Usefulness of the article: This article explains the interaction between monetary and fiscal policy in the current context. It attempts to quantify the effects of fiscal stimulus on economic activity through econometric analysis and considers the possible sectoral impact of the stimulus plan on the economy.

Abstract :

- The announced European stimulus could add 2% to GDP per year in the eurozone over the next four years.

- Against a backdrop of low interest rates and depressed demand, monetary policy would be less effective in supporting a rapid recovery. Indeed, the central bank cannot further lower financing costs to stimulate economic recovery.

- Conversely, it is in this context that fiscal policy is most effective, as it can remove uncertainty by creating prospects for future activity.

- With more targeted spending in sectors less affected by the crisis, such as the digitalization of the economy, this recovery plan could also promote structural transformations already accelerated by the Covid-19 crisis.

As European countries face a second wave of the Covid-19 pandemic, questions arise about their economic outlook. The fiscal stimulus plans announced at European and national levels will be key to promoting economic recovery. Indeed, when interest rates are low and aggregate demand is depressed, fiscal policy becomes the most effective instrument for boosting consumption and investment.

Fiscal and monetary policies are complementary when interest rates are low and unemployment is high

In a context of low or negative interest rates – also known as the « zero lower bound » – monetary policy is already close to its limits. The Central Bank certainly has enough ammunition to ease financing conditions, but lowering financing costs below zero is not enough to stimulate the economy. Before the COVID-19 crisis, the European Central Bank (ECB) had repeatedly missed its inflation target of close to, but below, 2%. Mario Draghi and then Christine Lagarde were already encouraging governments with budget surpluses to implement fiscal stimulus measures before the COVID-19 crisis.

The limitations of monetary stimulus seem to become more pronounced during a recession. As John Maynard Keynes said, lowering interest rates to kick-start the economy in times of crisis is like « pushing on a string. » By lowering financing costs and facilitating access to credit—whether through lower refinancing rates for banks or on the markets via its asset purchase programs in the case of the ECB this year—the Central Bank is helping indebted companies to repay their debts more easily and thus survive during a period when their self-financing capacity is damaged. This is what we have seen this year. However, monetary policy cannot remove all uncertainty about the outlook for future demand. Conversely, fiscal stimulus, with its specific commitments, provides clarity to businesses in growth markets and gives households greater visibility on their incomes. For example, the investment plans in energy transformation, digitization, and infrastructure spending announced this year are promoting a recovery in investment, a rebound in confidence in economic activity and job prospects, and thus also in consumption. Furthermore, as the ECB shares the same recovery objective as the government, i.e., to revive the economy, it is reinforcing fiscal action by maintaining easy financing conditions for governments and private actors. There is therefore no crowding-out effect on private demand.

We quantify the « fiscal multiplier » in the euro area to assess the implications of these interactions between fiscal and monetary policy for the post-Covid economic recovery (see Methodology in the appendix). The aim is to assess how much one euro of fiscal stimulus can boost the economy in times of crisis and with low interest rates. To this end, using TVAR modeling, we are able to differentiate between four economic states: high unemployment and low unemployment, as well as high interest rates and low interest rates. We find that:

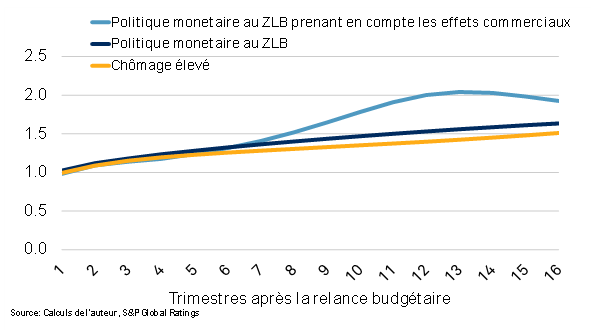

- Fiscal policy is more powerful when interest rates are low or negative (below 0.5%) and in times of crisis (unemployment above 10.1%). In such a context, €1 of fiscal stimulus can generate up to €2 of cumulative wealth after four years (see Figure 1). Taking into account foreign trade dynamics, the identified effect is highest, suggesting that in a crisis, fiscal stimulus leakage is limited.

Fiscal stimulus has a return of less than 1 over four years when monetary policy is not at the zero lower bound and the unemployment rate is below 10.1%. This is because the central bank will tend to raise its key interest rates to counter inflationary pressures.

Figure 1: €100 of fiscal stimulus today can generate up to €200 in two years

Our results reinforce the idea that fiscal stimulus has a greater impact when it is used for countercyclical adjustment and when monetary policy has reached the zero lower bound. It should also be noted that fiscal stimulus has a lower cost when it is more effective, since the central bank is not in a position to tighten rates. Governments can therefore finance themselves on the markets at relatively low rates. Furthermore, it is important to differentiate between contexts in order to identify the effect of fiscal stimulus. When no distinction is made, we find no significant effect of fiscal stimulus on the economy.

« EU Next Generation » could boost the economy by up to 10% after four years

Based on our estimates, the €750 billion European « Next Generation » fiscal stimulus plan, or 5.4% of EU GDP in 2019, could potentially boost the eurozone economy by around 7.6% after two years and up to 10% after four years.

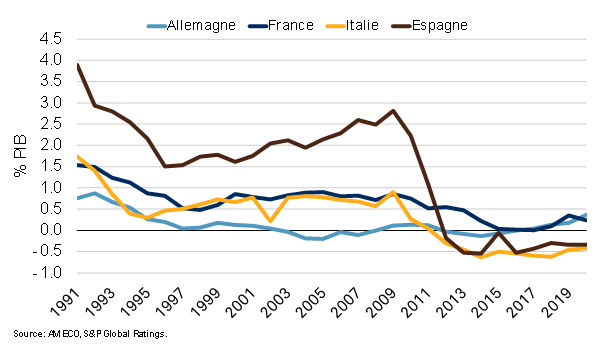

Beyond the size of the stimulus, its composition is also important for potential growth. At the European level, the emphasis is on long-term spending, with a minimum of 30% allocated to the ecological transition, and there is also a focus on digital development and structural reforms. These productive investments should boost long-term growth in the eurozone after ten years of low public investment (see Chart 2).

Chart 2: Public investment – net capital formation in the public sector

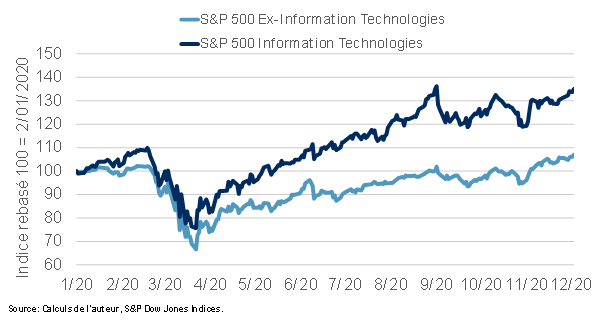

However, this recovery plan could promote certain structural changes accelerated by the COVID-19 crisis. For example, companies have increased the digitization of their activities following the expansion of teleworking and lockdowns. The information and communication sector has emerged stronger from the COVID-19 crisis (see Chart 3). Conversely, the tourism, catering, and hospitality sectors have been moreseverely affected by the crisis. Current recovery budgets seem to place more emphasis on digitization than on services such as catering or tourism. However, the skills of workers in these different sectors are not very similar. Thus, the apparent inequalities of this crisis could widen if these aspects are not taken into account by the recovery policy.

Figure 3: The Information and Technology sector emerges stronger from the crisis

Conclusion

Fiscal stimulus is the most effective tool for restarting the economy in a low interest rate environment and in the aftermath of a crisis. In the eurozone, the announced stimulus could add 2% to annual wealth over the next four years. The emphasis on productive investment could also improve the growth potential of European economies, although it may also further facilitate the structural changes accelerated by the lockdown.

APPENDIX – Methodology: Quantifying the fiscal multiplier in the eurozone

We choose a Threshold Vector Autoregressive (TVAR) model to differentiate the fiscal multiplier according to different states of the economy. Based on the literature on fiscal multipliers[1], this is the most relevant method for differentiating the effect of fiscal stimulus according to various states of the economy.

In the TVAR model, the transition from one economic state to another is identified by external threshold variables. We identify two types of economic states: a state of high or low unemployment and a state of low or high interest rates, which we define using the ECB’s « shadow » interest rate as defined by Wu-Xia. The threshold values are calculated before the TVAR model is estimated. The transition from a « low » to a « high » unemployment rate occurs at the 10.1% threshold, and the transition for the interest rate occurs at the 0.5% threshold.

We use aggregate quarterly data for the euro area from 2000 to 2019:

- Public expenditure is the sum of public consumption and public investment.

- Net taxes are the difference between expenditure and revenue.

- National accounting variables and the unemployment rate are from Eurostat, while the interest rate is from Wu-Xia.

- We transform the data into stationary variables by dividing the national accounts variables by potential GDP, which we estimate using a Hamilton filter, as our objective is not to examine the drivers of potential growth but simply to extract its trend.

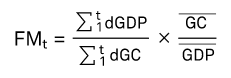

With regard to the model, we estimate the following TVAR: « public spending as a percentage of potential GDP, net taxes as a percentage of potential GDP, GDP as a percentage of potential GDP, » using the same order for the Cholesky identification scheme, which allows us to extract the response functions for the four states described above. We then use the response function for the public expenditure (dGC) and GDP (dGDP) variables to calculate the cumulative fiscal multiplier following a public expenditure shock. The multiplier takes the following form:

To verify the robustness of the result, we model variations in the model by adding the interest rate, inflation, and external dynamics (i.e., the visible trade balance). These estimates tend to reinforce our results. Taking external dynamics into account, we find an even higher fiscal multiplier when monetary policy is at the zero lower bound, reaching 2 after two years.

[1]Auerbach A. and Gorodnichenko Y. (2012): Measuring the Output Responses to Fiscal Policy, American Economic Journal: Economic Policy, Volume 4, No. 2, May 2012, pages 1-27

Blanchard O. and Perotti R. (2002): An Empirical Characterization of the Dynamic Effects of Changes in Government Spending and Taxes on Output, The Quarterly Journal of Economics, Volume 117, Issue 4, November 2002, pages 1,329-1,368

IMF (2019): The Euro-Area Government Spending Multiplier at the Effective Lower Bound, Working Paper No. 19/133.

Ramey V. and Zubairy S. (2018): Government Spending Multipliers in Good Times and in Bad: Evidence from US Historical Data, University of California, San Diego, and National Bureau of

Economic Research, Texas A&M University.

[1]See also: Tenreyro, Silvana, and Gregory Thwaites. 2016. « Pushing on a String: US Monetary Policy Is Less Powerful in Recessions. » American Economic Journal: Macroeconomics, 8 (4): 43-74.

[2]See, for example, the French 2021 draft finance bill: https://www.economie.gouv.fr/entreprises/projet-loi-finances-plf-plfss-2021-mesures or the EU recovery plan: https://ec.europa.eu/info/strategy/recovery-plan-europe_en#main-elements-of-the-agreement