The Tunisian economy post-revolution: ambition in the face of challenges (1/2)

Economic review

Summary:

· Since the Tunisian youth revolution in 2011, Tunisia has been taking steps toward democratic, economic, and social transition.

· In 2016, the economic situation fell short of expectations. Slower growth, widening twin deficits (public and current), persistent unemployment and inequality, declining investment, etc. All these factors reflect the scale of the challenges ahead.

· The « Tunisia 2020 » international investment conference, the adoption of a new investment code, the recovery of tourism, and the « dignity contract » to promote graduate employment are all efforts to enable Tunisia to return to growth.

· Tunisia still faces challenges in ensuring economic recovery and social peace, particularly through public finance reforms, improving the business climate, and measures to reduce inequality and unemployment.

Six years after the revolution, Tunisia is still making headlines. With agreements on investment, the recovery of tourism, and the increase in the public deficit, the Tunisian economy is oscillating between challenges to be overcome and potential to be exploited. Even if Tunisia’s current economic and financial situation is characterized by vulnerability, this nascent democracy is nevertheless showing positive signs that will enable it to embark on the path to growth.

A delicate economic situation

1- Growth, inflation, and unemployment

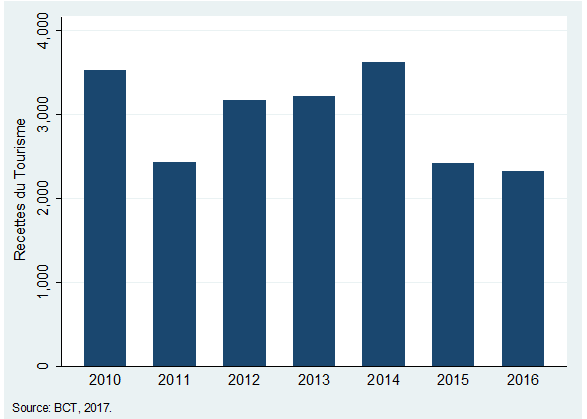

Since the outbreak of the revolution, economic growth has continued to decline (see Figure 1). At the beginning of 2016, economic growth forecasts were optimistic (around 2.5% according to the World Bank). At the end of the year, a downward revision was recorded. Economic growth in 2016 is expected to be limited to 1.5% (according to the IMF). This is partly due to a decline in the agricultural sector and a drop in the added value of non-manufacturing industries, particularly in the hydrocarbon and mining sectors (by 3% and 3.3% respectively). The decline in tourism activity may also be a cause of modest growth in 2016. Security instability and the series of attacks that struck the country in 2015 resulted in a 33% drop in tourism revenues between 2014 and 2015 and a further 4% drop in 2016 (Figure 2).

Figure 1 – Economic Growth and Inflation 2005-2016

Figure 2 – Evolution of tourism revenues in Tunisia 2010-2016 (in billions of Tunisian dinars)

The decline in investment may also explain the poor performance in terms of economic growth. Since 2011, instability and the security and economic climate have been sources of reluctance for investors. While investments accounted for more than 23% of GDP in 2011, they accounted for only 21.9% in 2015 and 21.7% in 2016.

As for inflation, the upward trend observed since the revolution began to decline gradually in 2014 (Figure 1). However, inflation rebounded at the end of 2016. According to the Central Bank of Tunisia (BCT), inflation is expected to reach 4.6% and 5% in 2017. Rising consumer prices are holding back household consumption, which is negatively affecting growth. Household purchasing power is also being affected by the depreciation of the Tunisian dinar, which is increasing the cost of imports.

The issue of unemployment remains particularly sensitive for post-revolution Tunisia. After peaking in 2011 (18.3% according to the World Bank), the unemployment rate fell slightly and stabilized at around 15.5% in 2016. According to the Tunisian National Institute of Statistics, unemployment affects women more than men, and particularly hits higher education graduates, with a rate of around 30% in 2016. These statistics illustrate the challenges facing the Tunisian government in terms of employment and highlight the need to reform the education system, in particular by adapting curricula to the requirements of the labor market (closer ties with businesses, support for the private sector to encourage employment, etc.).

The poverty rate[1] in Tunisia fell from 20.5% in 2010 to 15.2% in 2015. However, poverty affects non-urban areas more, particularly the interior regions, the cradle of the revolution, with a poverty rate of 26% in 2015 according to the INS. This finding reflects the inequalities that persist between different regions of Tunisia. The Gini coefficient was 36.1% in 2013 compared to 35.8% in 2010, illustrating the persistence of inequalities.

2- Widening twin deficits

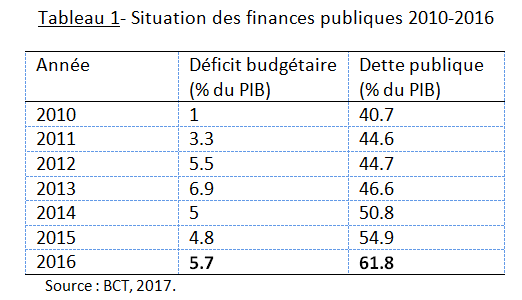

Public finance situation – With regard to public finances, the budget deficit continues to widen (Table 1). According to the BCT, the public deficit has been increasing steadily since 2010. The years 2014 and 2015 saw a decline in this deficit (to around 5% of GDP). However, the deficit is expected to rebound in 2016 to reach 5.7% of GDP.

The widening budget deficit is linked to lower tax revenues, partly due to lower investment, and the need to finance operating expenses, particularly the public sector wage bill, which accounts for around 14% of GDP and is in the order of 13 billion dinars, out of a total budget of 32 billion dinars.Public spending, which is mainly on infrastructure and capital goods, meets operating needs that are difficult to reduce, which explains the widening deficit that is driving up public debt.

Public debt continues to grow. It rose from 40% in 2010 to over 60% of GDP in 2016. This debt is particularly reflected in loans granted by international organizations, notably the IMF, on favorable terms (long maturities and low interest rates). Although considered sustainable by the IMF, this debt, which is generally denominated in foreign currencies, remains a burden that needs to be controlled, especially in Tunisia’s current context, characterized by a decline in the value of the dinar, which increases the cost of debt (exposure to unfavorable exchange rate risk).

At the end of 2016, the Tunisian government adopted a one-off economic contribution of 7.5% on corporate profits as part of the 2017 finance law—a further sign of economic distress. This is effectively a temporary tax for 2017, intended to boost the state budget. French and German companies operating in Tunisia have expressed their concerns following the imposition of this tax.

International trade: The current account deficit is widening. The current account deficit continues to widen, indicating that foreign exchange expenditures exceed revenues. The share of exports of goods and services in GDP has declined in recent years, reaching 40.8% of GDP in 2015.

However, exports of goods have been increasing steadily since 2010. In 2016, they reached 29,145.6 million dinars (nearly US$13 billion), an increase of 5.5% compared to 2015. This increase in exports is linked to the performance of olive oil, an improvement in the energy balance, and a recovery in manufacturing exports. Exports of services are also on the rise (up 5% between 2015 and 2016). Tourism revenues have remained modest since 2015, following the various attacks that have hit the country.

As for imports, government figures show an increase of 5.3% between 2015 and 2016. This increase is particularly noticeable in imports of consumer goods and foodstuffs. This category of goods also reflects the fragility of the economic situation in Tunisia. In this regard, discussions are underway concerning imports of consumer goods from Turkey and their impact on the competitiveness of Tunisian goods.

In terms of trading partners, Europe remains the main partner, accounting for 76.4% of total Tunisian exports and 68% of Tunisian imports in 2015. The proximity of the European market is considered an asset for Tunisia (Coface, 2017). Thus, with the return of more positive prospects for growth (and therefore demand) in Europe, Tunisia could benefit from an increase in exports to Europe.

What are the positive signs for the future?

1- « Tunisia 2020 » investment conference

Aware of the need for action to ensure economic transition, the Tunisian government announced a five-year development plan for 2016-2020 in 2016 with the aim of accelerating the pace of growth. Various structural reforms are planned, particularly in relation to the fight against corruption, improving the business climate, and social inclusion. As part of this plan, the Tunisia 2020 international investment conference, held in Tunis at the end of November 2016, was organized with the aim of promoting the country’s attractiveness in terms of foreign direct investment (FDI). The conference ended with €13 billion in investment pledges and financial aid from international organizations, European countries, and other Gulf countries. However, the implementation of these announced projects remains dependent on structural reforms and the quality of the business climate in Tunisia.

2- Tourism: Recovery in 2017?

The last few months of 2016 saw a return of tourism, albeit still very modest. According to the latest statistics published by the Ministry of Tourism, nearly 4.8 million tourists visited Tunisia by the end of October 2016, an increase of 3.4% compared to the same period in 2015. The gradual return of tourists is partly due to the gradual and partial lifting of restrictions or bans on travel to Tunisia imposed by foreign ministries. According to the BCT, however, tourism revenues fell by 3.8% compared to 2015 and by 36% compared to 2014, reflecting the fragility of the sector after the 2015 attacks.

However, these statistics do not dampen the government’s optimism for the 2017 tourist season. Seven million tourists are expected in Tunisia in 2017. To achieve this, several promotional events are planned in Tunisia in 2017, including the organization of the 23rd session of the M.I.T. « Marché International du Tourisme » tourism fair scheduled for April 2017. Particular attention is being paid to the Russian and Algerian markets. The recovery of tourism activity will bring in foreign currency, which is necessary to reduce the current account deficit, create jobs, and improve consumption, which will lead to an economic recovery.

Recommendations for a successful transition

In view of the various factors describing the country’s economic situation, a number of recommendations can be made with a view to putting Tunisia on a path to economic growth and social peace. To this end, the IMF has formulated a set of necessary structural reforms that are conditional on the disbursement of the second tranche of financial aid provided for under the Extended Credit Facility program ($2.9 billion over 48 months) granted in May 2016. These reforms include restructuring public finances and public institutions (notably the public banks Société Tunisienne de Banque STB, Banque Nationale BN, and Banque de l’Habitat BH), adapting the social security system, and strengthening the financial and banking sector.

There is also a need for greater visibility and transparency on the part of the government regarding the actions to be taken, particularly structural reform plans, in the medium term.

With regard to the private sector, the adoption of the new investment code, which is scheduled to come into force in April 2017, would be a key incentive for attracting foreign capital, particularly through tax advantages and the simplification of procedures for repatriating profits for foreign investors. This investment code will be an asset in bringing to fruition the projects agreed upon at the « Tunisia 2020 » international conference.

However, the success of these measures to attract investors and create sustainable economic activity depends on the quality of the business environment in Tunisia. In this regard, the anti-corruption program, the new investment code, and the reform of the financial sector will enable Tunisia to improve the quality of its business environment and thus enhance its international competitiveness. Indeed, Tunisia currently ranks only95th out of 138 countries according to the Global Competitiveness Report 2016.

In order to promote social peace, it is essential to make efforts to reduce the inequalities that persist between regions. This could be achieved through a better distribution of wealth and public investment projects, decentralization, and, above all, control of the informal economy( and informal sector employment) through better monitoring and enforcement of laws in cases of non-compliance.

Finally, it should be remembered that reducing inequalities and controlling inflation are key challenges in attracting foreign investors: by reducing social tensions, the democratic process could continue, which would encourage the inflow of FDI.

Conclusion

Tunisia, which has been engaged in a democratic process since the 2011 revolution, is oscillating between a difficult economic situation and a desire to achieve a sustainable democratic, economic, and social transition.

However, successive governments since 2011 have continued to make efforts to put Tunisia on the path to sustainable growth. Measures are multiplying, even if improvements are still modest.

Tunisia still faces challenges, particularly in terms of reducing unemployment and inequality, reforming the public sector, and reviving the economy. International organizations’ forecasts for 2017 remain optimistic. There is an international awareness that, despite the challenges, Tunisia will manage to move forward on the path to growth, supported by aid from international organizations and its proximity to the European market.

Bibliography

– Central Bank of Tunisia (BCT), 2017, https://www.bct.gov.tn/

– Global Democracy Rankings Report, 2017, http://democracyranking.org/wordpress/

– IMF (2016),“Tunisia: Fiscal Transparency Evaluation,” IMF Country Report No. 16/339.- IMF (2016),“Corruption: Costs and Mitigating Strategies,” Staff Discussion Note No. 16/05.

– Tunisian National Institute of Statistics INS (2017), www.ins.nat.tn/

– World Bank Group (2016),“Doing Business Economy Profile 2017: Tunisia”, World Bank, Washington, DC. © World Bank. https://openknowledge.worldbank.org/handle/10986/25654 License: CC BY 3.0 IGO.

[1] Considering the overall (not extreme) poverty threshold at the national level, which was around 1,206 Tunisian dinars per capita per year in 2010 and 1,706 dinars in 2015, according to an INS survey.

[2] The distribution of wealth in the country also shows inequalities. According to the latest World Bank statistics, approximately 43% of income is held by the richest 20% of the population.

[3] All other things being equal.

[4] This report provides a global competitiveness indicator based on the assessment of 12 pillars: institutional quality, infrastructure, macroeconomic environment, higher education, goods market efficiency, labor market efficiency, financial market development, technological flexibility, market size, business environment quality, and innovation.

[5] Whose weight has increased since 2011 from 15% to 50% of GDP.

[6] As confirmed by Christine Lagarde, Managing Director of the IMF, on the sidelines of the Davos Economic Forum held in January 2017.