Summary:

· Universal basic income has been receiving increasing media coverage in recent months and now appears to be a possible measure in France in the not-too-distant future.

· Universal basic income can be a tool for combating poverty, which has increased in recent years in France and in the main European economies;

· However, it would be illusory to see it as a sufficient response to rising inequality and, more broadly, to the difficulties faced by developed economies in providing employment and an adequate standard of living for the entire population. ;

· With regard to its financing, the conditions for its implementation can take very different forms, which makes it difficult to quantify.

In France and abroad, universal income is increasingly present in public debate. In 2016, a popular initiative referendum was held in Switzerland on the creation of a basic income, resulting in the rejection of this measure by a large majority (77% voted against). Since January, an experiment has been underway in Finland: 2,000 people will receive an unconditional income of €560 for two years. In France, media coverage of this measure increased during the primary elections of the right and center, then during the primary elections of the left, whose winner wishes to introduce it (gradually) if elected President of the Republic.

This article looks at the issues surrounding universal basic income, which is praised by some of its supporters as having many virtues, but is considered too expensive and an incentive for laziness by its detractors.

1. What is universal basic income?

According to the Basic Income Earth Network (BIEN), universal basic income has five characteristics:

– It is periodic, not a one-off subsidy;

– It is provided in monetary form, which guarantees the beneficiary’s freedom of choice in how it is used;

– It is individualized;

– It is universal, with no means testing;

– It is unconditional and does not depend, in particular, on the recipient seeking work.

Behind these general features, which form the common ground shared by proponents of universal income, there are, however, many differences.

The main difference is the ideology underlying the need to create a universal income, which, as we shall see, directly determines how it is implemented. Its introduction is supported by a very diverse group of intellectuals, economists, and policymakers. For some, universal income responds to the desire for greater income socialization. For others, it rewards the use and appropriation of a common heritage and resources (oil, natural resources, past inventions, etc.).

Others see universal income solely as a safety net that removes individuals’ uncertainties about meeting their basic needs (housing, food, etc.). It would thus be the shortest route to eradicating poverty and social exclusion.

2. A tool for reducing poverty, not inequality

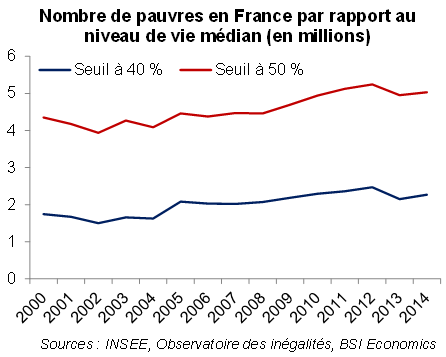

Over the past ten years, the economic crisis and rising unemployment have led to an increase in poverty. In France, 5 million people had a standard of living below 50% of the median standard of living in 2014( compared to 4.4 million in 2008). Even aside from the rise in unemployment, which deprives low-income households of the income from work on which they are particularly dependent, poverty is a phenomenon that France has never been able to eliminate. More than 2 million people live below the threshold of 40% of the median standard of living, despite the various social benefits that exist.

The introduction of a universal basic income appears to be a simple solution to poverty. In Capitalism and Freedom ( 1962), this is the main motivation of Milton Friedman, who defends this measure in a chapter devoted to the fight against poverty. John Kenneth Galbraith also wrote in Time Travel in Economics ( 1995) that « there is no more obvious solution to poverty than income. » Universal basic income has the merit of directly addressing poverty without tackling its many complex causes by increasing the incomes of the most disadvantaged. However, an acceptable standard of living threshold (50% of the median standard of living, for example) still needs to be defined, which will determine the terms of application (amounts and financing in particular).

In concrete terms, universal income can take the form of a negative tax. This is the case, for example, in the proposal by Gaspard Koenig and Marc de Basquiat in a 2014 report: LIBER, un revenu de liberté pour tous(LIBER, an income of freedom for all). According to their simulations, LIBER, financed by a proportional tax, would result in a net financial gain for the first deciles (in terms of income), which would gradually decrease, and a net loss for the last two deciles.

In terms of reducing inequality, the potential effects of universal income seem more limited, as it is a tool for redistribution but does not address primary income inequality. In Capital in the 21st Century, Thomas Piketty highlighted that income inequality from labor, except for the tiny top bracket he calls « super-executives » compared to the rest of the population, was much lower than inequality in capital endowments. To reverse the trend toward capital concentration and income inequality, a high universal basic income financed by higher capital taxation would need to be considered. Given the high mobility of capital and the already high level of capital taxation in France, there is limited room for maneuver. Coordination between states would be more appropriate, but seems unlikely in the near future. Reducing inequality requires more profound economic changes that go far beyond the issues surrounding universal income.

3. A response to the scarcity of jobs?

The universal income envisioned by Milton Friedman aims to eradicate poverty. It ensures that no member of society falls into poverty and exclusion, without undermining the functioning of the market economy and private property. By acting as a safety net, universal income can be useful in terms of financial security, at a time when career paths are becoming less and less linear.

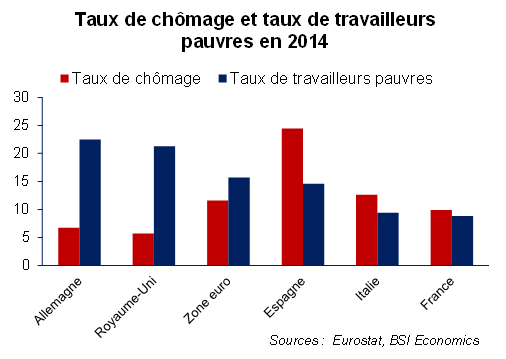

It is therefore conceivable that the creation of a universal income would have an impact on the labor market by affecting the supply of labor. A financial safety net could indeed affect both the reservation wage[3] of employees and their bargaining power. Depending on the type of universal income introduced and the amount provided, this effect could be greater or lesser. In recent years, labor market reforms in most European countries have been guided by the constraints of price competitiveness adjustments and have weighed on job quality, wages, household incomes, and productivity. In the United Kingdom and Germany, where the number of unemployed has fallen from its 2007 level, the share of atypical jobs[4] has increased, and the level of poverty is high, particularly among those in employment (see graph).

Faced with the rise in the number of low-wage workers or those on atypical contracts, as well as the number of unemployed (more than 6 million people in France across all categories), the role of universal income as a protection against poverty and precariousness may appear to be potentially important. Its introduction would be a powerful counterweight to the deterioration in employment and income conditions for the most vulnerable workers. In reality, labor market regulations and the existence of minimum wages already fulfill this role. The need to protect workers from poverty and precariousness reveals more shortcomings in the functioning of the labor market than it is a solution. In France, the proportion of working poor is lower than the European average. Even if progress is possible, work remains an effective protection against poverty in France compared to other European countries, but the unemployment rate is high.

For some of its advocates, universal income is also a response to the scarcity of work. As a result of a sustained slowdown in economic growth, the number of unemployed people has risen significantly in Europe over the past ten years. In France and the eurozone, the unemployment rate stands at 10% of the working population. From a macroeconomic perspective, this would amount to using universal income as an adaptation to, rather than a solution for, underemployment. Universal income would thus be a new form of work sharing, transforming unemployment into total or partial paid inactivity. This raises the question of whether other forms of work sharing might not lead to more inclusive growth and greater social progress.

There are many causes of underemployment, and they do not necessarily require increased income socialization. On the supply side, it can result from insufficient labor productivity, which can be resolved by lowering labor costs or increasing workers’ skills; on the demand side, it can result from a lack of opportunities, which limits employment. Part of the unemployment in France and more broadly in Europe is cyclical in nature and stems from weak demand. There is also a strong labor productivity constraint weighing on low wages. The government’s policy of boosting job growth by lowering labor costs is a response to this challenge. France’s economic policy does not focus on reducing labor costs through wages (but through a reduction in social security contributions), a policy that would make low-productivity jobs profitable, reduce unemployment, but generate working poor.

Universal income does not address the growing inability of most developed economies to create jobs and productivity gains without undermining the determinants of aggregate demand. While it may, depending on how it is implemented, mitigate the consequences to a greater or lesser extent, it is not a sufficient response to underemployment in France (and Europe).

As for the incentive to work, if its definition is limited to the exercise of a job, it is better preserved when labor regulations protect working conditions and wages. In the same way that the minimum hourly wage protects against poverty, it preserves the incentive to work, particularly for full-time employees, because it guarantees a minimum income per hour worked. The decline in the participation rate, transforming part of unemployment into inactivity, should therefore remain limited if universal income is introduced. To preserve this incentive to work, it is essential that the protection offered by universal income as a safety net does not open the door to a downward leveling of income protection and working conditions for those in employment.

For these same reasons, namely that work offers a higher level of income than universal income, the latter is not a tool for stabilizing demand. At the bottom of the cycle, job losses, rising unemployment, and their effects on wage income call for the implementation of a countercyclical policy to support demand, which universal income cannot replace. More structurally, universal income can generate additional consumption insofar as it reduces inequalities and increases the income level of the poorest, who save little. However, we have seen above that the lasting reduction of inequalities, which are responsible for the rise in the savings rate and the sustained weakening of aggregate demand[5], requires more comprehensive changes.

4. Is universal income affordable?

In a recent note, Universal income: a useful utopia?, the French Economic Observatory (OFCE) estimated that the introduction of universal income would represent 22 points of GDP, which in practice makes this project unrealistic.

In the table below, we have simulated the gross cost of two « formulas » for universal income, one (UI 1) being significantly more generous than the other (UI 2). In both cases, the amounts involved are indeed considerable. Thus, for an amount of €250 per month for those under 18, €450 per month for those aged 18-65, and €550 per month for those over 65, the universal income would represent €340 billion (or 15 points of GDP, and €615 billion or 28 points of GDP in the more generous formula).

Although these amounts may seem prohibitive at first glance, they must be analyzed in net terms, which depend greatly on the rationale behind the introduction of a universal income. Nor do they take into account its potential impact on the economy (and tax revenues, employment, etc.).

One could imagine a self-financing redistributive tax system, with or without the principle of tax brackets. The « LIBER » mentioned above would, for example, be financed by a proportional tax. The higher an individual’s income, the lower their net financial gain, which is equal to the amount received as universal income minus tax. For individuals with the highest incomes, the tax would exceed the amount of universal income, making them net contributors.

Furthermore, we could also consider replacing social welfare benefits with universal income. The increase in public spending could be offset by the elimination of some social spending, leading to possible administrative simplifications. The overhaul of minimum social benefits, without necessarily eliminating all consideration of the specificities of individual situations, and the individualization of payments were mentioned in the Sirugue report[6] in 2016.

In France, social benefits amounted to €690 billion in 2014, or about one-third of GDP, according to the Directorate for Research, Studies, Evaluation, and Statistics (Drees). Of this expenditure, €240 billion was for health (particularly illness and disability) and is not intended to be redirected to universal income. The link between other social spending and universal income is not always clear for items such as Old Age and Survivors (€313 billion), Employment (€43 billion, particularly unemployment), Housing (€18 billion), and Family (€54 billion). For Poverty and Exclusion expenditure (€20 billion), substitutability is clearer.

The financing of universal income is an important issue for its credibility. It depends both on the amounts paid out under universal income, which may be more or less generous depending on the monetary poverty threshold used, and on the implementation of a more redistributive tax system and possible savings in social spending.

In a logic of increased socialization of income or remuneration of common wealth or natural resources, universal income opens the door to much greater intermediation by the state and public spending in the sharing of added value.

Conclusion

The introduction of a universal income would be a direct solution to poverty, which has been on the rise in France and in the main European economies in recent years. It potentially represents a simple and effective tool for responding to the consequences of the inability of developed economies to guarantee employment and a minimum standard of living for their populations.

As a financial safety net, it could be a response to the rise in financial insecurity, amplified by the increase in unemployment and the development of atypical contracts, but it will not solve the structural causes. Universal income does not eliminate the need to address the economic imbalances that currently characterize developed economies: structural weakening of aggregate demand, slowing productivity, rising inequality, inadequate training systems, etc.

It can be financed by making trade-offs with existing social benefits and public policies or by accepting increased intermediation by public administrations in the distribution of income, by increasing income taxation and strengthening the redistributive nature of the tax system. In any case, this makes it an extremely politically and economically impactful choice.

[2] Primary income is a household’s income before redistribution.

[3]The reservation wage is the wage below which an unemployed person will not accept a job.

[4] A typical job is a permanent full-time job.

[5] This topic has been the subject of numerous articles, including those by Lawrence Summers on secular stagnation, as well as a study by BSI Economics: » What are the risks of secular stagnation for the eurozone? »

[6] « Rethinking social minima: towards common basic coverage, » published in 2016.