Political risk can be defined as all political and/or geopolitical events that could lead to a deterioration in a country’s economic and financial situation. For a long time, political risk was observed almost exclusively in emerging countries. In recent years, however, it has also been scrutinized in developed countries, with several notable cases: the debt crisis in the eurozone with the risk of Grexit, the 2016 presidential elections in the United States, the management of the refugee crisis since the Syrian conflict, etc. 2017 is unlikely to be spared from rising political risk, particularly in Europe, where since the June 2016 referendum that led to the Brexit victory in the United Kingdom, populism and political tensions have tended to increase before and during election periods.

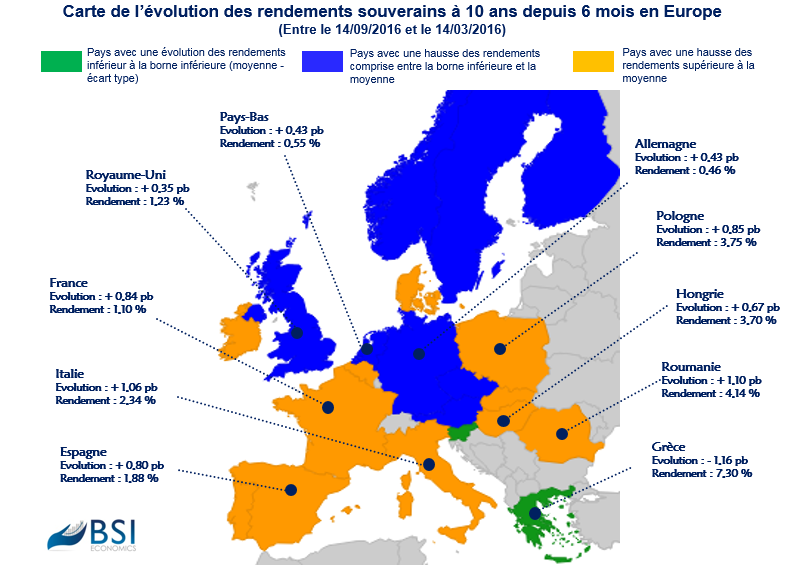

While it is difficult to quantify political risk within a country, variations in sovereign yields tend to capture, at least partially, this type of risk. For example, in the case of the 2017 presidential elections in France, uncertainties related to the rise of extremist parties and the absence of a clear favorite are causing concern among investors. This concern is reflected in higher sovereign yields, i.e., the level of interest rates that investors demand to purchase French debt securities. A marked increase in a country’s sovereign yields relative to its neighbors in recent months can therefore be seen as a consequence of increased political risk in that country. This would be particularly true in the eurozone, where the ECB’s quantitative easing (QE) policy is supposed to maintain downward pressure on these yields, thereby limiting their rise.

While France is a perfect example of this trend, with the upcoming presidential elections (April 23 and May 7, 2017) illustrating a rise in political risk accompanied by an increase in sovereign yields, other countries are also affected: Italy, Poland, Spain and Romania, even though they will not necessarily be facing important elections on their territory in the coming months.

V.L