Summary :

· Systemic financial tensions persist within the eurozone, exacerbated by the favorable environment created by falling nominal and real interest rates.

· Despite its positive effects, the low interest rate environment is potentially conducive to the emergence of several risks weighing on the banking and financial markets: bank profitability, insurance sector solvency, investors’ yield-seeking strategies, and the risk of normalization in the event of a rise in interest rates;

· For banks, insurance companies, and markets alike, a steepening of the yield curve could largely result in a major risk of a correction in risk premiums on bond markets, a sharp repricing of financial assets, a risk of intermediaries exiting market segments invested in by yield-seeking investors, and an impact on foreign exchange and real estate markets.

On February 21, 2017, the President of the Federal Reserve Bank of San Francisco highlighted the persistence of low interest rates and their role in the current environment, which is favorable to the financial sector but increases risks to financial stability ( » in a world of persistently very low interest rates, risks to financial stability may be greater than before « ). In 2016, in a quarterly exercise, the European Securities and Markets Authority assessed the low interest rate environment as a significant source of risk.

There are currently many risks to financial stability (sluggish growth, political uncertainty, uncertainty surrounding the finalization of the Basel III agreements, risk of financial deregulation (BSI article on the risks associated with deregulation)), but the extremely low interest rate environment is of considerable importance in that it constitutes an environment potentially conducive to the rise of several risks that this note aims to analyze. However, the stability of the financial system and the confidence it inspires are pure public goods, as defined by Charles Kindleberger (1986)[1]. Proof that institutions attach great importance to this is that in March 2016, in its motion for a resolution on the role of the European Union in international financial, monetary and regulatory institutions and bodies, the European Parliament stated: « whereas the stability of the financial system, which is a prerequisite for the efficient allocation of resources for growth and employment, is a global public good. »

To what extent do very low interest rates weigh on financial stability? What are the associated risks?

1. A look back at the causes of low interest rates

The 2007-2008 financial crisis highlighted significant shortcomings in the monitoring of systemic risk: its highly composite nature made it difficult to arrive at a simple definition of systemic risk that could be translated into a single indicator. In 2012, the European Central Bank developed a composite indicator of systemic stress,which aggregates stress indicators for the bond, money, stock, foreign exchange, and financial intermediary markets. It reflects systemic financial stress within the euro area while indicating the presence of simultaneous stress in various markets. However, the following chart highlights its increasing rise and increased volatility in the recent period (2013-2017).

Figure 1. Composite indicator of systemic stress in the euro area

Source: ECB, CISS – Composite indicator of systemic stress

The favorable environment generated by the decline in nominal and real interest rates is the result of a structural phenomenon that has been ongoing since the 1990s, and particularly since the 2008 crisis, which is being felt on a global scale. In order to anchor nominal interest rates at low levels, central banks have intervened extensively to support the interbank market and supply the real economy with liquidity. They have therefore lowered their interest rates and implemented a variety of monetary easing measures (cuts in the main refinancing rate and the deposit facility rate; LTRO and TLTRO operations; asset purchase program). This combination of interventions is likely to continue, given the ECB’s willingness to pursue this course of action, even as demand for safe assets increases.

Furthermore, beyond the effects of less conventional monetary policies, the theory of secular stagnation points to other factors that may explain the current low real interest rates: slowing productivity gains, demographic upheavals (increased life expectancy, decline in the working population), rising inequality, etc. (On the subject of secular stagnation, see this article by BSI Economics).

2. What risks does the low interest rate environment pose to financial stability?

Low interest rates have mixed effects on the financial system, and the banking system in particular. A low interest rate environment has some positive effects: it helps to reduce the refinancing costs of banks and the financing costs of economic agents, thereby improving access to credit for households and businesses and helping to increase borrowers’ ability to meet their commitments. In addition, a low interest rate environment improves asset quality and reduces the cost of risk, giving businesses more room formaneuver by easing their financing costs.

Chart 2. Composite cost of debt financing for banks

Nevertheless, a low interest rate environment also has negative effects on the stability of the financial sector. First, it is important to highlight the scissor effect between the supply of safe assets( particularly due to the downgrading of peripheral countries’ sovereign debt) and the demand for safe assets (which has increased significantly in recent years due to prudential regulations[3] and the regulation of OTC derivatives markets), accentuated by the ECB’s quantitative easing policy, as highlighted by the French Financial Markets Authority in a November 2016 report. The use of the repo market, which has a positive effect on the availability of high-quality collateral in the market, also poses significant risks to financial stability (leverage, interconnectedness, procyclicality, and market risks) that are worth mentioning.

Six risks weighing on the banking and financial markets can be identified:

1. A risk to banks’ profitability andtherefore to the profitability of their maturity transformation activity, via the deterioration of the net interest margin (return on loans on the asset side – cost of refinancing liabilities adjusted for the cost of risk).

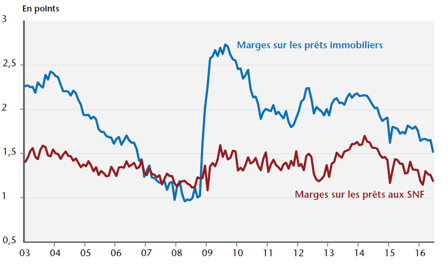

According to the 2016 annual report of the High Council for Financial Stability, the net intermediation margin[5] of major French banks (but also in Europe and the United States) has been on a downward trend since the 1990s: after peaking during the crisis in 2008-2009, it has fallen by 0.2 points since 2011.

Figure 3. Net interest margin on real estate loans to households and loans to non-financial corporations in the euro area

Source: OFCE, review no. 148 (2016)

However, this risk is not immediate and depends largely on the structure of banks’ balance sheets and the speed at which monetary policy is transmitted to lending rates. In this sense, and under the effect of competition within the banking industry and with the bond market, institutions have thus passed on changes in rates to the rates on loans to non-financial agents.

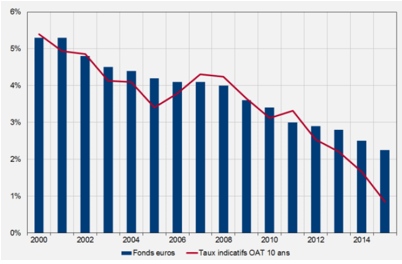

2. A significant risk in the insurance sector, particularly in the life insurance sector.

The combination of duration mismatches between assets and liabilities and rate guarantees offered to customers poses a risk to insurers’ solvency due to declining returns on their asset portfolios.

Chart 4. Average returns on life insurance for euro-denominated funds and French sovereign securities (2000-2015)

Source: 2016 annual report of the HCSF

In this regard, the EIOPA (European Insurance and Occupational Pensions Authority) has conducted stress tests which show that a significant number of European life insurers would see their solvency deteriorate in the event of a sharp rise in interest rates and inflation.The adjustment of contract remuneration, particularly on euro funds, would in fact be insufficient given the financial and macroeconomic circumstances, especially in view of the declining return on underlying assets.

Nevertheless, in its 2015 and 2016 annual reports, the High Council for Financial Stability (HCSF) emphasized that the French market remained relatively less exposed due to stricter regulations (recently reinforced by the Solvency II directive and the Sapin 2 law, which gives the HCSF the possibility of implementing preventive and corrective macroprudential measures atacross the insurance sector) and a relatively low proportion of life insurers offering guarantees above current OAT rates within the total outstanding amount (BSI Economics article oneuro funds of life insurance companies).

3. A risk to investors’search for yield strategy.

In order to meet their performance objectives, investors are seeking higher returns, changing their investment strategies and revising the risk/return trade-off in their portfolios (even though the economic and geopolitical context would suggest greater risk aversion).

In the asset management sector, the growth in assets under management (the French sector accounts for 14% of assets under management in the eurozone) is partly due to the rise of passive management[6] but also to the search for yield, through the management of assets characterized by their illiquidity premium, their issuance by non-eurozone issuers with a higher risk profile, or the extension of their maturity[7]. We are also seeing investors reusing securities on the securities lending market[8] in a quest for yield: lending financial securities has become a source of cheap financing for investment and hedging strategies, thereby maximizing portfolio returns.

We can also note the enthusiasm observed by the HCSF for thehigh-yield bond market[9], which has led to a sharp compression of risk premiums. What risks does this search for higher returns pose to financial stability? The risk of mispricing (a disconnect between the valuation of securities and their fundamentals)[10], but also a decline in investor vigilance (attraction to risky products, less scrutiny of product complexity, etc.).

4. A risk on money markets, which reached negative territory in 2015 and 2016.

The lack of attractiveness of money market funds[11] has forced them to significantly change their investment allocations by incorporating more risk (increased duration, credit risk). Money market funds have less room for maneuver in terms of reducing their exposure to interest rate risk compared to other funds (bond and diversified funds). Money market fund managers have therefore implemented measures (reduction of management fees, fund mergers) that threaten the sustainability of this market segment, as highlighted in the 2015 annual report of the HCSF, and pose increased risks to subscribers.

5. A risk of normalization in the event of a rise in interest rates.

Rates could rise as a result of several factors: (i) a significant return to actual and/or potential growth; (ii) a return to less accommodative monetary policies (notably via an end to the ECB’s QE program); (iii) a resurgence of inflation, which has already occurred (according to the OECD, it is estimated at 1.2% in France in 2017); or (iv) a reversal of fiscal policies.

However, a lasting change in the situation remains unlikely in Europe at present: on March 9, the European Central Bank announced that it would leave its rates unchanged (key rate at 0%, deposit rate at -0.40% and marginal lending facility rate at 0.25%) and would continue its asset purchase program at the same pace (at a rate of €60 billion per month starting in April, as announced in December 2016), given that « the ECB cannot say that it has achieved its goal, » according to Mario Draghi. Nevertheless, several changes are currently taking place in the United States: Donald Trump’s election as President of the United States has resulted in a faster rise in long-term interest rates (growth and inflation expectations due to his proactive program of tax cuts and infrastructure spending); two interbank rate hikes (currently in a range between 0.50% and 0.75%) are expected in March and May 2017 following the December 2016 increase. The dollar has continued to appreciate against the euro since the November 2016 election and expectations of a rate hike by the Federal Reserve, and a decline in the US sovereign bond market.

6. A steepening of the yield curve

For banks, insurance companies, and markets alike, a steepening of the yield curve could result in a major risk of a correction in risk premiums on bond markets, a sharp repricing of financial assets, a risk of intermediaries exiting market segments invested in the search for yield, and an impact on foreign exchange and real estate markets.

In particular, since a steepening of the yield curve correspondsto a situation of rising long-term interest rates, it occurs when investors demand higher risk premiums due to expectations of future inflation or a deterioration in the fiscal situation. J.R. Hicks’s theory of expectations of the term structure of interest rates (1939) explains that when bonds have long maturities, investors (characterized by their risk aversion and preference for liquidity) require higher returns (via higher risk premiums) in order to hold less liquid securities.

Conclusion

The IMF has sounded the alarm about the accumulation of medium-term risks to financial stability, including a persistent slowdown in global growth, the continuation of a low interest rate environment, and longer delays in the normalization of monetary policy. It is therefore necessary to consider a range of « more vigorous and coordinated » measures, going well beyond monetary initiatives, which would mitigate any scenario of financial and economic stagnation and ultimately prevent an increase in the aforementioned risks to financial stability.

Bibliography

– « Fed’s Williams sees more financial stability risk with low rates, » Reuters, February 21, 2017. Available at this link.

– Kindleberger Ch. P. (1986): The International Economic Order. Essays on Financial Crisis and International Public Goods, Berkeley, University of California Press.

– Borio C., and A. Zabai, 2016, « Unconventional monetary policies: a reappraisal, » BIS Working Paper, No. 570

– European Parliament motion for a resolution of March 17, 2016 on the role of the Union in international financial, monetary and regulatory institutions and bodies (2015/2060(INI)). Available at this link.

– Economic Analysis Council, « Very low interest rates: symptoms and opportunities, » note No. 36, December 2016

– Report by the French Financial Markets Authority, November 2016: « The reuse of assets: regulatory and economic issues. » Available at this link

– 2016 report by the High Council for Financial Stability. Available at this link

– Banque de France report on the assessment of risks to the financial system, December 2016. Available at this link.

[1] All economic agents benefit from financial stability, and the benefit of the financial system by one agent does not prevent other agents from also benefiting (non-rivalry criterion); and public authorities cannot exclude from its benefits agents who refuse to pay the price (non-exclusion criterion). Furthermore, the costs of financial instability to the community are not properly internalized by individual financial actors, thereby justifying public intervention. In addition to these two criteria (highlighted by Paul Samuelson in 1954), C. Kindleberger also emphasized the international and intergenerational dimensions as inherent to the concept of global public goods.

[2] The IMF (2012) uses four criteria to qualify an asset as safe, or « risk-free »: (i) low market and credit risk; (ii) high liquidity; (iii) limited inflation risk; and (iv) limited currency risk. Dang, Gorton, and Holmström (2010) consider risk-free assets to be insensitive to information: thus, when they are used as collateral in a financial transaction, investors assume that they are safe and therefore there is no need to seek information on the quality of their issuer. This risk-free nature is often determined in the markets by the ratings assigned by rating agencies.

[3] In this regard, it is worth noting the Basel III liquidity ratios (in particular, by 2018, compliance with the LCR liquidity ratio, which requires banks to hold sufficient stocks of high-quality, fully liquid assets to cover liquidity needs in a 30-day stress scenario) as well as the implementation of Solvency II regulations in the insurance sector (which, in particular, makes capital charges conditional on the credit quality of the asset portfolio and therefore encourages insurance companies to replace assets that are costly in terms of capital with safe assets that consume little capital).

[4] The repo market (or » repurchase agreement « ) is a secure source of refinancing within the money market: it is a contract whereby two parties agree to exchange, in full ownership subject to a commitment to retransfer, cash for financial securities, commodities or guaranteed rights relating to the ownership of securities or commodities, at a price determined in advance.

[5] The net intermediation margin is the banks’ income from their lending activity (the net balance between the difference in rates between deposits collected and loans granted).

[6] Passive management is linked to the performance of a market index, unlike active management, where an investment fund uses a fund manager to buy and sell financial securities with the aim of outperforming the market. The share allocated to indexing by management companies has increased steadily over the past 15 years, particularly through the development of exchange-traded funds.

[7] These vulnerabilities are addressed by the Financial Stability Board and the International Organization of Securities Commissions in their work on asset management vulnerabilities.

[8] Securities lending and borrowing is a form of securities reuse involving a variety of players, including both insurance companies and investment funds: a lender grants a temporary loan of securities, accompanied by a transfer of ownership of the securities lent to a borrower, who in return pays interest and provides collateral in the form of cash or securities. The borrower then returns the securities and the associated collateral to the lender.

[9] High-yield bonds are corporate bonds that present a higher risk of default (low credit rating, below BBB-) than investment-grade bonds and offer a higher coupon in return. They are therefore highly speculative.

[10] Hyman Minsky (1982) theorized this with his financial instability hypothesis, whereby the current and future decisions of economic agents are inherently unpredictable.

[11] Money market funds are known to be relatively accessible short-term investment tools. They are mainly composed of money market securities with very short maturities (less than one year), such as Treasury bills and short-term bonds. Short-term money market funds are inherently less risky and therefore less profitable. Their interest rates are indexed to the EONIA and 3-month Euribor (BSI Economics: « What are the similarities and differences between the EONIA and Euribor indices? »)and their yields are therefore declining.