In response to the Covid-19 crisis, the French government has deployed a wide range of measures to support the economy. Among these, state-guaranteed loans (PGE) have enabled companies to access cash financing on favorable terms, with the aim of mitigating the decline in activity. Between March and January 2020, €131.6 billion was granted to nearly 635,000 businesses.

Although these loans were a lifeline and necessary, they nevertheless added to the debt burden of French companies, which was already high before the crisis (76% of GDP in the first quarter of 2020). The question of converting PGE loans into equity or quasi-equity quickly arose, but no answers have been provided at this stage. The aim of this conversion is to prevent the PGE from ultimately weighing on companies’ solvency and/or reducing their ability to finance essential expenditure (e.g., investment and hiring).

A sharp deterioration in the financial sustainability of companies could have significant negative repercussions on employment (in the event of company failures leading to layoffs), for healthy companies (via customer-supplier relationships or via a general shortage of bank credit), for banks (which would have to increase their capital in proportion to the losses they would incur on their loans), or even for the State (which guarantees 80 to 90% of state-guaranteed loans).

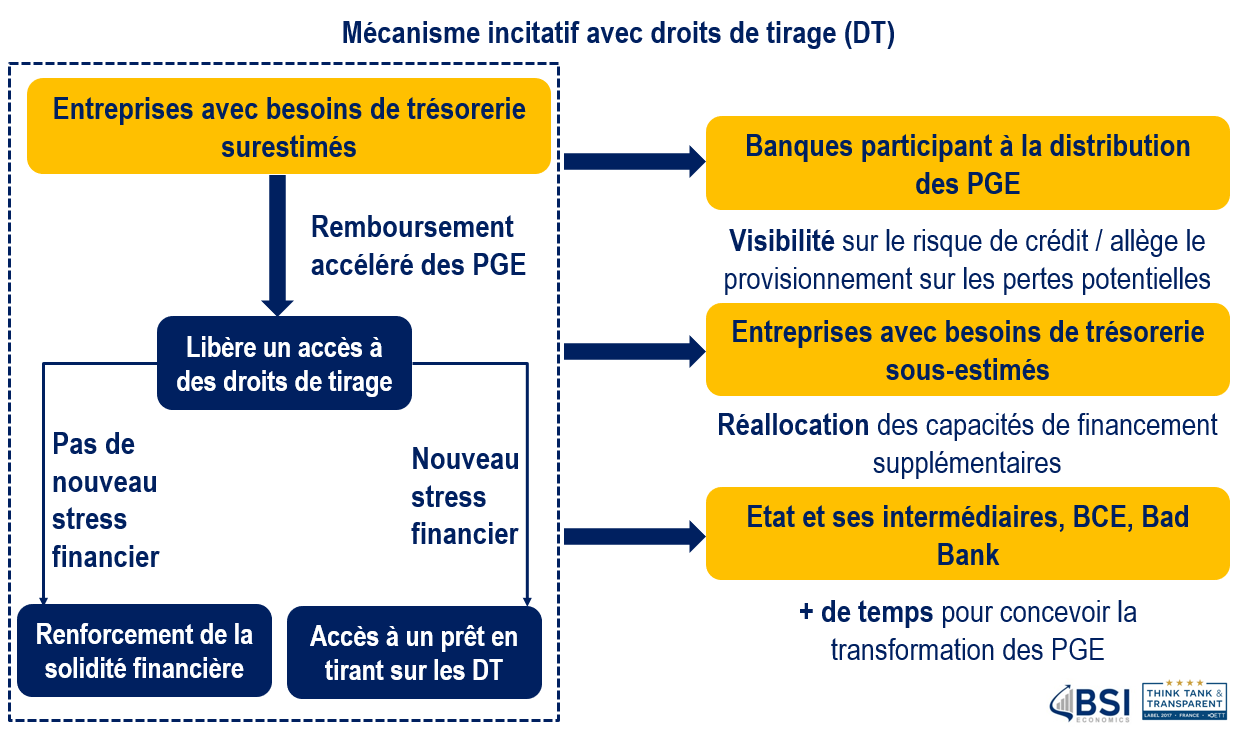

The independent think tank BSI Economics has examined this key issue and submitted several proposals in response to a request from the Finance Committee of the National Assembly concerning the trade-offs of the recovery plan. This article reviews the outlines of the proposal concerning the management of state-guaranteed loans, which would limit the risks associated with this « debt wall » through the implementation of a mechanism based on a system of incentives.