Abstract :

- Brazil has very high foreign exchange reserves, well above IMF recommendations;

- However, these foreign exchange reserves generate budgetary costs of around 2.5% of GDP per year, mainly due to the interest rate differential between central banks;

- With the accommodative local monetary cycle now over and public debt dynamics unfavorable, the question arises as to whether part of the reserves should be sold in order to reduce public debt.

- Indeed, the expected gains from selling excess reserves remain significant, while the exchange rate risk remains uncertain and will depend on the gradual nature of the implementation.

This article discusses the risks and benefits associated with the very high level of foreign exchange reserves in certain emerging countries. This is particularly the case in Brazil, where high interest rates are generating budgetary costs. The expected gains from selling foreign exchange reserves could prove substantial, especially in the current environment.

Foreign exchange reserves are assets held mainly in foreign currencies and gold by central banks. Foreign exchange reserves can also take the form of Treasury bills and bonds issued by various governments. These enable central banks to intervene in the foreign exchange market in order to regulate their currency rates. Reserves therefore offer room for maneuver in terms of protecting a country’s currency, as well as for foreign investors.

However, maintaining a level of foreign exchange reserves generates costs and benefits in various respects. Developing countries with high interest rates, such as Brazil, often have a positive cost of maintaining these foreign exchange reserves. Brazil, whose reserves have stabilized at over USD 350 billion since 2011, ended a strong cycle of monetary easing by lowering key interest rates from 14.25% to 6.50% between 2016 and early 2018. Furthermore, its public debt remains at a worrying level—84% of GDP at the beginning of 2018, set to reach 100% by 2023, according to the IMF, with a projected public deficit of 8.3% of GDP in 2018. In this context, the question arises as to whether foreign exchange reserves should be maintained at such a high level.

1) The dynamics of foreign exchange reserves in emerging economies and Brazil

1.A) Since the 2008 crisis

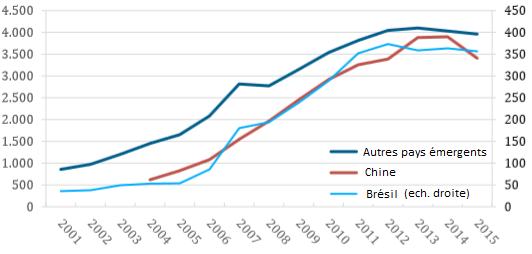

Brazil has followed the global trend in foreign exchange reserves, increasing its reserves sharply before the 2008 crisis, before stabilizing them at around $350 billion in 2011. This trend is also intrinsic to all emerging countries, as shown in Figure 1 below. China saw its reserves decline in 2014, contributing to a slow but significant global reduction in foreign exchange reserves (see BSI Economics article ).

Chart 1 – Foreign exchange reserves of emerging countries, in billions of USD

Sources: IMF, BC, BSI Economics

1.B) Changes in the cost of maintaining these foreign exchange reserves

Maintaining foreign exchange reserves generates costs and benefits in various respects. First, the cost of foreign exchange reserves is generally measured by the interest rate differential between interest rates in the rest of the world and domestic interest rates, i.e., the central bank’s area of jurisdiction. It can also be measured in terms of opportunity costs, for example if these reserves were used differently. Conversely, the benefits are measured mainly in terms of confidence, i.e., a lower risk premium because agents know that the central bank can intervene in the foreign exchange market in the event of a crisis. These reserves thus provide additional assurance that a flexible exchange rate regime will be maintained, which remains loosely administered in Brazil.

Developing countries with high interest rates therefore often have a positive cost of maintaining these foreign exchange reserves, especially when rates are low in the United States or the euro zone, as is currently the case. This raises the question of the optimal level of foreign exchange reserves: between protection and the ability to intervene in the foreign exchange market and the cost of maintaining them. It is also important to give foreign exchange reserves a guarantee of credibility for certain economies. These economies are indeed more exposed to large capital outflows or a sudden interruption in capital inflows.

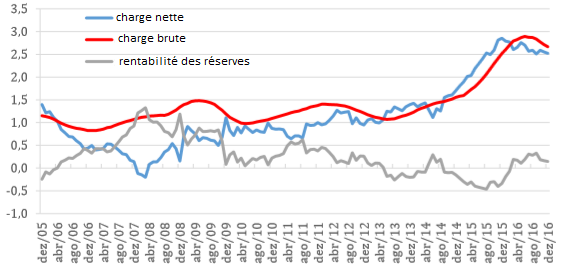

Figure 2 below shows that the cost associated with these foreign exchange reserves is currently around 2.5% of GDP per year, which remains a very high level.

Figure 2 – Cost of maintaining foreign exchange reserves as a percentage of GDP

Sources: IMF, BC, BSI Economics

2) Traditional parameters for foreign exchange reserves

2.A) Optimal levels

There are several variables that can be used to anchor the characteristics of certain countries (months of imports, external debt, short-term debt, current account balance) to an optimal level of foreign exchange reserves, i.e., the level at which their protective effect would be maximized. The aim is to ensure that a balance of payments crisis does not occur and that a country is able to pay for its imports, its external debt held in foreign currency, its short-term debt, and its current account deficit, according to the Greenspan-Guidotti criteria. The table below provides a typology of the criteria and shows the relationship between the actual level of foreign exchange reserves and the calculated optimal level. The IMF also defines an optimal level known as ARA ( Assessing Reserve Adequacy).

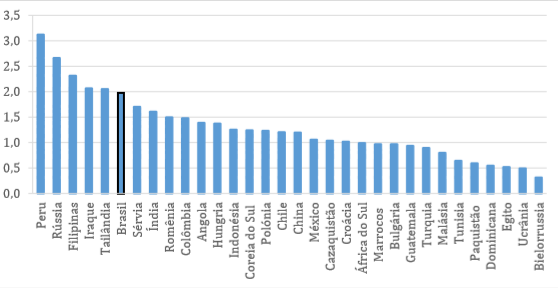

2. B) Comparison with the ARA level recommended by the IMF

The level of foreign exchange reserves is thus twice as high as the IMF’s recommendations. However, at the international level, Brazil rankssixth in terms of the ratio between its reserve level and the optimal level, behind Peru, Russia, the Philippines, Iraq, and Thailand. This comparison tends to put into perspective the fact that Brazil has excessively high reserves.

Figure 3 – Ratio of foreign exchange reserves to the IMF’s ARA variable, 2015

Sources: IMF, BC, BSI Economics

3) The optimal level in light of the structural depreciation of the Brazilian real

3.A) Accommodative monetary cycle, depreciation of the real, and the BCB’s response

Between late 2016 and early 2018, in order to support the recovery of the Brazilian economy, and with inflation under control, the Central Bank of Brazil (BCB) pursued an accommodative monetary policy, lowering its SELIC key rate from 14.25% to 6.50%. This policy ran counter to the normalization of US monetary policy. As mentioned in the previous BSI Economics paper on Brazil, the real has since depreciated steadily by 25% against the dollar in one year, in line with other emerging market currencies. This accommodative cycle limits the risk of a liquidity contraction that would result from a decline in the BCB’s foreign exchange reserves.

3.B) Foreign exchange reserves to reduce or cancel part of the public debt?

While the main concern for the Brazilian economy remains the dynamics of public spending, which is constitutionally guaranteed by the pension system that is about to become obsolete, the sale of part of the foreign exchange reserves would have two effects:

- In the short term, it would cancel part of the public debt, and therefore the future burden of this debt, which would have a positive effect on the economy’s exchange rate and thus encourage investment.

- In the medium term, the burden of maintaining reserves would be reduced, which would limit the increase in public debt.

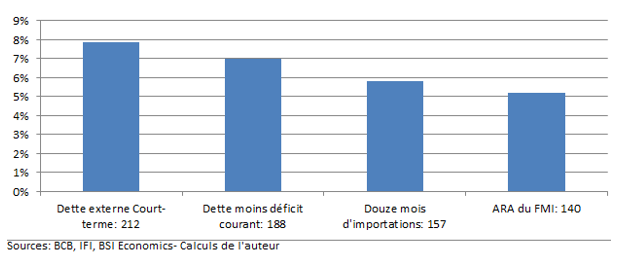

The IFI, an independent economic institute attached to the Brazilian Senate, has calculated the potential gains based on the reduction in reserves. Similarly, this study shows the expected gains from a sale of foreign exchange reserves. Based on the calculation considered to be the optimal level (see table above), a so-called surplus level of these reserves is calculated. Here, Figure 4 shows the level of surplus reserves based on the calculation chosen to characterize the optimal level of foreign exchange reserves. Taking into account international metrics and the trend at the end of 2016 of USD 360 billion in reserves, these surpluses represent between USD 140 and 212 billion. For Brazil, these surpluses represent between 5 and 8 points of GDP in debt to be canceled in the short term. This is a significant amount, which could provide real relief to economic agents concerned about Brazil’s public debt. In the chart below, the surpluses calculated in billions of dollars according to the metric considered (on the x-axis) refer to the potential gain from debt cancellation calculated as a share of GDP.

Chart 4 – Estimated potential gains (as a % of GDP) based on surplus reserves (in billions of USD)

Sources: IMF, BC, BSI Economics

It should also be noted that a decline in foreign exchange reserves could entail parallel risks, particularly depending on how these surplus reserves are used. According to the IFI, the main risk is the use of reserves for primary expenditure rather than for public debt cancellation. The exchange rate risk remains fairly uncertain. In particular, the BCB uses a flexible exchange rate regime and only intervenes in the event of panic. Given the profile of its public debt, which is largely domestic, and its reserve cushion, the risk of panic remains moderate in the event of a gradual sale of assets. The gradual implementation would make it possible to counter currency risk by observing the reaction of economic agents.

Conclusion

Brazil appears to be protected for the time being from the balance of payments crises currently experienced by other emerging countries such as Turkey and Argentina. Its level of foreign exchange reserves would indeed limit the depreciation of the real in the face of the normalization of US monetary policy. However, with economic growth remaining weak (1.5% expected in 2018 according to the BCB), the budgetary situation remains a concern and is an issue in the presidential election. Beyond fiscal and structural measures to limit the endemic rise in public debt, it would therefore be advisable to consider selling foreign exchange reserves as a gradual solution to cancel part of the debt. This solution is all the more relevant as it is in line with the flexible exchange rate regime adopted by the BCB.

Sources:

- BSI Economics and foreign exchange reserves: http://www.bsi-economics.org/749-brcpecrcf

- BSI Economics and Brazil: http://www.bsi-economics.org/831-bresil-spirale-taux-interet-jt

- IFI study on foreign exchange reserves: http://www2.senado.leg.br/bdsf/bitstream/handle/id/529487/EE_Reservas_Internacionais.pdf?sequence=1

- IMF, Article IV: https://www.imf.org/~/media/Files/Publications/CR/2018/cr18253.ashx

- BCB: https://www.bcb.gov.br/pt-br/#!/n/RESERVA