News: The ECB may be tempted to reduce its monetary accommodation. However, isn’t it a little premature to start normalizing monetary policy?

– The risk of deflation has now been averted

For: Peter Praet, Chief Economist at the ECB, stated that » since the crisis, deflationary risks have caused serious concerns on several occasions in the euro area, but today we can say that they have disappeared. »

Inflation in the eurozone reached its lowest point in January 2015 at -0.6%, forcing the ECB to intervene to avoid deflation. It is now close to 1.4%, while core inflation remained stable at 0.9% after jumping to 1.2% in April.

Cons: But is this inflation sustainable? It is difficult to say, as the adjustment to 1.2% in the underlying figure has not materialized in the latest figures. Nevertheless, stronger wage inflation across the eurozone will certainly be necessary to stabilize overall inflation and make it self-sustaining (i.e., not dependent on QE, which currently contributes 0.4 percentage points to inflation) over the medium term. Since 2013, wage inflation has stagnated at around 1.6%[4].

According to the chart above, the ECB’s monetary policy appears to have been ineffective in stimulating core inflation. However, it has enabled the eurozone to avert the risk of a deflationary spiral[5] and thus justify its effectiveness in a context of weak growth and persistently low inflation.

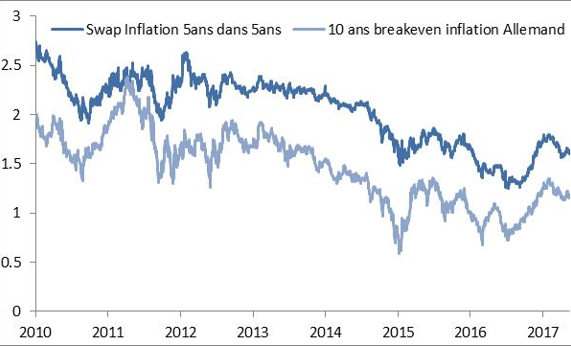

– Inflation expectations have rebounded since summer 2016

Pros: The ECB’s reaction function takes inflation expectations into account rather than the current level of inflation. Economic agents tend to postpone consumption if they anticipate a fall in prices, thereby reducing demand. This decline is exacerbated by self-fulfilling expectations (this postponement of spending leads to a fall in demand and therefore in prices, and so on).

Against: The ECB closely monitors the 5-year forward inflation rate, which is a true barometer of inflation expectations. At only 1.6%, the 5-year forward rate is close to its level prior to the announcement of QE[6].

– Stronger growth

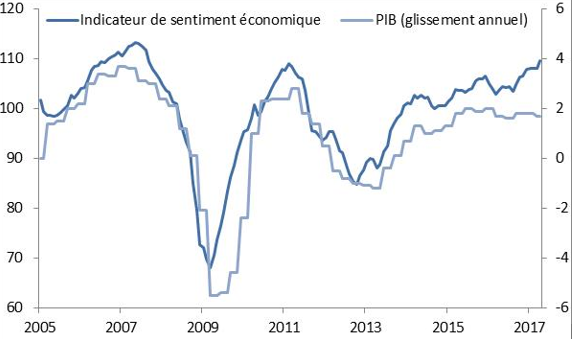

Pros: The eurozone’s overall activity index is at its highest since April 2011 for both services and manufacturing, with production, order books, and employment at their highest levels in six years. Consumer confidence, business climate, and investor optimism indices are improving. The eurozone confidence index is also at its highest level since September 2007.

Another key point is that the latest figures point to more consistent growth within the eurozone, with the economic cycles of member countries converging once again, as seen in Portugal (+1% quarterly growth in Q1) and Italy (+0.4% in Q1).

On the downside: According to the minutes of its April 27 meeting, the ECB believes that economic growth is increasingly solid but that a number of risks still weigh on the recovery. It cites in particular the uncertainty surrounding the Trump administration’s policies, the economic impact of Brexit, and the slowdown in growth in China and other emerging economies. Although reduced following the Dutch and French elections, domestic risk has not been completely eliminated. Italy is once again a cause for concern, with a fragile economy (low growth, very high debt stock) and persistent political instability.

– Continuing QE in 2018 would be technically difficult

Pros: The current technical constraints on QE could eventually force the ECB to halt its debt purchase program. Asset purchases are made based on the eurozone members’ share of the ECB’s capital. The central bank also imposes a purchase limit on each security of 33% of the total size of the issue. According to the latest figures published, the ECB would find it difficult to meet its purchase targets (based on the capital allocation key of the member states), particularly for German and Portuguese debt.

Cons: Even if the options remain limited, the ECB could initially raise the purchase limit on each security from 33% to 50%.Alternatively, the ECB could opt to reduce QE gradually, leaving itself some leeway (i.e., extending QE until the end of 2018 by reducing purchases to €30 billion for six months, then to €10 billion).

Conclusion

It is therefore difficult to imagine an announcement of QE tapering as early as June, given that « we have not yet reached a stage where inflation dynamics can be self-sustaining without the support of monetary policy[1] » and that the various criteria set out above on inflation are still not being met. The ECB is likely to limit itself to raising its growth forecasts for the eurozone while revising its inflation estimates downwards. However, some investors still believe that a change in monetary policy in September remains a possibility.

[1]April 2017 data, year-on-year.

[2]Core inflation: Inflation excluding the most volatile components such as commodities.

[3]April 2017 data, year-on-year.

[4]Q4 2016 data, year-on-year.

[5]A difficult situation to overcome, as illustrated by the case of Japan.

[6]January 22, 2015

[7]Mario Draghi, April 6, 2017