Abstract:

· The performance of private equity funds is unique in the world of asset management;

· There is a mystery surrounding the performance of private equity funds: given the various risks associated with private equity, such as concentration risk, liquidity risk, and legal risk, are the premiums paid sufficient to make them attractive?

· The financial and sovereign crisis of recent years has weakened private equity, but the performance achieved in a low interest rate environment keeps French private equity attractive to domestic and international investors, as French private equity performance has remained at a high level since 2012;

· Investments in leveraged buyouts (LBOs) remain at very high levels, while venture capital funds are posting positive but fragile performance.

Corporate financing in France is largely dominated by bank financing. With more than €900 billion in outstanding loans at the end of 2016, corporate credit is the primary source of external financing. Private equity represents an estimated €90 billion in outstanding loans. Nevertheless, it is the second largest source of external financing for French SMEs, ahead of capital increases on listed markets.

Although companies in France have strengthened their equity capital, particularly in the 1990s, they do not systematically turn to investment funds. Given the dilution that this entails and the loss of control in the case of majority stakes, SME managers are sometimes reluctant to engage in this type of investment, preferring traditional bank financing combined with self-financing.

Furthermore, private equity is characterized by high financial risk. Solvency (Solvency II) and liquidity (Basel III) reforms have forced large institutions such as banks and insurance companies to significantly reduce their contribution to French private equity, particularly between 2009 and 2012.

Presentation and definition of private equity

Private equity is a form of financing that developed in the United States in the second half of the 20th century. It took root in France in the 1970s and has grown significantly over the past several decades. It involves investing directly in the capital of unlisted companies through the purchase of shares (equity) or convertible bonds (quasi-equity). This industry comprises several segments. In France, we distinguish between four main types of investment, which we will briefly describe below:

· Venture capital involves acquiring equity in companies at the beginning of their life cycle. Investors can invest in future projects (seed capital), companies in the process of being created (start-up capital) or after their creation but before they reach profitability (post-creation).

· Growth capital is involved in the more advanced stages of a company’s life. Investors participate in capital increases of profitable companies in order to accelerate their growth, through external or internal growth;

· Buyout capital consists of company buyouts, generally accompanied by bank debt leverage (leveraged buyout). Investors intervene in companies that are well established in their market.

· Turnaround capital involves acquiring a stake in struggling companies with the aim of turning them around.

These investments are made through investment funds with very specific characteristics. In France, Professional Private Equity Funds (FPCI) predominate. In 2016, they accounted for 60% of investments made by management companies based in France. Other funds have also been set up to mobilize household savings in order to endow mutual funds (FCP). These are Local Investment Funds (FIP) and Innovation Mutual Funds (FCPI). These three categories account for nearly 70% of investments. The remaining 30% is made by venture capital companies (SCR) and financial holding companies under French or foreign law. Investments are made by management teams, which are generally specialized by business line or sector of activity of the target companies. This phenomenon is justified by the fact that private equity funds not only provide financing, but also their expertise, analytical capabilities, and networks, which maximize the chances of making the initial investment profitable.

Equity financing and the importance of management team specialization

Private equity in Europe and the United States is characterized by the specialization of management teams. In France in particular, specialization by sector, geography, and stage of development of companies is a phenomenon that has been observed in conjunction with the development, professionalization, and structuring of private equity funds in recent decades.

This specialization has been studied in particular by Paul Gompers (2009). The author has shown that in private equity, there is a positive relationship between the specialization of management teams and the future success of their investments. He observed that specialized teams performed better than generalist firms. Past performance plays a very important role in private equity, as it determines future fundraising. In order to exist, a private equity fund needs to raise funds from institutional investors such as banks, insurance companies, pension funds, and sovereign wealth funds. Past performance is used as a selling point for their product and enables management teams to create better-funded, more efficient funds, in the sense that the probability of missing out on an investment opportunity is low and they are better able to withstand negative economic shocks.

Unlike other asset classes, capital investment therefore results in specialization rather than diversification, which, in the case of traditional asset management, provides better risk coverage. Furthermore, unlike public equity, private equity is also characterized by high illiquidity. The shares held are not continuously traded on an open market. They therefore have no market price until the fund sells them. This makes the concept of exit essential and central to the analysis of investment fund performance. Capital gains or losses can only be accurately quantified when the shares are sold.

There are several exit routes for a private equity fund. In the case of positive exits, it can resell these shares to the company’s management, to an industrialist as part of a company buyout, to another private equity fund, or on the listed markets as part of an initial public offering (IPO). If the company is in difficulty, it can sell these shares to a turnaround company or to financial institutions, for example in the event of liquidation. However, the exit only takes place after a long holding period, averaging five to seven years. The performance of the funds during this period is therefore based solely on the management company’s estimate of the value of its holdings. This is private information, based on the managers’ expectations regarding the viability of the projects they finance.

The enigma of private equity performance

The outperformance of private equity is neither proven nor unanimously accepted. Therefore, after explaining the constraints associated with illiquidity and the specialization of private equity investment teams, this question raises the issue of the justification for this type of financing. Kaplan and Schoar (2005) tend to show that the net performance of US funds, in the case of venture capital, appears to be higher than the performance that would have been achieved on the markets. However, Moskowitz and Vissing-Jorgensen (2002) tend to justify capital investment by non-pecuniary advantages rather than by the outperformance of this asset class. These advantages may stem in particular from the control they have over the company.

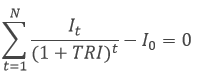

Before attempting to answer the question of private equity’s outperformance, it is worth recalling the elements used to measure the performance of capital investments. In order to quantify this, management teams calculate the internal rate of return (IRR) which, combined with the investment multiple, provides an understanding of the performance of investment funds.

By applying the Public Market Equivalent method, AFIC has demonstrated that, over a 10-year horizon, the net performance of French investment funds is twice that of the CAC 40 index. However, it is important to understand that higher returns do not necessarily mean better performance. In fact, at least two premiums must be added to an investment in private equity: the illiquidity premium and the risk of non-diversification. The key question is whether these premiums are properly valued and sufficient to justify bearing the risks inherent in private equity.

Stylized facts about private equity investments

The IRR of an investment fund is characterized by a J-shaped curve over time.

Graph 1. Illustration of private equity performance

Sources: BSI Economics

Depending on the performance of the investments in the investment fund, the overall performance of the fund only returns to positive territory after four or five years. The sources of performance come mainly from the creation of value in each of the fund’s holdings. This performance may be due to organic growth of the companies in the portfolio, i.e., by developing new markets or unlocking growth potential. But it may also be due to generating synergies and growth levers through the acquisition of new entities. This is referred to as external growth.

Furthermore, in the context of venture capital investment, the capital investor enables the company to unlock the debt capacity of innovative start-ups. Bank credit is not well suited to investment in innovative sectors because there is an information asymmetry between managers and lenders. The capital investor then acts as a signal that allows the lender to commit funds to the project because they have information that the project is considered profitable by management teams with proven expertise and privileged information.

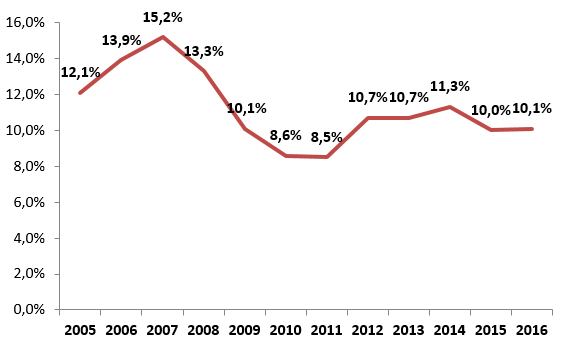

Performance history of French private equity

French private equity weathered the financial crisis well and has posted returns of over 10% since 2012.

Figure 2. Performance of French private equity funds

Sources: AFIC/EY, BSI Economics

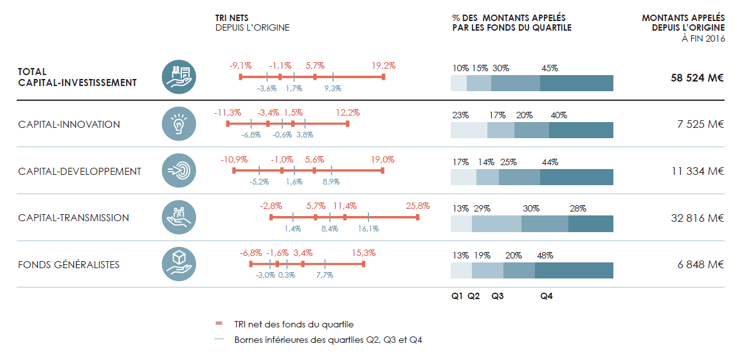

However, there are significant disparities depending on the stage of development of the companies in which the investment funds invest. LBO funds[3]are outperforming, with a median return of 8.4%, while innovation capital, which is riskier, has a median IRR of -0.6%, meaning that more than half of the funds are delivering negative returns to investors. However, this segment is heavily subsidized and investors can count on tax incentives. This exposes them to an additional risk: legal risk. France is characterized by highly volatile tax policies, meaning that today’s advantages may change in the future.

Figure 3. Performance of French private equity funds

Sources: AFIC/EY, BSI Economics

Conclusion

Private equity offers attractive returns and can be an alternative for institutional and individual investors looking to boost their investment performance by allocating a larger share to this asset class. However, fund performance varies widely, so it is advisable to diversify investments across several investment funds. Due to the specific nature of the business, the risk borne by management teams is subject to a high concentration risk due to the specialization of the teams.

The rapid development of crowdequity platforms offers an alternative way to boost individual investors’ savings. In the future, individuals wishing to invest in private equity will need to be aware of the specific characteristics of these investments in order to enable the sustainable development of this type of subscription and diversification of savings.

Appendices

IRR is calculated using the following formula:

The net IRR is the IRR achieved by an investor on their investment in a private equity vehicle, taking into account negative cash flows relating to successive capital calls and positive cash flows relating to distributions (in cash or securities) as well as the net asset value of the units still held in the vehicle on the calculation date (the Net Present Value or NPV).

The investment multiple is defined as follows:

![]()

The DPI or Distribution to Paid-in is the effective rate of return, i.e., the amount actually paid to investors relative to the capital called.

The RVPI ( Residual Value to Paid-in ) is the expected rate of return, i.e., the estimated value of the fund relative to the capital called.

In order to compare these indicators with other asset classes, Jagannathan, Ravi, and Morten Sorensen (2014) demonstrated and justified thePublic Market Equivalent(PME) method developed by Kaplan and Schoar (2005). The PME method makes it possible to replicate private equity flows on listed markets (for example, on an index such as the CAC 40), then calculate the IRR obtained on this index and compare its value with the IRR calculated on private equity funds.

Bibliography

Private Equity Performance: Returns, Persistence and Capital Flows Steve Kaplan and Antoinette Schoar, 2005

The Returns to Entrepreneurial Investment: A Private Equity Premium Puzzle?, Tobias J. Moskowitz and Annette Vissing-Jørgensen, 2002

Specialization and Success: Evidence from Venture Capital, Paul Gompers, Anna Kovner, and Josh Lerner, 2009

Financing Structure: The Contributions of Private Equity, Pierre-Michel Becquet, 2013

Private equity performance study, AFIC 2016

Private equity performance study, AFIC 2015

Value Creation Study, AFIC 2016