Abstract :

· R&D and innovation are important factors in the growth of so-called « knowledge economies. » In 2015, France devoted 2.2% of its GDP to domestic R&D expenditure (R&D expenditure by businesses, higher education institutions, and research organizations), which is slightly above the European average (2%);

· The innovation support system in France is mainly based on indirect aid through the research tax credit (CIR), which cost €5.5 billion in 2015. Most studies estimate that the CIR is relatively effective in encouraging investment in R&D;

· The innovation support system in France has become increasingly complex. The multiplicity of mechanisms and actors tends to make it difficult for public authorities to steer policy.

Since 1990, developed countries have gradually shifted from an industrial economy to a globalized and financialized knowledge economy. Economist Elie Cohen distinguishes three dimensions to this new economy: R&D and innovation have become important factors in growth dynamics, new sectors specific to the knowledge economy have developed (e.g., the digital health sector), and the share of knowledge activities within traditional activities has increased. This transformation towards a knowledge-based economy is accompanied by a policy of supporting innovation.

Innovation is the result of investment choices that are influenced by public policy. In a broad sense, innovation support policy includes all policies aimed at ensuring an environment conducive to the development of innovation. In fact, this includes education and research policies, as well as labor market policies, competition and intellectual property policies, taxation, etc. Here, we will focus on innovation support policies for businesses that involve subsidies, tax incentives, and human capital development.

The National Commission for the Evaluation of Innovation Policies (CNEPI) distinguishes between three types of instruments supporting innovation in France: direct subsidies, loans, and equity investments; human capital development and cooperation between actors; and indirect tax incentives and social security contribution relief.

1. The innovation support system has become more fragmented

In 2015, innovation support mechanisms provided by the State and its public operators amounted to €8.5 billion, compared with just €3.5 billion in 2000. In the space of fifteen years, the landscape has changed significantly with the development of a genuine policy to support innovation, the proliferation of instruments, and the emergence of new operators.

Innovation policiesreally took off in the late 1990s thanks to closer coordination between research policy and industrial policy. The Research and Innovation Act (1999) was a first step toward further promoting the results of public research by allowing researchers and academics to file patents and create startups. The law also led to the emergence of around 30 public incubators to help create innovative companies based on the results of public research (e.g., the Paris Biotech Santé incubator founded in 2000 by Paris Descartes University, ESSEC, Ecole Centrale Paris, and INSERM).

Innovation policies have several justifications from an economic point of view. First, public measures aimed at encouraging private investment in R&D are based on the idea that the level of private investment in R&D is below its socially optimal level. Indeed, since companies cannot reap all the benefits of their R&D investments, they tend to underinvest in R&D, which limits the potential for innovation at the national level. Public intervention can also aim to promote cooperation between actors, for example by reducing barriers to technology transfer or by capitalizing on R&D synergies.

Over the past fifteen years or so, new players have emerged in the ecosystem. In addition to traditional players such as the state and its public operators, regions have taken on an important role by making more regular use of the instruments made available to them by the European Union, such as subsidies from the European Regional Development Fund (ERDF). In 2015, subsidies ultimately originating from the regions accounted for 15.2% of total innovation subsidies, compared with 5.4% in 2000. In addition, access to financing for SMEs has improved with the creation in 2005 of EPIC OSEO to compensate for the lack of financing during periods of low economic activity. The public investment bank BpiFrance, created from the merger of the Strategic Investment Fund, Caisse des Dépôts Entreprises, and OSEO, will take over this role from 2012. In 2010, the Commissariat général à l’investissement (CGI) was created with the aim of managing the French government’s major investment program (PIA: programme d’investissements d’avenir). In 2015, these innovation programs accounted for 57% of the total amount of subsidies granted. Finally, the National Research Agency (ANR) was created in 2005 to finance scientific research projects and, in particular, to develop partnership-based research through the Carnot Institutes. The emergence of these new operators also explains the proliferation of schemes over the last fifteen years.

The National Commission for the Evaluation of Innovation Policies notes that the number of schemes managed by the State and its operators doubled between 2000 and 2015, rising from 30 in 2000 to 62 in 2015. This increase in the number of schemes has resulted in an average decrease in the funds allocated to each instrument. While the proliferation of instruments makes it possible to cover a wider field and thus provide more targeted support to businesses, the question of how to effectively manage all of these schemes arises. In addition, the increase in the number of instruments has been accompanied by a higher rate of renewal of these schemes, which can be explained in part by the need to adapt to a particularly changing environment. Nevertheless, the complexity and instability of innovation support tools may discourage less informed and less organized companies that would otherwise be eligible for these schemes.

2. Innovation support policy is mainly based on tax incentives

The direct support system (grants, loans, and equity investments) has the advantage of allowing for the targeting of supported investment projects and is perfectly suited to a strategic vision of innovation policy. Apart from the defense sector, aeronautics and electronics are the sectors that benefit most from direct aid. Several players are involved in direct support for innovation: the regions, the Carnot institutes attached to the ANR, BpiFrance, and more generally the various operators in charge of the PIA. BpiFrance offers a range of innovation support measures, including grants, repayable advances, zero-interest loans, guarantees, and equity investments.

The CIFRE program was launched in 1981 with a view to developing human capital. This program aims to strengthen the links between the business world and public research by co-financing the training of a doctoral student recruited by a company for a research assignment. This contract must be part of the company’s R&D strategy and is carried out in conjunction with a research laboratory. In 2015, the annual cost of the CIFRE program amounted to €52 million. Competitiveness clusters, created in 2004, also play an important role in increasing cooperation between stakeholders. These clusters, of which there are 71, bring together companies, schools, universities, and research laboratories. Collaborative R&D projects emerging from these clusters may receive specific public funding following a call for projects.

Tax incentives account for the majority of funds available to support innovation (€6.4 billion in 2015) and are mainly attributable to the research tax credit (CIR), which has become increasingly important over time (€5.5 billion in 2015, or 0.26% of GDP). The CIR, created in 1983, is a tax credit that encourages companies to increase their R&D spending. Before 2003, the credit was only granted to companies that increased their R&D spending. Between 2003 and 2008, the level of spending was included in the calculation of the tax credit in the same way as its evolution. Finally, since 2008, only the level of R&D expenditure has been taken into account in the calculation of the CIR. The tax credit is equal to 30% of R&D expenditure when this is less than or equal to €100 million and 5% above €100 million. Since 2013, in parallel with the CIR, an innovation tax credit (CII) has been created for SMEs. This allows them to benefit from a tax credit of 20% of the expenditure necessary for the design and/or production of prototypes or the installation of a new product. The Young Innovative Company (JEI) scheme, launched in 2004, offers social security exemptions for SMEs less than eight years old that devote at least 15% of their turnover to R&D. In 2013, 3,100 SMEs benefited from this system.

3. The performance of the French system remains improvable

France performs averagely in terms of the volume of its R&D activities, with domestic R&D expenditure as a percentage of GDP at 2.2% in 2015 (average of 2.1% in the eurozone). This level is below the 3% target set at the European summits in Lisbon in 2000 and Barcelona in 2002. France’s R&D intensity has increased slightly in recent years despite the negative effects of deindustrialization and the shift towards a service economy. Between 1995 and 2014, the share of services in value added rose from 72.7% to 78.7% in France. The OECD notes that France invests less in R&D than its competitors, particularly Germany. One reason for this may be that France appears to be more competitive in sectors that are less R&D-intensive, such as luxury goods and agri-food, and that the manufacturing sector in France is relatively small (11% of GDP in 2014 in France compared with 23% in Germany).

As the OECD notes, public intervention in France is very present at all levels of the production chain, from the creation of an ecosystem for the development of innovative companies to the financing of projects. However, this strong intervention does not seem to be reflected in France’s performance. These disappointing results can be explained by the presence of numerous obstacles to the development of innovation: a lack of openness or flexibility in the labor and product markets, a heavy and complex corporate tax system that undergoes regular changes from one year to the next, and difficulties in accessing financing for businesses. On this last point, it appears that venture capital financing is difficult to obtain in the seed phase, whereas it is abundant in the expansion phase (see this article on this subject). In general, the OECD considers that public intervention in France is not always consistent and that the multiplicity of measures does not allow for strategic orientation.

There is no consensus among developed countries on the optimal choice of instruments to support innovation. In some countries, such as France, Canada, and South Korea, tax incentives predominate, while in Germany, Sweden, and Finland, a system based on direct aid (subsidies) is preferred. However, these countries are all part of the group of countries with high R&D intensity. Nevertheless, over the past 20 years, there has been an increase in the number of countries using tax instruments. France remains the most generous country for this type of instrument (0.26% of its GDP), while Canada ranks second with 0.21%.

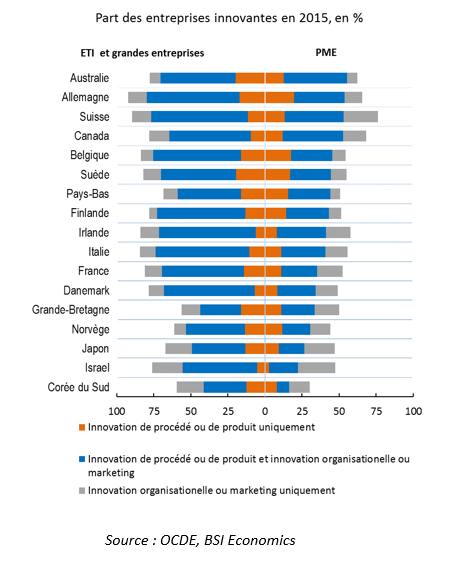

The innovation support system in France has been the subject of several evaluations. Studies have focused on the CIR, which accounts for a very large share of aid (€5.5 billion out of €8.5 billion). Since the 2008 reform, which made the CIR more accessible thanks to administrative simplification, the number of SMEs benefiting from the CIR has increased significantly. Nevertheless, the share of innovative companies remains significantly lower for SMEs (fewer than 250 employees) than for medium-sized and large companies (see chart below). Studies conducted to assess whether the credit granted to companies replaced R&D expenditure or actually increased R&D expenditure mostly conclude that the aid has an additive effect on R&D expenditure. In other words, one euro of aid generates at least one euro of R&D expenditure. In addition, the National Commission for the Evaluation of Innovation Policies (CNEPI), created in 2014, supports and coordinates various ongoing research projects to assess the overall effects of the innovation support system.

Conclusion

France has a public innovation support system for businesses that has become more fragmented with the emergence of new players. Indirect innovation support, through research tax credits, has become the main tool used by public authorities over time, while the share of direct support (grants, aid, loans) has decreased. Finally, better coordination and clarity of the mechanisms could improve France’s performance.

Bibliography:

– Fifteen years of innovation policy in France, report by the National Commission for the Evaluation of Innovation Policy. January 2016.

– Innovation in France, international positioning indicators. 2016 edition.

– Impact of the 2008 CIR reform on R&D and innovation. Bozio

– Evaluation of the impact of direct and indirect aid to R&D in France, Lhuillery, Marino, Parrotta. 2013

– OECD reviews of innovation policies. France 2014.

[1]The OECD defines innovation in the Oslo Manual as « the implementation of a new or significantly improved product (good or service) or process (production), a new marketing method, or a new organizational method in business practices, workplace organization, or external relations. »