Purpose of the article: This note aims to present the results of one of the simulations using global macroeconomic models, which show that the impact on the euro area would be limited in the event of a slowdown in China’s GDP growth, but significant if the adjustment were to be marked.

Summary:

- China’s economic growth has been slowing gradually since 2010.

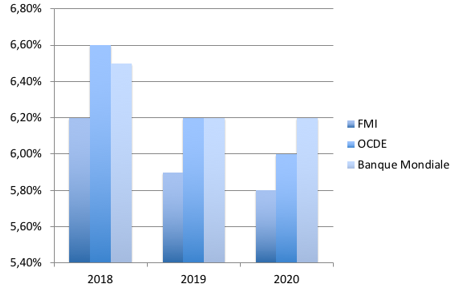

- According to the Organization for Economic Cooperation and Development (OECD), China’s growth is expected to moderate gradually to reach 6% by 2020, which is already directly affecting its main partners through various channels: trade, finance, and raw materials.

- According to simulations, excluding Germany, the eurozone as a whole would be less exposed than countries with strong bilateral trade relations with China. In the case of a « rapid rebalancing » (intermediate), the eurozone would be affected by a 0.3% decline in GDP in the event of a 3% decline in Chinese GDP smoothed over three years.

After several decades of expansion, China’s economic growth began to slow in 2010, falling from an annual rate of 10% since 1980 to around 6-7% in recent years. At the same time, China’s share of global GDP has risen from 4% in the late 1990s to nearly 17% today. Moving away from a model in which investment and exports played a major role, since 2010 the country has been shifting towards a model focused on domestic demand and private consumption.

Given (1) the size of the country, (2) its openness to trade, and (3) its dominant position as a consumer of raw materials, China’s transition may prove to be fundamental to the global economic outlook.

The country plays a dominant role in global goods and commodity markets (12% of oil consumption and 22% of global energy consumption), but remains less financially integrated than advanced economies, for example.

1. The current macroeconomic environment highlights the impact of the Chinese slowdown on the eurozone

In recent years, several institutions such as the OECD, the International Monetary Fund (IMF), and the European Central Bank (ECB) have raised the issue of China’s changing growth model and the possible repercussions for partner countries, particularly those in the eurozone. Against a backdrop of trade tensions and a more pronounced slowdown in the global economy[1], with China as the main driver of global growth, this issue is highly topical.

1.a) The latest data show a sharp decline in Chinese growth

China’s economic growth has been gradually slowing since 2010.Since 2017, the Chinese government has implemented policies aimed at limiting macro-financial imbalances, including tighter restrictions on access to mortgage credit for households, which has ultimately weighed on domestic demand. Trade tensions with the United States have added to the factors weighing on foreign trade.

According to the latest business climate surveys, activity slowed in 2018. The Caixin PMI index[2] fell sharply in December 2018 to below 50, its lowest level since 2016, indicating a contraction in activity, before recovering in March. Economic growth in 2018 was 6.6%, the lowest level since 1990.

According to the OECD, China’s growth is expected to moderate gradually to reach 6% by 2020. New fiscal stimulusmeasures are currently being implemented to boost growth (issuance of subnational government bonds to finance infrastructure projects, one-point reduction in the VAT rate) and monetary policy has been eased (lowering of the reserve requirement ratio). In the event of a further slowdown, additional measures to support economic activity could be introduced.

Figure 1: IMF, OECD, and World Bank growth forecasts for China

Sources: IMF, OECD, World Bank, BSI Economics

1.b) The contagion effect is being felt on eurozone exports, mainly through the case of Germany

In the eurozone, the latest IHS Markit index publications confirm downward pressure on activity, which is never a very good sign for economic strength. For the eurozone, the index had not been this low since June 2013, but at that time the trend was upward, whereas now it reflects a deterioration in activity.

One explanation lies in international trade, and this is particularly true in Germany. Germany is particularly hard hit by the contraction in trade due to its openness rate of over 44%, compared with 15% in the United States and 26% in France. Any shock to global trade has an immediate impact on our neighbor across the Rhine. The decline in orders in the capital goods and automotive sectors is at the heart of Germany’s slowdown. In addition, the decline in registrations in China also directly affects Germany (China is Germany’sfifth largest trading partner for exports, accounting for 6% of its exports). Germany has seen its export orders revised downwards from the March estimate (38.9 versus 39.5 initially for the IHS Markit PMI sub-index on export orders). For France, which is less exposed to the risk of a Chinese slowdown and global trade, the figure remains unchanged.

With 5,000 companies operating in China, the presence of German firms is unmatched by that of other European countries. In 2017, Germany accounted for 54% of eurozone exports to China, five times more than France. Germany’s strong specialization in the capital goods and automotive sectors, which was well suited to Chinese demand, particularly during the eurozone crisis, is now beginning to reveal itself as a potential vulnerability in the current context.

2. Quantifying the slowdown in the eurozone

To illustrate the impact of a slowdown in China on the eurozone, it is useful to identify the transmission channels and the various possible adjustment scenarios.

2.a) Transmission channels

International trade is the main transmission channel through which a shock to Chinese GDP could have a significant impact on the global economy. A decline in Chinese growth would reduce demand for goods and services produced by the rest of the world, thereby affecting global activity. Across the euro area as a whole, China’s direct trade links with the euro area are limited. Around 7% of exports outside the euro area are destined for China.

The financial channel is the second main channel through which a negative shock would have a very limited direct impact on global financial markets(equities, bonds, and foreign exchange), as China’s global financial integration is relatively weak compared to its trade integration. Nevertheless, a slowdown in activity in China and investor uncertainty could weigh on markets (equities, bonds, and foreign exchange) and, in particular, restrict the financial conditions of economic agents (households and businesses), which would ultimately penalize economic growth in the euro area. The financial links between China and the euro area are weaker: according to the ECB, China and Hong Kong account for 2.7% of bank claims outside the euro area and around 1% of euro area bank claims when intra-euro area claims are included.

Finally, the eurozone has very little negative exposure to the commodity price channel, whichmainly affects exporting countries, as China plays an important role in global goods and commodity markets (12% of oil consumption and 22% of global energy consumption).

2.b) Results of the ECB study: fairly limited impacts for the euro area in the event of a mild or rapid slowdown

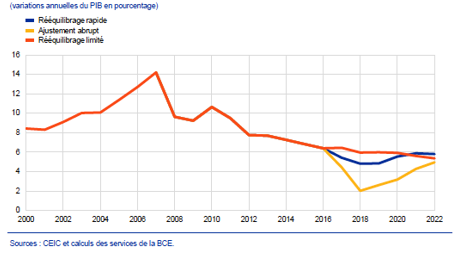

In order to understand the impact of a slowdown in growth in China, macroeconomic models are used to study the contagion effects on the global economy. The ECB has published a summary of the macroeconometric models used, presenting the results of several slowdown scenarios ranging from a « soft landing » to a « hard landing. »

Figure 2: Scenarios for China’s growth prospects

Sources: ECB, BSI Economics

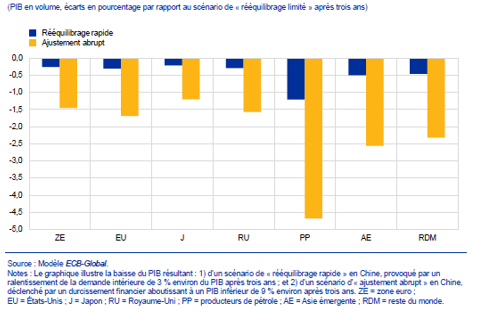

Looking at the results, the eurozone is less exposed than countries with strong trade links with China. In the case of a « rapid rebalancing » (intermediate), the eurozone would be affected by a 0.3 percentage point decline in GDP in the event of a 3 percentage point decline in Chinese GDP smoothed over three years. According to another recent OECD study, exports by volume would have a slightly greater impact on Germany than on the rest of the eurozone. Thus, a 2 pp decline in domestic demand smoothed over two years in China would reduce German GDP by 1.4 points, compared with 1 point for the eurozone as a whole.

The ECB’s « hard landing » scenario would be triggered by a significant tightening of financial conditions in China. This scenario implies a more pronounced slowdown in GDP growth in China, which would have a greater impact on the rest of the world than in the « rapid rebalancing » scenario. However, the different nature of the shock would also affect the magnitude of the repercussions. Despite weak financial integration with the rest of the world, ECB economists assume that tighter financial conditions in China would increase risk premiums globally. The shock observed in China would therefore spread both through the trade channel (via a decline in domestic demand) and through the financial channel, and consequently the impact on the rest of the world would be greater.

Chart 4 – Contagion effects: « rapid rebalancing » and « hard landing » scenarios

Sources: ECB, BSI Economics

Conclusion

China’s weight in global growth, its openness to trade, and its dominant position as a consumer of raw materials mean that its transformation could have a significant impact on global growth prospects. Various models measuring the impact of the Chinese slowdown suggest that the effects on the eurozone would be limited in the event of a moderate slowdown in Chinese GDP growth, but could be considerable in the event of a sudden shock. Germany, due to its mainly export-based model, would be the eurozone country most affected in the event of a sharp slowdown in China.

China’s slowdown would therefore have a contagion effect on: (1) commodity prices, (2) trade relations, (3) exchange rates, and (4) financial relations. Despite China’s weak integration with the eurozone and the rest of the world, a recession in China could trigger significant tensions in financial markets and ultimately tighten financial conditions for the rest of the world.

Bibliography

ECB (2017), « Growth and economic rebalancing in China and implications for the global economy and euro area economies, » ECB Economic Bulletin No. 7, pp. 37-59

Société Générale (2016), « China: Estimating the impact of a Chinese slowdown on the global economy, » Econote No. 32, July

OECD (2019), OECD Interim Economic Outlook, March.

Lallement R. (2017), « Socioeconomic changes in Germany: review and outlook, » Working Paper No. 2017-04, France Stratégie, March.

Gaulier G. et al. (2010), « China: End of the Extroverted Growth Model, » La Lettre du Cepii No. 298, April.