Abstract :

· Moldova’s GDP growth rebounded in 2016 and is expected to average around 4% in the medium term.

· However, Moldova faces several downside risks in the short term: parliamentary elections in fall 2018 could lead to significant fiscal slippage, while growth in Moldova’s main trading partners (Romania and Russia) could be lower than expected and affect Moldova’s growth.

· Regulation and supervision of the banking system have improved since the 2014 scandal, but significant challenges remain.

· The resumption of international aid in the second half of 2016 is good news for the country, but serves as a reminder of its dependence.

· The business climate is improving despite persistent corruption.

After recording a technical recession in 2015, Moldovan economic activity rebounded in 2016 (+4%) thanks to private consumption and a sharp increase in agricultural production. GDP growth is expected to maintain this pace in the medium term. Moldova is expected to continue reorienting its foreign trade towards the European Union (Romania in particular) at the expense of the Commonwealth of Independent States (Russia and Ukraine in particular). Supervision and regulation continue to be strengthened in the wake of the 2014 banking scandal, but significant challenges remain. The stabilization of the political and economic situation has led to a resumption of international aid, on which Moldova is dependent, and an improvement in the business climate despite endemic corruption. With the 2018 parliamentary elections approaching, there are many reforms to be carried out. Despite the slow pace of implementation, Moldova nevertheless seems to be on the right track.

1. Economic activity rebounded in 2016 thanks to private consumption and good harvests

After GDP growth of 4.8% in 2014, Moldova experienced a technical recession in 2015 (-0.4%), due in particular to poor harvests and a decline in household consumption, which was affected by the fall in remittances from migrants (16% of GDP) following the Russian crisis. However, the Moldovan economy rebounded in 2016. GDP growth reached 4.0%, supported by strong growth in agricultural production (+18%, with this sector accounting for 12% of GDP) and wage increases (+14.8%)[1]. As a result, household consumption was buoyant and inventories were replenished, with these two components contributing a total of 5.4 pp to GDP growth. Also noteworthy was the smaller contraction in migrant remittances (-6% compared with -30% in 2015). Conversely, net exports and investment weighed on growth (negative contribution to GDP growth of 1.3 pp and 1.1 pp respectively).

In 2017, GDP growth is expected to reach 4.5% according to the IMF and 3.8% on average over the period 2018-2020, supported by private consumption. Higher wages (+13.2% year-on-year in the second quarter of 2017) and a more accommodative fiscal policy are expected to benefit households, while exports are expected to be supported by restocking following the good harvests of 2016. As a result, poverty is expected to decline but remain at a high level (9.6% of the population in 2015[2] ), while the human development index (0.699 in 2016) is expected to improve slightly.

Figure 1. GDP growth is expected to stabilize in the medium term, in line with the dynamics of workers’ remittances and consumption

Several downside risks could have a negative impact on the economy if they materialize:

· Scheduled for fall 2018, parliamentary elections[3] could slow the pace of reforms and result in significant budget slippage.

· Growth forecasts for Moldova’s main trading partners (particularly Romania and Russia) could be lower than expected and affect Moldova’s growth;

· High emigration and low birth rates pose a problem for pension financing in the medium term, despite the recent pension reform;

· Moldova also faces several challenges: an aging population, global warming (causing severe droughts and floods since 2007), and the sustainability of growth in a context of low productivity gains and low labor force participation (38%).

Inflation is expected to accelerate slightly in 2017 (+7.3% year-on-year in August) due to higher utility prices and rising commodity prices. In the medium term, inflation is expected to remain within its target range (5% with a margin of fluctuation of +/-1.5pp), averaging 5.4% annually over the period 2018-2020, according to the IMF.

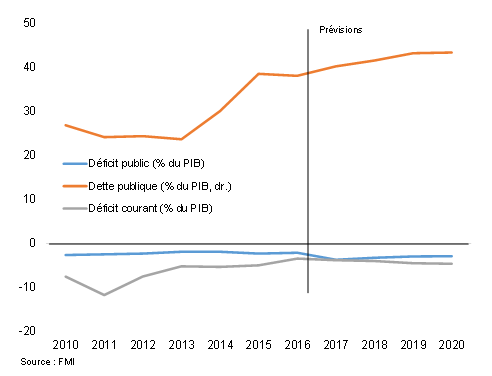

The current account deficit narrowed from -5% of GDP in 2015 to -3.4% in 2016. However, due to low FDI, the current account deficit was mainly financed by debt, which represents a medium-term risk due to potentially high refinancing costs. This is particularly true given that imports are twice as high as exports in value terms, resulting in a structural current account deficit.

Figure 2. Public and current account deficits are likely to persist in the medium term, with public debt continuing to rise gradually

Moldova continues to be relatively affected by the measures adopted by Russia (11% of exports) with the embargo or increase in taxes on Moldovan agricultural products) following the agreement with the EU signed in 2014 and which came into force in 2016. Begun in the early 2000s, Moldova has accelerated the process of reorienting its exports following the retention measures imposed by Russia. Moldovan exports are now more focused on the EU (65% of total exports, +10% since 2013) than the CIS (19% of exports, -49% since 2013). Russia (-55%) and Ukraine (-61%) have been particularly affected, while Romania is reaping the full benefits of this reorientation (+21%, 24.4% of exports).

2. Regulation and supervision of the banking system is improving, but significant challenges remain

The Moldovan banking sector is very small, comprising 11 banking institutions (three of which closed in 2015). Foreign presence is limited (four banks, 26% of total assets). The rate of banking intermediation remains low, with outstanding loans representing only 26% of GDP (compared to 43% in Ukraine and 100% in the eurozone).

Two-thirds of assets are held by three banks: MAIB (27% of total banking assets), MICB (20%) and Victoria Bank (17%). These three banks are under special supervision by the National Bank of Moldova (BNM) following the disappearance of $1 billion at the end of 2014 (15% of GDP). Since then, MAIB and Victoria Bank have been placed under special supervision by the NBM, while MICB is under temporary administration by the NBM. After conducting a series of audits, the NBM seized 43% of MAIB’s shares and 60% of MICB’s shares due to a lack of transparency on the part of these shareholders. These shares must be resold on the market in order to attract new, more transparent private investors. Despite the opacity of the sector, tangible progress has been made in terms of regulation, supervision, and the independence of the central bank.

Financial stability has improved, although many challenges remain. Deposits increased by 10% in 2016 and the level of capital (30%) is well above the regulatory minimum of 16%. On the other hand, credit growth remains negative despite a 10.5 pp decline in the BNM’s key interest rate in 2016, resulting in part from excess liquidity in banks. The non-performing loan (NPL) ratio continues to rise (18% of total loans, forecast for 2017), reflecting the reclassification of loans following audits conducted after the banking scandal.

3. Moldova remains dependent on international aid

Suspended in 2015 following the banking scandal, international financial aid (4.6% of GDP in 2015 according to the World Bank) resumed in the second half of 2016. The main donors are the IMF, the World Bank, the EU, and Romania.

Moldova benefits from:

(i) A €150 million loan granted in 2015 by Romania, with disbursements beginning in August 2016;

(ii) A three-year €150 million loan from the IMF granted in November 2016;

(iii) €100 million in financial assistance from the EU (€60 million in loans and €40 million in grants) approved by Council decision in April 2017;

(iv) The essential presence of the World Bank, which is currently committed to providing USD 360 million spread across nine projects (education, health, business support, tax administration, roads, agriculture, etc.). It should also be noted that in July 2017, the World Bank adopted the new 2018-2021 Partnership Agreement with Moldova. This agreement will support the improvement of the country’s economic governance and public services, as well as the development of human capital.

The resumption of international aid has freed the government from financial constraints. Several investment expenditures had to be postponed, resulting in a 2% decline in public spending. Budget execution (structurally in deficit) was then better than expected (-2.1% of GDP versus 3.5% budgeted). The resumption of international aid would coincide with a more accommodative budget execution in 2017: the budget deficit would stand at 3.7% of GDP according to the IMF. Public debt would increase slightly to 40% of GDP, a level much higher than in 2013 (24% of GDP).

4. The business climate is improving despite persistent corruption

Moldova ranks44th in the World Bank’s Doing Business 2017 ranking (+3 places compared to 2016). The main improvements concern access to electricity, which remains limited, and tax payments. Conversely, the processing of building permits remains very poor, particularly in terms of the time taken to obtain them (276 days on average compared with 150 in OECD countries).

Corruption persists and is even increasing. Moldova fell 20 places in 2016 in Transparency International’s Corruption Perceptions Index, to123rd place. This is accompanied by very low confidence in public institutions, but also by an erosion of confidence among private investors and international organizations. Several measures have already been adopted in the past, but implementation remains fragile. A major reform of the judicial system is currently being carried out by the government in order to make institutions more independent and transparent (doubling of judges’ salaries, renewal of 25% of their staff, etc.).

Conclusion

Weak institutions and governance, the small size of the economy, and demographics continue to make the situation volatile in the short and medium term, while the country’s geographical position creates long-term uncertainty. Many significant challenges remain: fighting corruption, reducing poverty, improving governance, independence, and transparency in the public and banking sectors, etc.

Nevertheless, Moldova appears to be on the right track. The political and economic situation has stabilized since 2014 and numerous reforms are underway (judicial system, energy sector, education, public administration). In addition, the Moldovan economy is continuing its transition, becoming less dependent on the agricultural sector (12% of GDP in 2016 compared to 24% in 2004) and more focused on services (46%, 40%) and foreign trade (17%, 11%).

Finally, dialogue and cooperation between the country and international institutions (which play an essential role in the country) will be important in the run-up to the 2018 legislative elections and in the longer term.

[1]The average monthly salary is around EUR 240.

[2]For the record, the poverty rate was 21.9% in 2010, according to the UNDP. The poverty line is USD 1.9 per day.

[3]For the record, the current Prime Minister is Pavel Filip (Democratic Party).

[4]External debt has increased by 15 pp in two years.

[5]These three banks granted loans totaling $1 billion shortly before the parliamentary elections on November 30, 2014. The recipients of these loans havenot been identified.

[6]There are 52,300 companies in Moldova, 98.7% of which are SMEs.

[7]For example, the World Bank is conducting an energy efficiency project in the capital (Chisinau) to reduce household bills. Between January and March, one-fifth of household expenditure is devoted to energy costs, according to the Bank.

[8]Moody’s has given Moldova a B3 sovereign rating (highly speculative category).