Summary:

-Russian state banks have virtually no access to the capital markets of the European Union and the United States since the tightening of Western sanctions (July 31 and September 12, respectively) against Russia in the context of the Russian-Ukrainian crisis.

-This has resulted in capital outflows, putting pressure on the ruble and foreign exchange reserves, with the adoption of a floating exchange rate regime as a direct consequence, and a relative shortage of euros/dollars in the Russian banking system.

– These sanctions raise the question of the risk of a liquidity crisis, as it has become difficult to refinance Russian bank debt in euros/dollars. A liquidity crisis occurs when a bank does not have enough liquid assets to meet its commitments to its creditors.

– The liquidity of banks’ balance sheets and the central bank’s foreign exchange reserves reduce the risk of a short-term liquidity crisis. In the medium term, the liquidity of state-owned banks could be put to the test if Russian companies choose to repay their foreign currency debts using their bank deposits.

By highlighting Russia’s support for pro-Russian insurgents in eastern Ukraine, the crash of flight MH-17 in mid-July 2014 triggered tougher economic sanctions against Russia by the EU and the US.

Since mid-September, Russian state-owned banks have been virtually unable to obtain financing on the EU and US capital markets. With state-owned banks accounting for 60% of the Russian banking system (Sberbank alone accounts for 30%), these sanctions are a heavy blow to the Russian economy.

Do these sanctions pose a risk of a liquidity crisis for Russia’s major state-owned banks?

1 – The immediate impact of sanctions against Russian state-owned banks

The immediate impact of the sanctions against Russian state-owned banks is threefold: difficulty in obtaining financing in euros/dollars, depreciation of the ruble, and pressure on foreign exchange reserves.

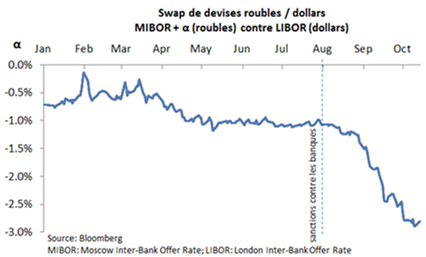

Since mid-September, Russian state banks (Sberbank, VTB, Gazprombank, Vnesheconombank, and Russian Agricultural Bank) have been virtually unable to obtain financing (loans and securities issues with maturities of more than one month) on the EU and US capital markets. However, they can still enter into currency swaps (which are not subject to sanctions), enabling them to convert ruble loans into dollar loans. On July 30, 2014, one day before the sanctions were announced, in order to exchange ruble flows for dollar flows, a Russian bank paid the US Libor interest rate (to the currency swap provider) and received the Mibor rate on average.[1]minus 1% (the alpha in the chart below) . On October 20, the ratio was US Libor versus Mibor minus 3%. This increase in the cost of currency swaps reflects the emergence of a relative shortage of dollars in the Russian banking system.

This series of sanctions is putting direct pressure on the exchange rate. Entities under sanctions—state-owned banks, but also certain companies in the energy (Rosneft, Lukoil, Gazprom Neft) and arms (Rostec) sectors—must now sell rubles on the foreign exchange market to obtain the foreign currency needed to repay their foreign currency debts. This reduced access to foreign capital markets, combined with the fall in oil prices, explains the sharp depreciation of the ruble since June (-25% against the dollar).

In order to contain the depreciation of the ruble, the Russian central bank has recently had to step up its interventions on the currency market. These amounted to USD 30 billion in October alone, representing 7% of its foreign exchange reserves at the end of October. As these interventions were no longer considered sustainable (rapid reduction in foreign exchange reserves) or effective (ruble depreciation anchored in expectations), the Russian central bank shifted its monetary policy by adopting a floating exchange rate regime, notably to preserve foreign exchange reserves.

The immediate impact of the sanctions is therefore that Russian state banks are finding it difficult to obtain financing in euros/dollars (either directly or indirectly via currency swaps) and that the ruble and foreign exchange reserves are under pressure, as evidenced by the recent shift in monetary policy towards a floating exchange rate regime.

2 – In the short term, the risk of a banking liquidity crisis seems remote

Why are these sanctions likely to trigger a liquidity crisis?

A liquidity crisis occurs when a company does not have enough liquid assets[2]to meet its commitments to creditors. However, holding liquid assets is not a given for a bank. First, because the fundamental role of a bank is to grant loans, and a loan is not a liquid asset[3]. Secondly, because holding illiquid assets, such as loans, is generally more profitable than holding liquid assets, such as cash. Thus, to meet a debt that is coming due, a bank can either decide to use its liquid assets or decide to refinance.

However, in the case of sanctioned banks, refinancing euro/dollar-denominated debt has become very difficult because the capital markets in the European Union and the United States are virtually closed and the rate on currency swaps has skyrocketed (see chart). Their ability to repay their euro/dollar-denominated debt therefore depends mainly on their liquid assets. Analysts estimate that liquid foreign currency assets cover on average one year of foreign currency debt servicing, assuming that foreign currency deposits remain stable. The problem of repaying foreign currency debt would arise fairly quickly if the Russian central bank did not hold substantial foreign exchange reserves. However, its substantial foreign exchange reserves enable it to intervene in the foreign exchange market to ensure its liquidity and thus enable banks to obtain large amounts of dollars in exchange for rubles. These reserves (excluding gold stocks), which stood at USD 430 billion at the end of October 2014, appear comfortable compared with the foreign currency debt of state-owned banks, which is in the region of USD 100 billion.

The liquidity of Russian state-owned banks’ balance sheets and the foreign currency reserves of the Russian central bank therefore significantly reduce the risk of a short-term liquidity crisis.

3 – In the medium term, the liquidity of Russian state banks could be tested by a withdrawal of deposits by Russian companies

Russian companies hold more than half of Russian bank deposits (55%), so their financial decisions could have a significant impact on the financial situation of state-owned banks.

The risk for state-owned banks is that companies will draw on their bank deposits (i.e., their cash reserves) to repay their external debt. The external debt of Russian companies represents 60% of Russia’s external debt and is twice that of the banking system. A company may be forced to take such a decision if it does not have or no longer has sufficient access to foreign capital markets (as is already the case for Rosneft, Lukoil, Gazprom Neft, and Rostec in the EU and the US) or if the refinancing of this debt is at excessively high rates (due to a shortage of dollars in the Russian banking system, for example). The scale of the decline in Russian corporate debt issuance in the first half of the year (-70%) suggests that refinancing their external debt will not necessarily be easy.

For example, Russia’s largest oil company, Rosneft, recently asked the Russian sovereign wealth fund for help in refinancing its debt, but this was refused on the grounds that Rosneft has sufficient cash to meet its commitments to its creditors for a certain period of time. Rosneft may therefore be forced to gradually draw on its bank deposits to repay foreign currency debts that it cannot refinance. However, Rosneft’s foreign currency deposits are colossal: they amount to $5 billion, or nearly one-third of the « highly liquid » assets of Gazprombank, the country’s third-largest bank.

In the medium term, the liquidity of state-owned banks could therefore be put to the test if Russian companies start withdrawing their deposits on a large scale.

Conclusion

The specter of a Russian banking crisis triggered by a liquidity crisis seems remote in the short term, given the liquidity of the banks’ balance sheets, the size of the Russian central bank’s foreign currency reserves, and the latter’s determination to provide foreign currency liquidity to the banks.[4]. In the medium term, the liquidity of state-owned banks could be put to the test if Russian companies chose to repay their foreign currency debts using their bank deposits.

While a liquidity crisis seems unlikely in the short term, the liquidity of Russia’s major banks is nevertheless under pressure. What impact will this have on corporate and household financing? In this geopolitical context of sanctions, the stakes appear to be high, as only 16% of Russians currently report feeling the effects.

Notes:

[1] The Mibor is the average rate at which a sample of around 30 Russian banks lend (without collateral). It is calculated daily by the Russian central bank for given maturities (short, several months).

[2] That is, cash or assets that can be quickly exchanged for cash, such as well-rated government bonds.

[3] For a bank to sell a loan, it must have a price, but this does not exist automatically. Determining the sale price of a loan portfolio requires work (audit, valuation, search for a buyer) that is the subject of certain consulting professions.

[4] Implementation of foreign currency repurchase agreements with banks in early November.

References:

-Facts: Moscow Times, Financial Times, Bloomberg, Reuters

-Figures: Fitch Ratings, Standard and Poor’s, Bloomberg

-European Union press releases

-Press releases from the Central Bank of Russia

-Opinion polls by the Levada Center

-Rosneft’s 2013 annual accounts