Summary:

– Life annuity sales still have negative connotations today

– However, this type of sale can provide a more comfortable retirement and help finance long-term care

– As proof of interest in this product, several French investors, including Caisse des Dépôts, plan to create a life annuity investment fund worth €100 million[1]

– The recent growth of the reverse mortgage market in the United States suggests that greater development of life annuities is possible in France

Life annuities? When you hear the term, you probably think of Pierre Tchernia’s film or the fact that Jeanne Calment herself sold her home on a life annuity basis to her notary, who, unfortunately for him, passed away before her. Add to this cultural heritage the fact that life annuities are contracts linked to death—a subject with negative connotations, to say the least—and that they are sometimes associated with a desire to disinherit one’s children, and you have many reasons for the often negative connotations associated with this product. Moreover, the debate on the « morality » of life annuities is not new. They existed inthe Old Law that prevailed until the Revolution, and the question of whether to maintain them under the Civil Code gave rise to heated debate.

So why is there renewed interest in life annuities today? Why, for example, have several institutional investors recently decided to create a €100 million investment fund dedicated to life annuities? This article will attempt to answer these questions and draw parallels between life annuities and their American « equivalent, » the reverse mortgage.

What is a life annuity in France?

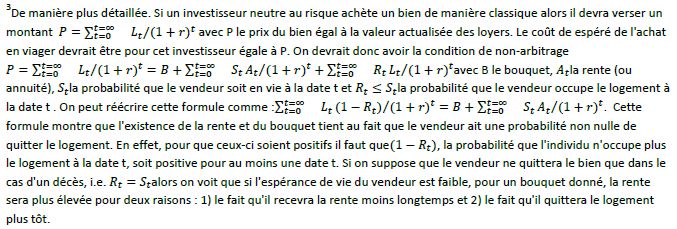

A life annuity sales contract is a contract for the sale of real estate. In the case of a seller of a life annuity property who wishes to continue living in it[2], the seller retains a right of occupancy and, upon their death, the buyer will be free to dispose of the property. The payment made by the buyer to obtain the property consists of two parts: a lump sum and an annuity. The lump sum is a sum paid at the time of sale and the annuity is a sum that the buyer must pay to the seller until the latter’s death. Ultimately, the sales contract should satisfy the equation (with VA for Present Value):

Price of the Property = Lump Sum + DV(Annuity) + DV(Rent)

As the seller retains the right to remain in their home, the buyer will not be able to rent out the property, over which they haveabusus. This is why the present value of the rent that the buyer will not be able to collect is included in the equation.[3].

For a given annuity, the present value of the annuity will be higher if the seller’s life expectancy is high. This is because if the seller has a longer life expectancy, they are likely to receive the annuity for a longer period of time, which increases the cost of the annuity payments for the buyer. Similarly, the higher the annuity, the lower the lump sum will be.

In the case of life annuities, the controversial element is the annuity[4]. Some see it as a « bet on death » since it is in the buyer’s interest for the seller to die early so that they do not have to pay them the annuity. This is the whole logic of Pierre Tchernia’s film. As we will see later, one of the advantages of creating life annuity investment funds is probably to reduce this idea of a « bet on death. »

What is the purpose of a life annuity? Three explanations.

Is a life annuity so uncommon? Actually, no. A life annuity is, by definition, an annuity paid until the death of the beneficiary. However, most retirees today finance their retirement through a life annuity: their retirement pension. A life annuity is a special type of insurance where the beneficiary is insured against the risk of living a long life. Before the introduction of public pension systems, people were either uninsured against the risk of longevity or could insure themselves in other ways: selling their property on a life annuity basis, purchasing a life annuity in exchange for capital (which was similar to a tontine), or through their family (with younger members supporting older members).

This brings us back to the benefits of selling a life annuity. For a significant proportion of households in France and many other countries, real estate represents a significant part, or even the majority, of their assets.[5]. Since many people want to remain in their homes, they tend not to sell them. However, one way to remain in one’s home while benefiting from additional income is to sell on a life annuity basis. This is one of the reasons why, historically, people selling on a life annuity basis have often been widows: people with low retirement pensions but sometimes significant real estate assets.

One might wonder whether the potential benefits of selling on a life annuity basis are lower today than they were in the past, given the widespread availability of retirement pensions. A fairly simple way to assess this is to look at the difference between the amount of retirement pensions and the cost of dependency, i.e., the cost associated with the loss of independence in old age. In 2009, the cost of home care was around €1,800 per month and €2,300 in an institution. At the same time, half of French people received a retirement pension of less than €1,000 per month, with state assistance averaging €450.[6]. It is therefore clear that many retirees’ pensions are insufficient to cover their needs if they become dependent on care. Life annuity sales therefore seem potentially attractive to many retirees, offering the prospect of a more comfortable retirement[7.

Another advantage of life annuities is that they allow people to leave their assets to their potential heirs earlier, perhaps at a time when it is more useful to them. This is one of the functions of the lump sum option. Life annuities are therefore not necessarily at odds with the idea of wanting to leave part of one’s wealth to one’s children, for example.

Institutional players: what is the advantage for the development of life annuities?

Life annuity sales currently represent only a tiny fraction of total real estate transactions in France (just over 0.5% of the total). However, it is reasonable to assume that greater involvement by institutional players could help to increase the volume of the market and its share of total real estate transactions.

One advantage is that it reduces the idea of « betting on death. » The idea of entering into a contract with someone who has a strong interest in you not living too long is undoubtedly unpleasant and could even be considered immoral. It is easy to imagine that many people refuse to sell on a life annuity basis for this reason and consider it a last resort. A large fund that invests in life annuity purchases plays on the law of large numbers. The longevity of a single seller has a minimal impact on the fund’s return, so it is less likely that the institutional buyer will hope for the seller’s death, as might be the case for an individual buyer.

A second advantage is that the counterparty risk is undoubtedly lower. It is quite conceivable that the buyer of a life annuity may no longer be able to pay the annuity, exposing the seller to the risk of not receiving the annuity for which they initially signed the contract. It is likely that for a (well-managed) fund, the risk of being unable to pay the annuity is lower. Finally, it should be noted that individuals may be reluctant to purchase a life annuity because they are highly exposed to the risk that a person may live a long time (see the case of Jeanne Calment). For them, it is clear that investing in a life annuity is , a priori, very risky.

Another type of contract in the United States: the reverse mortgage

In the United States, there is another product that is quite similar to a life annuity: the reverse mortgage. The logic behind this type of product is the same as that of a life annuity: to convert real estate wealth into cash. In 2011, only 2.1% of households over the age of 65 had a reverse mortgage. However, this figure was less than 0.5% in 2005, reflecting strong market growth.

Unlike life annuities, these mortgages are most often in the form of a line of credit.[8]. However, it should be noted that people wishing to benefit from a reverse mortgage can also choose a life annuity or a fixed annuity for a certain period of time. It is also possible to combine these different options. This proves that it is undoubtedly possible to offer solutions that are more flexible than the traditional life annuity and that may be better suited to certain specific needs of retirees. It is reasonable to assume that increasing the opportunities for retirees to benefit from additional income linked to their real estate is beneficial. For example, a person may only wish to use their real estate if they have to pay significant healthcare expenses. In this case, they may prefer a line of credit solution to a traditional life annuity solution.

In any case, the recent development of the reverse mortgage market suggests potential growth for products that allow real estate to be used to finance retirement. In France, this could take the form of a development of the life annuity. It is particularly interesting to note that the greater interest in reverse mortgages in the United States comes at a time when most contracts (90%) are now administered by a federal agency.[9]. This shows that institutional players can undoubtedly play an important role in the development of this type of product. They can build trust in contracts that may appear complex. In the United States in particular, people wishing to take out a reverse mortgage must meet with an advisor from the U.S. Department of Housing and Urban Development (HUD) before they can commit, which undoubtedly helps to reassure interested parties who may be afraid of being « ripped off » by certain private players, as well as increasing their understanding of the products.

Two main limitations to the development of the life annuity market

There is undoubtedly one main limitation to life annuity sales: the property being sold. While it may be relatively easy to sell a life annuity and generate significant income in Paris or on the French Riviera[10], it can be more difficult to sell in a more remote rural area. This brings us back to one of the main problems associated with real estate: lack of diversification. Indeed, a person who owns a property that is the main component of their assets remains subject to the risk that, at the time of sale, the value of the property will be lower than expected.

There is also a risk for funds investing in life annuities: the systemic risk of falling real estate prices. Recent experience (in the United States, Spain, and Japan since 2007, for example)[11]shows that this type of risk should not be overlooked, highlighting the need to carefully consider the structure and financial viability of these investment funds.

Retirement financing is a complex issue linked essentially to two risks: longevity and dependency. The two variables are closely related. The longer people live, the greater the risk that they will one day face a situation of dependency. With the aging of the population, many questions arise about the ability of public financing systems to meet the needs of retirees. These needs can be very varied in nature: home adaptations, domestic help, medical assistance, etc. They broadly cover all the services that make up what has been called the silver economy. The latter is defined as the economy serving the elderly, and some see great potential in it in terms of job creation. The Directorate for Research, Studies, and Statistics (DARES) estimates, for example, that it could create 300,000 net jobs by 2020. Even if these figures are open to debate, it is certain that the aging of the French population, but also the global population[12], is likely to lead to growth in sectors linked to this silver economy.

However, a fundamental question remains: how will these services be financed? Will older people be able to afford them? Given that a significant portion of retirees’ wealth is tied up in real estate, life annuities are one way of enabling retirees to access the services offered by the silver economy and thus enjoy a more comfortable retirement. They also allow people to stay in their homes longer if they wish.

Conclusion

The development of life annuities or other reverse mortgage- type products can contribute to the growth in demand for services for the elderly, easing certain financial constraints that limit the services they can purchase. It can also help finance home modifications to adapt them to the needs of old age.

Given its importance in retirees’ assets, the use of real estate to finance retirement has a potentially major role to play in terms of demand for services for the elderly. Life annuities therefore offer a range of significant opportunities at both the individual and macroeconomic levels. Indeed, it is difficult to see how the silver economy could develop significantly without substantial demand, which could mean a bright future for this old product, the life annuity, which until recently seemed to be on its last legs.

References

– Makoto Nakajima & Irina A. Telyukova, » Reverse Mortgage Loans: A Quantitative Analysis , » 2013. Working Paper.

Févier Phillipe, Laurent Linnemer & Michael Visser » Testing for Asymmetric Information in the Viager Market , » 2012, Journal of Public Economics.