Usefulness: Home to nearly 10% of the world’s population and experiencing some of the most dynamic economic growth in the world, Southeast Asia remains particularly exposed and vulnerable to natural disasters intensified by climate change. This change is not without consequences for economic growth, with the Asian Development Bank estimating that it could reduce regional GDP by nearly 11% by the end of this decade[1].

Summary:

- Southeast Asia is vulnerable to flooding and drought;

- Greenhouse gas emissions resulting from growth in the region are contributing to climate change (rising temperatures), which in turn is increasing the frequency of natural disasters;

- Floods and droughts are among the main natural disasters facing the region and particularly affect production and supply chains.

Jakarta, the capital of Indonesia with a population of nearly 10.7 million (five times the population of a city like Paris), began 2020 with flooding caused by heavy monsoon rains, the most severe the country has ever experienced. Faced with a growing risk of rising water levels, the measures taken by the capital’s government to combat flooding have remained limited, with a budget allocated this year that is 26% lower than in 2018.

Southeast Asia has been one of the most dynamic regions over the past decade, but at the cost of greenhouse gas emissions that have grown at the same rate as economic growth during this period. These emissions have caused temperatures to rise by between 0.14 and 0.20 degrees per decade since the 1960s, exposing the region to more frequent natural disasters. These include floods, droughts, and rising sea levels, which threaten Jakarta and other capitals in the region, such as Ho Chi Minh City (Vietnam) and Bangkok (Thailand), by 2050, according to Climate Central, an independent scientific research center specializing in the impacts of climate change. This article attempts to identify the main causes of climate change in Southeast Asia and analyze what its consequences could be in the coming years.

Source: Asian Development Bank, World Bank, BSI Economics

Rapid growth accompanied by increased fossil fuel consumption due to deforestation

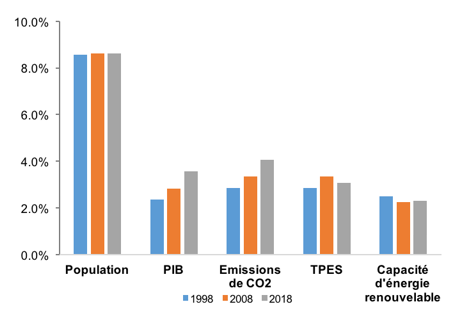

Share of key global economic and energy indicators in Southeast Asia, 2000-2018

Sources: World Bank, IEA, IRENA, BSI Economics

N.B.: TPES – total primary energy supply: the amount of primary energy (in millions of tons of oil equivalent) available to the country.

In recent years, Southeast Asia has experienced rapid and sustained economic growth, accompanied by a 5% increase in greenhouse gas emissions over the last two decades, a rate close to its growth level (4.7% according to the latest estimates from the Asian Development Bank). CO2 emissions[3] in the region account for nearly 4.1% of global emissions and are concentrated in Indonesia, which is home to nearly 264 million people and accounted for nearly 36% of regional emissions in 2017, followed by Thailand (18%), Malaysia (16%), and Vietnam (14%).

The main causes of CO2 emissions are deforestation and the use of fossil fuels, which have intensified in response to growing urbanization and rapid population growth. However, according to estimates by the Asian Development Bank, they could reduce regional economic growth by around 11% by 2100.

Deforestation: responding to urbanization and growing production at the expense of the environment

The tropical forest in Southeast Asia accounts for nearly 15% of the world’s forests but is facing a faster rate of deforestation than other tropical regions, mainly to meet the growth of its urban population (2% on average across the region) and agriculture. Indonesia has seen the most significant decline in forest cover in the region, ahead of Malaysia, Vietnam, Cambodia, and Thailand, with a loss of 13 percentage points (forests accounted for nearly 65% of the total land area in 1990 and 52% in 2011) in the space of twenty years in order to expand agricultural land by 5.2 percentage points (from 24.9% of the total area in 1990 to 30.1% in 2011). However, according to a study by the Asian Development Bank, this deforestation is not without consequences for CO2 emissions, as Indonesia’s swamp forests contain thousands of tons of carbon, forming carbon sinks[4].

Southeast Asia is heavily dependent on fossil fuels

The economies of Southeast Asia are still dependent on fossil fuels, which are the second largest source ofCO2 emissions after deforestation. Regional energy demand has increased by more than 80% since 2000, with fossil fuels predominating. Among these energy sources, oil is used for electricity generation and in the transport sector: it is expected to exceed 9 million barrels per day by 2040, compared to 6.5 million per day today, if no action is taken, according to the IEA’s « Southeast Asian Energy Outlook 2019 » report.

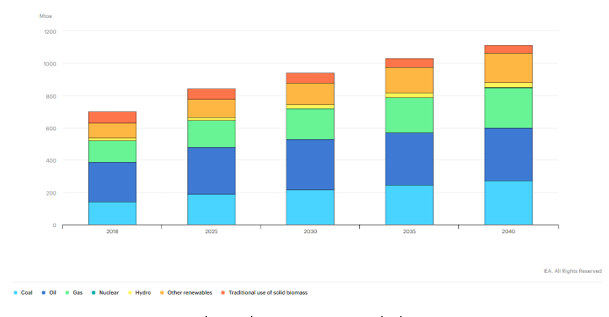

Energy demand in Southeast Asia according to IEA scenarios, 2018-2040

Source: The Southeast Asia Energy Outlook 2019, IEA

Nevertheless, Southeast Asia has significant potential to develop renewable energies, which currently meet only about 15% of the region’s energy demand. IEA estimates indicate that renewable energy could account for 30% of regional energy production by 2040. Although governments are becoming aware of the threat that climate change poses to their economies, renewable energy production remains far from reaching the current levels seen in China (26.7%) or India (35%).

This ambition remains partly dependent on international funding. This is the case, for example, in Indonesia, which has committed to reducing itsCO2 emissionsby 39.25% by 2030, which come mainly from coal and fossil fuels. However, green energy projects appear to be encountering financing difficulties, according to the Director of New Energy at the Indonesian Ministry of Energy and Mineral Resources. According to the ministry’s data, 30 out of 75 renewable electricity purchase agreements, with a total capacity of 1,581 megawatts, are currently awaiting financing.

Furthermore, the reality is that the region is not making sufficient use of its energy mix and, because its environmental standards are more lax, it is instead welcoming coal-fired power plant projects, thereby increasing its dependence on coal. In September 2019, Urgewald and its NGO partners updated the Global Coal Exit List, which is used by asset managers and institutional investors to divest from coal. According to this list, Vietnam (33,935 MW), Indonesia (29,416 MW), and the Philippines (12,014 MW) are home to the largest coal-fired power plants and continue to expand with the construction of new plants run by foreign companies seeking to avoid stricter environmental standards in their home countries. South Korea, for example, invested nearly $5 billion between 2013 and 2019 in coal projects, according to a Greenpeace report. However, these projects are often located in countries such as Indonesia and Vietnam, where standards for harmful pollutant emissions are more lax, allowing plants to emit up to 18.6 times more nitrogen oxide and 11.5 times more sulfur dioxide than those in South Korea.

Deforestation and the use of these polluting energy sources, which are the main causes of flooding, in turn affect export-led growth and production.

ASEAN is more vulnerable to flooding

Source: ASEAN Coordinating Center for Humanitarian Assistance on Disaster Management

The region is more exposed to flood risks, the economic consequences of which will be analyzed: only the main supply shocks have been selected. Given that Southeast Asian economies are mainly driven by exports and agriculture—while benefiting from shifts in the Chinese supply chain—rice production, business risks, and productivity have been selected for this analysis.

Supply chains increasingly disrupted

The region has benefited from shifts in the Chinese supply chain, reinforced more recently by the effects of the trade war. This has accelerated the process of relocation from China to the region in order to escape increased customs duties and benefit from low manufacturing costs. However, natural disasters are further disrupting the supply chain by interrupting production for varying lengths of time, and some companies are seeing their revenues decline.

The Japanese automotive industry and electrical component manufacturers, which had gradually established themselves in Thailand since the 1960s to benefit from low local labor costs and thus strengthen the price competitiveness of their exports, had not sufficiently integrated environmental risks. The 2011 floods in Thailand, which lasted nearly six months, highlighted the vulnerability of certain industries: they blocked the supply chain, affecting nearly 10,000 factories, from automotive components to semiconductors. According to the Tokyo Chamber of Commerce in 2017, nearly 80% of 1,000 Japanese companies have no flood contingency plans. Honda Motor, for example, was forced to suspend production at its factories in Thailand (state the year), which had a production capacity of 240,000 cars per year, or 5% of its total production. Toyota’s profits also plunged by 18.5% in the second quarter of 2011.

Agricultural production and exports: the case of rice

Although economies are beginning to diversify, agricultural production remains a major component of the region, with nearly 200 million hectares dedicated mainly to the production of rice, corn, and vegetable oil (palm oil), representing nearly 10.3% of GDP in 2018. However, changing climatic conditions resulting from rising temperatures are undermining agricultural production. On the one hand, rising temperatures can lead to the sterility of certain crops and reduced yields. On the other hand, seasonal variations in rainfall can lead to water shortages or flooding, causing a decline in agricultural production. Rice production in the region, which accounts for nearly 30% of global production and nearly 12% of regional GDP, is particularly vulnerable to these changes.

According to the latest ADB estimates (2015), rice yields are expected to decline by 50% relative to 1990 levels by 2100, affecting not only regional growth but also global rice prices. The most recent example is Thailand, the world’s second-largest rice exporter, which suffered from a severe drought in 2019, affecting the country’s economic growth . This is one of the reasons (along with the recent coronavirus outbreak and increased uncertainty due to the delay in voting on the 2020 budget) why the Bank of Thailand recently decided to cut its rate by 25 basis points to 1% in order to support growth.

Conclusion

The dependence of Southeast Asian economies on fossil fuels and deforestation are the main factors contributing to greenhouse gas emissions in the region. They are responsible for rising temperatures, causing extreme weather conditions, ranging from severe droughts to heavy rainfall leading to flooding. These effects of climate change particularly affect agricultural production and supply chains that have developed in the region, which are heavily dependent on fossil fuels.

ASEAN governments aim to increase the share of renewable energy to 23% of the region’s energy mix by 2025. However, currentCO2 emission reduction policies are not sufficient to achieve the levels envisaged by the 2015 Paris Agreement. Renewable energy projects in the region are facing financing difficulties and remain at levels that are still insufficient to meet the growing electricity demand of the region’s economies. On the other hand, the region is welcoming new coal projects from countries seeking to avoid stricter environmental standards, thereby accelerating the region’s dependence on fossil fuels instead of developing its energy mix.

Bibliography

Southeast Asia and the economics of global climate stabilization, ADB, 2015

Impacts of sea level rise on economic growth in developing Asia, ADB, 2017

Storm clouds loom for Asian companies unready for climate change, Nikkei Asian Review, 2018

Boiling Point, Amit Prakash, Finance & Development, IMF, 2018

Southeast Asia energy outlook 2019, IEA, 2019

Summary of the Asia-Pacific Disaster report 2019, UN Economic and Social Council, July 2019

Climate change 2014, Impacts, Adaptation, and vulnerability, IPCC

The Economics of climate change in Southeast Asia: a regional review, ADB, 2009

“Rising Seas Will Erase More Cities by 2050, New Research Shows”, New York Times, Oct 2019

https://www.nytimes.com/interactive/2019/10/29/climate/coastal-cities-underwater.html

Building Resilience in Businesses and Supply Chains in Asia, Asia Business Council, Feb 2018

“Mitigating supply chain disruption risks from natural disasters”, Bangkok Post, 2017

NGOs Release New Global Coal Exist List for Finance Industry, Urgewald, Sept 2019

https://urgewald.org/medien/ngos-release-new-global-coal-exit-list-finance-industry

A Deadly Double Standard, South Korea’s Financing of Highly Polluting Overseas Coal Plants Endangers Public Health, Greenpeace, Nov 2019

[1] https://www.imf.org/external/pubs/ft/fandd/2018/09/southeast-asia-climate-change-and-greenhouse-gas-emissions-prakash.htm

[2]SEA and the economics of global climate stabilization, ADB, 2015

[3]IEA statistics, 2017

[4] This is the mechanism that extracts CO2 from the atmosphere by storing it in another form. Generally, greenhouse gases are absorbed into ocean water, the subsoil, and flora. Forests and oceans are the main carbon sinks, capable of absorbing about half of greenhouse gas emissions. In the case of oceans, CO2 dissolves and is drawn into deep waters. As for forests, they release the CO2 they have absorbed into the atmosphere in the form of oxygen via photosynthesis. In this sense, deforestation would accelerate greenhouse gas emissions.

[5]https://www.thejakartapost.com/news/2019/02/07/indonesian-institutions-struggle-to-get-funding-for-green-energy-projects.html

[6] https://news.mongabay.com/2019/11/coal-south-korea-plants-pollution-export-financing/

[7] https://storage.googleapis.com/planet4-international-stateless/2019/11/ea2d3c1d-double_standard_report-high-resolution.pdf

[8] https://www.aseanstats.org/wp-content/uploads/2019/11/ASEAN_Key_Figures_2019.pdf