to this insurance. The principle is as follows: capital must enable banks to cope with unexpected losses, i.e., losses that are not priced into their commercial interest rates. Since the first Basel Accords in 1988, these capital requirements have been harmonized at the international level.

However, these requirements applied regardless of the level of credit risk. This introduced a risk of regulatory arbitrage: banks could seek to take on more risk without exposing themselves to higher requirements. However, these riskier loans are also more sensitive in times of crisis: unexpected losses on these assets can be greater. The Basel II agreements therefore introduced the concept of risk weighting, with the aim of expressing the requirement not simply in terms of the amount of credit granted, but in terms of the amount of credit weighted by its level of risk. Higher risk loans are thus assigned a higher weighting [Note 2].

The 2008 crisis revealed two limitations of this system. On the one hand, banks were not sufficiently capitalized to cope with the materialization of extreme risk. On the other hand, this system led to procyclical reactions by banks, which amplified the crisis. The Basel III agreements took both of these aspects into account.

Increased capital requirements

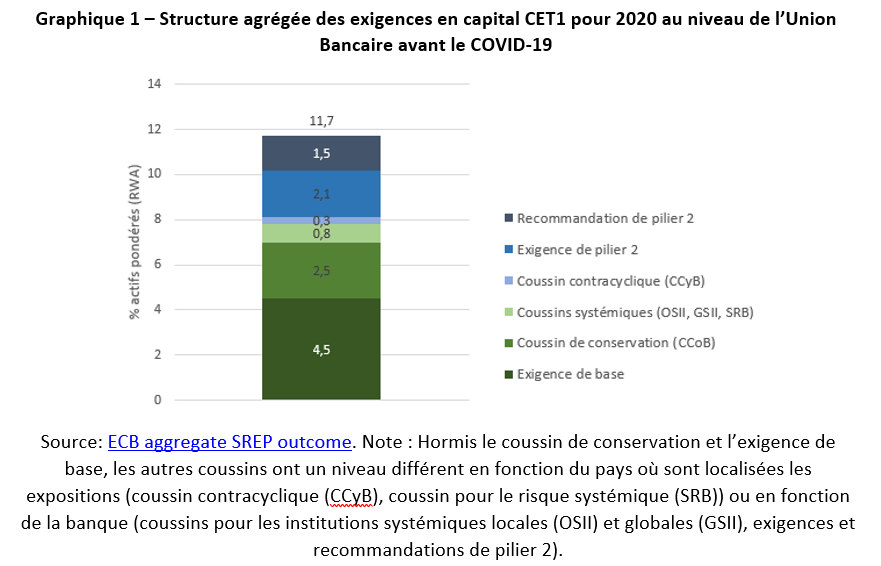

The first area of reform was to increase capital requirements. The minimum requirement for higher quality capital (Common Equity Tier 1, or CET1) is now 7% of risk-weighted assets (RWA), compared with 2% before the 2008 crisis [Note 3]. This across-the-board increase was supplemented by increases targeting certain risks, such as the introduction of specific buffers that are higher for banks that are systemic and implicitly protected by the state. The current total requirement is therefore 11.7% of RWA in the Banking Union, and the banking system effectively holds capital amounting to 14.6% of its weighted assets (Chart 1). In numerical terms, this represents €1.7 trillion in capital, covering €11.7 trillion in risk-weighted assets [1]. Despite the downward trend in capital ratios from a historical perspective [2], Basel III has therefore made it possible to strengthen them substantially in recent years [3]. However, the question of their optimal calibration is still under debate: what level of shock should they be able to absorb?

Source: ECB aggregate SREP outcome. Note: Apart from the conservation buffer and the basic requirement, the other buffers have different levels depending on the country where the exposures are located (countercyclical buffer (CCyB), systemic risk buffer (SRB)) or depending on the bank (buffers for local systemically important institutions (OSII) and global systemically important institutions (GSII), Pillar 2 requirements and recommendations).

In this debate, two camps are logically opposed. On the one hand, advocates of lower requirements will highlight the special nature of bank debt, which consists largely of deposits. By offering this savings product to households, banks fulfill an essential role in the economy: creating liquid and secure securities. Providing this service allows them to benefit from a liquidity premium, which explains why banks are able to finance themselves at low cost. In this context, limiting banks’ debt ratios would unduly increase the cost of capital used by banks to finance themselves [4]. In turn, an increase in their cost of capital would be reflected in the cost of credit granted to households and businesses. According to studies, this increase in the cost of credit would be 10 to 15 basis points per point of capital [5].

On the other side of the spectrum, those who advocate for stricter requirements argue that they would make the financial system safer at a lower cost [6]. The logic of the Modigliani-Miller theorem, which is fundamental in corporate finance, is that the cost of capital for a company does not depend on its financing structure, but solely on its investment opportunities [7]. Any increase in leverage would automatically increase the cost of financing a unit of equity, which would become riskier. The high level of debt observed in banks would then stem mainly from the deductibility of interest from corporate income tax (common to all sectors of activity) and deposit insurance (specific to the banking sector). These factors reduce the cost of debt relative to equity and encourage banks to increase their leverage to optimize their cost of capital. Finally, an increase in the cost of credit could remain beneficial from a societal perspective if it were offset by greater gains in terms of financial stability [8].

A complementary approach to determining the appropriate level of requirements is to test the resilience of banks by imagining economic and financial crisis scenarios: these are known as « stress tests. » They make it possible to determine whether the capital held is sufficient to cope with plausible crisis scenarios. In Europe, these exercises are carried out every two years by the European Banking Authority. The 2018 exercise estimated the aggregate losses of European banks at 4 points of capital [9]. In their scenario, half of the banks had to restrict their dividend distributions in order to maintain their capital above regulatory thresholds [Note 4].

The implementation of countercyclical mechanisms

A second failure of the system during the crisis was to cause procyclical behavior that amplified the crisis. In times of stress, bank capital deteriorates through two channels. On the one hand, the increase in borrower default rates directly leads to losses for banks and erodes their capital. On the other hand, the increase in default risk translates into increased requirements through risk weightings. In this context, a bank has a range of three tools at its disposal to adapt: increasing its capital, reducing its loan volume on the balance sheet (by reducing its lending activity or reselling its loans on the secondary market through securitization), or de-risking its portfolio (restricting credit to the riskiest borrowers). In a crisis situation, the first option can be very disadvantageous if stock prices have fallen too much. Banks will therefore give priority to using the other two levers. In doing so, access to credit becomes more difficult and can have a retroactive effect on the borrower’s probability of default, which deteriorates further.

To address this problem, the Basel III agreements introduced the countercyclical buffer. This requirement, set by national authorities at between 0 and 2.5% of RWA, must be increased during periods of growth and relaxed during periods of crisis [Note 5]. Countercyclical requirements proved their usefulness in Spain with the use of a dynamic provisioning system in the 2000s [10]. Banks were then required to set aside more provisions during calm periods and could reduce their provisions when a crisis hit. This did not prevent the banking crisis, but the banks that had to make the most use of this system were better able to maintain their credit flows.

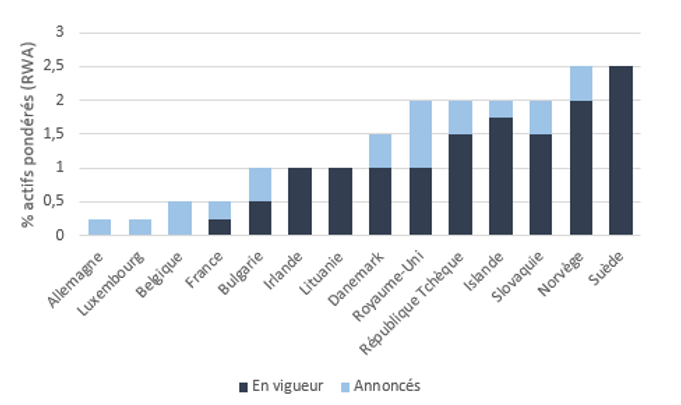

At the European level, many countries have introduced a countercyclical buffer since 2013, albeit to varying degrees. In France, the High Council for Financial Stability has increased this requirement twice—it was set to reach 0.5% in April [11]. Against a backdrop of low bank profitability and the gradual implementation of other requirements, regulators have remained cautious with this tool (Chart 2). For most countries, the current crisis is the first opportunity to relax this requirement [Note 6]. According to the ECB, the combined use of European countercyclical buffers and a few other requirements imposed by national authorities has reduced European bank capital requirements by €20 billion [12].

Chart 2 – Applicable countercyclical buffer rates announced by European Economic Area countries that had announced a non-zero buffer as of December 2019

Source: ESRB. Note: The regulations provide for a one-year period between the announcement of a countercyclical buffer and its application, to give banks time to adjust to the new requirements.

Regulators have also used other levers to give banks flexibility. Specifically, the single banking supervisor has authorized banks to operate under Pillar 2 guidance (a discretionary capital requirement specific to each bank and set by the supervisor) and to cover the Pillar 2 requirement with lower-quality capital (a measure initially planned for 2021, the application of which has thus been brought forward). These measures represent a €120 billion reduction in aggregate bank capital, according to the supervisor [13]. Other technical rules have been relaxed, including a reduction in capital requirements for market risk to offset market volatility and a relaxation of the treatment of non-performing loans [14].

To prevent the released capital from being distributed to shareholders, the supervisor has indicated that banks should not pay dividends until October. Beyond its symbolic dimension, this measure has a desirable countercyclical effect: it prevents banks close to the capital constraint from seeking to restrict credit instead of reducing their dividends. Finally, a major relief could come from the prudential treatment of government-guaranteed loans. These loans could benefit from a minimum weighting (loans guaranteed by the highest-rated sovereigns benefit from a 0% weighting), allowing banks to absorb these loans on their balance sheets without constraining their capital [Note 7].

Conclusion

Current events will therefore provide an opportunity to test the regulatory architecture that emerged from the 2008 crisis, and certain factors are reassuring. On the one hand, the banking sector’s capitalization levels are higher. Second, the authorities have swiftly deployed a range of measures to limit the potentially procyclical effects of capital requirements. In addition, fiscal and monetary support is helping to transfer risks from private balance sheets to public balance sheets, easing the strain on banks. Naturally, bank balance sheets will ultimately reflect the difficulties of their borrowers. Private and public sector debt levels are high and will emerge from the crisis even higher. The sustainability of this debt, which depends on the duration of the health crisis, will largely determine whether or not this real crisis turns into a financial crisis.

[Note 1] Any regulation can be justified by market failure, i.e., the inability of competitive mechanisms to produce an optimal balance from a societal perspective. See Market Failure in Context, A. Marciano & S. Medema, 2015, History of Political Economy. Deposit insurance is necessary to prevent bank runs, which occur as a result of a coordination problem among depositors. Capital requirements stem primarily from the moral hazard problem introduced by deposit insurance.

[Note 2] This weighting is fixed by asset class in the standard model (e.g., 35% for a secured mortgage loan, 100% for a loan to a company rated between BBB+ and BB-) and recalculated when banks use an internal model. Finally, this principle applies to capital requirements for credit risk, which represents the bulk of a bank’s portfolio (in addition to requirements for market risk and operational risk).

[Note 3] To finance a loan of €1, a bank can therefore borrow a maximum of 93 cents. The highest quality capital corresponds exclusively to retained earnings and capital raised during capital increases. It contrasts with so-called « hybrid » financing instruments (between equity and debt), such as convertible bonds.

[Note 4] Mirroring the capital requirements is a maximum distributable amount: the maximum amount of dividends a bank can distribute without breaching these requirements. Any bank profits not distributed to shareholders are, by definition, retained on the balance sheet and reinforce the available capital. This maximum level may be lower than the expected dividends if the bank has incurred excessive losses.

[Note 5] As such, the countercyclical buffer is part of a new range of macroprudential instruments, which aim to take macroeconomic effects into account in the regulation of the financial system. They complement microprudential instruments, which seek to ensure the individual resilience of banks.

[Note 6] The British have already had the opportunity to lower their countercyclical buffer from 1% to 0% in connection with Brexit.

[Note 7] At the time of writing, this point is still under discussion.

[1] See the annual transparency exercise carried out by the European Banking Authority. Figures for thesecond quarter of 2019.

[2] Bank Capital Redux, O. Jorda, B. Richter, M. Schularick, and A. Taylor, forthcoming, Review of Economic Studies.

[3] Will the coronavirus crisis rehabilitate the banks?, Financial Times, April 1, 2020.

[4] Liquid-Claim Production, Risk Management, and Bank Capital Structure: Why High Leverage is Optimal for Banks, H. DeAngelo & R. Stulz, 2014, ECGI Finance Working Paper No. 356.

[5] The costs and benefits of bank capital – a review of the literature, Basel Committee on Banking Supervision, June 2019, Working Paper 37.

[6] Fallacies, Irrelevant Facts, and Myths in the Discussion of Capital Regulation: Why Bank Equity is Not Socially Expensive, A. Admati & P. DeMarzo & M. Hellwig & P. Pfleiderer, 2016, Stanford University Graduate School of Business Research Paper.

[7] The Cost of Capital, Corporation Finance and the Theory of Investment, F. Modigliani & M. Miller, 1958, American Economic Review.

[8] Optimal Bank Capital, D. Miles & J. Yang & G. Marcheggiano, 2012, The Economic Journal.

[9] EBA publishes 2018 EU-wide stress tests results, EBA, November 2, 2018, press release.

[10] Macroprudential Policy, Countercyclical Bank Capital Buffers and Credit Supply: Evidence from the Spanish Dynamic Provisioning Experiments, G. Jimenez & S. Ongena & J.-L. Peydro & J. Saurina Salas, 2015, European Banking Center Discussion Paper.

[11] Press release from the High Council for Financial Stability, April 2019

[12] ECB supports macroprudential policy actions taken in response to coronavirus outbreak, ECB, April 15, 2020, press release.

[13] ECB Banking Supervision provides further flexibility to banks in reaction to coronavirus, ECB, March 20, 2020, press release.

[14] ECB Banking Supervision provides temporary relief for capital requirements for market risk, April 16, 2020, press release.