Abstract :

- Internal and external economic imbalances, doubts about the independence of the Central Bank, and diplomatic tensions with the United States caused the Turkish lira to plummet in the summer of 2018.

- Turkey is affected by significant structural problems, with banks in particular being in a difficult position. Double-digit inflation is eroding household purchasing power, and Turkish companies’ dollar (USD) debt has skyrocketed, making them vulnerable to exchange rate fluctuations.

- Financing the external deficit has become more complicated and costly since the US Federal Reserve began raising its key interest rates in response to the strong US economy.

- These issues also affect emerging countries, particularly those that depend on foreign capital to finance their external deficits.

This article traces the causes of the sharp fall in the Turkish lira since the summer of 2018. It presents the structural weaknesses of the Turkish economy and the international economic situation that is exacerbating them.

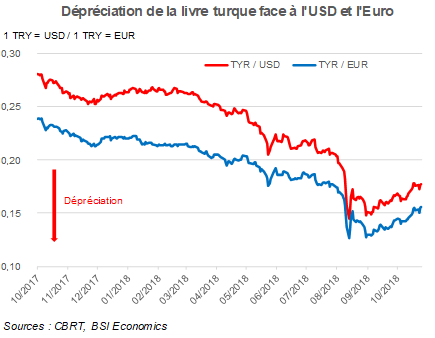

The Turkish lira, whose decline has accelerated since the beginning of August, has lost 32% of its value against the euro and 35% against the US dollar (USD) in 2018. This has led to high inflation due to the rising cost of imports. This price increase reached nearly 24.5% year-on-year in September and could reach 20.8% for 2018, according to forecasts announced by Turkish Finance Minister Berat Albayrak.

The depreciation of the lira began in line with the overall decline in emerging market currencies, amplified in Turkey by macroeconomic imbalances. The crisis worsened again with the tension in relations between Turkey and the United States during the summer. This diplomatic crisis was linked to the fate of American pastor Brunson, who was then detained in Turkey and whose release was demanded by President Trump. In response to Turkey’s refusal, the United States announced that it would double import taxes on Turkish steel and aluminum, from 25% and 10% to 50% and 20%, respectively. This announcement worried investors, who withdrew some of their capital from the country, accelerating the lira’s decline.

What are the weaknesses of the Turkish economy?

- Significant foreign currency debt

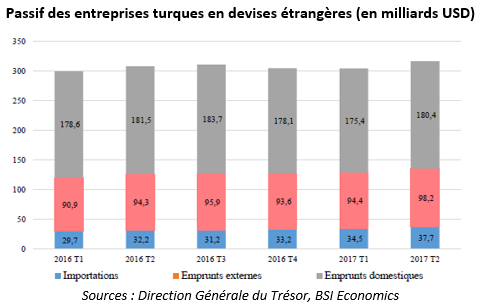

Despite its strong growth (7.4% in 2017), the Turkish economy has several weaknesses that make it vulnerable to external crises. One of the main causes of the current crisis is the massive foreign currency debt of the private sector, particularly in US dollars (USD). This high level of corporate foreign currency debt is due to insufficient savings by Turkish households and the underdevelopment of domestic capital markets. Corporate financing is therefore often obtained in foreign currencies, and this debt has made the private sector vulnerable to exchange rate fluctuations. The fall in the lira has automatically increased the cost of private debt in foreign currencies, causing repayment difficulties for the companies concerned. Turkish banks are affected not only by increasing corporate credit risk but also by refinancing risk, given their high level of short-term debt. Their refinancing costs are therefore likely to be high, particularly due to the tightening of global financial conditions.

- Weak and belated public intervention

The fall of the Turkish lira has been further exacerbated by the central bank’s reduced independence in steering monetary policy and by fears of escalating tensions with the United States. President Recep Tayyip Erdogan has spoken out against raising interest rates. However, the markets believe that only a significant rise in interest rates could stabilize the Turkish lira against other currencies. The lack of response from the CBRT (the Turkish Central Bank) during the summer severely undermined its independence and credibility, prolonging the fall of the lira.

But on September 13, the CBRT finally raised its main interest rate from 17.75% to 24% to stem the fall of the lira and halt inflation. It also announced that it would continue to « use all available levers to ensure price stability, » thereby marking its independence. The Turkish lira rose 5% against the USD the very next day. But this action is not a panacea for the Turkish economy’s problems. Rising oil prices are fueling inflation, which is significantly reducing real returns on investments in Turkey.

Furthermore, the rise in interest rates automatically leads to a slowdown in the country’s economic activity due to the increase in borrowing costs for households and, above all, for companies wishing to invest. In addition, the fall in the lira and the drying up of portfolio investments will cause significant delays, or even defaults, among companies unable to repay their loans denominated in dollars or euros. There remains considerable uncertainty about the ability of banks to manage their non-performing loans, of the government to set up a bad bank, and above all of the CBRT to curb inflation, which is fueling continued pressure on the Turkish lira.

- A large current account deficit

Turkey has a high current account deficit, at 7% of its GDP, due to its heavy dependence on imports and limited domestic savings. This imbalance could therefore be a source of financial fragility for Turkey if its current account deficit is not financed by foreign investment.

Foreign direct investment (FDI) represents a long-term interest in the country concerned by the rest of the world and is therefore the most stable means of financing. However, FDI covers only one-fifth of Turkey’s current account deficit. To meet its significant short-term financing needs, Turkey is also highly dependent on portfolio investment, i.e., short-term financial commitments. Turkey is therefore exposed to the volatility of financial markets.

This type of fragility exposes a country to strong pressure on its currency.

When the Fed (the US Central Bank) interest rates were close to zero as part of its ultra-accommodative policy, investors flocked to emerging economies with higher-yielding assets. But the United States is now engaged in a cycle of rising interest rates, leading to an appreciation of the USD and a decline in the value of emerging market currencies. This rise in the dollar is prompting investors, who doubt the solidity of fragile emerging countries, to leave these countries and invest their capital in the United States, where rising rates and interest rate differentials now offer a better risk/return ratio. The depreciation of the lira is therefore increasing inflation and borrowing costs for Turkish companies with dollar-denominated debt.

To avoid these harmful effects, one solution would be to limit the external deficit as much as possible. This would therefore act as a brake on investment and growth. However, Turkey needs to accumulate capital in order to invest and develop. Structurally, Turkey must borrow from the rest of the world because its domestic savings are low. This external balance constraint is therefore ineffective for Turkey, but remains inevitable in a context of rising interest rates in developed countries. Indeed, if the country maintains a current account deficit without being able to attract capital, it will suffer a balance of payments crisis, in other words a currency crisis, since its external deficit would not be financed. The value of its currency would then fall sharply. The sharp rise in interest rates by the Turkish central bank thus makes it possible to maintain the country’s attractiveness and mitigate capital outflows. This policy slows the fall of the Turkish currency, but at the cost of slowing growth.

Conclusion

Turkey has a savings shortfall that leads to a chronic external deficit, exacerbated by more expensive energy imports. The recent rate hike by the CBRT seems to have prevented capital flight despite diplomatic and trade tensions with the United States and to have alleviated international investors’ doubts about the independence of the Turkish Central Bank.

Turkey is not the only emerging market in this situation. Argentina also has a large current account deficit, exceeding 5% of its GDP, although the reasons behind the peso’s 50% depreciation against the USD differ from those in Turkey (massive public debt in Argentina).

In other emerging countries, the Fed’s policy has not triggered a sudden exodus of capital. This is therefore not a crisis affecting all emerging countries, but rather certain countries affected by both structural weaknesses and destabilizing political factors.

Sources:

Recent developments in Turkey clearly illustrate the nature of emerging market risk, Flash Economie, Natixis Research No. 945

Global outlook for fall 2018: still buoyant despite headwinds, Trésor-Eco, September 2018