During the debates held on January 22, 2018, at the National Assembly on the financing of productive investment in France, BSI Economics presented its contribution on the structure of household savings, average savings efforts, the effectiveness of the PEA-PME (small business equity savings plan), and the attractiveness of private equity and crowdfunding.

#1 Typology and structure of French household savings

The data is calculated from the financial accounts of financial agents, national accounts, and quarterly studies on household wealth conducted by the Banque de France.

· In mid-2017, total household wealth was divided between ~40% (~€4.9 trillion) in financial assets and ~60% in non-financial assets (real estate). Household financial assets are mainly concentrated in risk-free products (64% of investments) and liquid products (69% of investments: this figure includes euro-denominated life insurance funds considered liquid, most of which are not subject to any holding period restrictions other than tax incentives and can be quickly mobilized), including in particular:

– 21% in liquid banking products: 9% in demand accounts alone (more than €400 billion) and 12% in all savings accounts (regulated and unregulated).

– 33% in euro-denominated life insurance funds.

– 29% in productive investments: while equities account for a small proportion (5%), indirect investment via life insurance unit-linked products makes up the difference (6%). In addition, unlisted assets account for nearly 18% of household wealth.

– 17% in money market funds, notes, and other instruments.

· The breakdown of French households’ assets has remained relatively stable over the long term and is changing only slowly.

· Furthermore, financial assets are divided almost equally between bank balance sheet products (29%, of which 24% is in commercial banks and 5% in Livet A, LDD and LEP accounts centralized at the Caisse des Dépôts), euro funds (33%), and investments in businesses (30%: direct shares, life insurance units of account, debt securities, unlisted), banknotes, coins, and other items (8%).

#2 Average financial savings of French households

· The average financial savings effort of households is around €90 billion per year, with its breakdown being fairly sensitive to economic conditions and recently shifting strongly towards liquidity.

· Financial investment flows reached €92 billion in 2016 (compared with a five-year average of €91 billion), down from the pre-financial crisis period (when they peaked at around €120 billion).

· Unlike the stock (wealth), financial savings flows are sensitive to economic conditions (interest rates, confidence, unemployment, etc.) and regulatory changes (taxation of retirement savings, raising of the ceilings on Livret A and LDD savings accounts, etc.). There are fairly significant year-on-year variations in the distribution of these savings among the assets available to households.

· Recently, in a context of low rates of return, it has shown:

§ an increased preference for liquidity (71% of flows at the end of the second quarter of 2017), particularly through demand deposit accounts (€42 billion deposited over the last four quarters) due to a significant opportunity cost (low incentive to invest funds in investments considered to be unprofitable and a probable wait-and-see effect).

§ A moderate return to risky investments (nearly 30% of flows over the last four quarters, particularly due to subscriptions to unit-linked products and non-monetary UCITS).

#3 The PEA-PME: high complexity, lack of communication, and absence of digitalization

· Context: Created in 2014, the PEA-PME scheme aimed to channel the savings of French citizens, initially the wealthy and then the general public, towards the equity financing of SMEs and mid-cap companies. When the scheme was launched, asset management professionals wanted to develop the range of UCITS eligible for the PEA-PME, encouraged by the performance analysis of the SME equity market in France and Europe. However, this sentiment at the launch of the scheme was tempered by its complexity, which could hinder its widespread adoption and therefore its success.

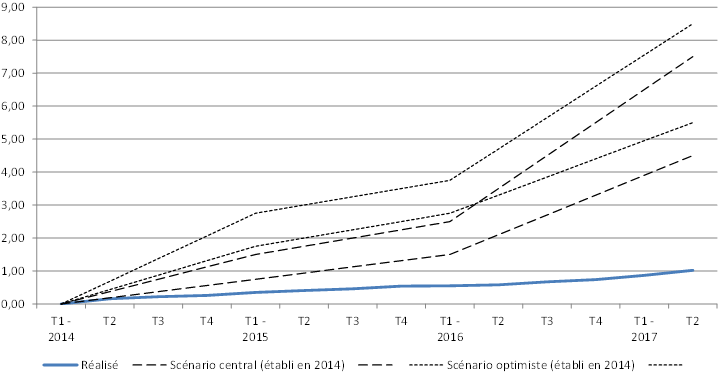

· Observation: These fears proved to be well-founded, and in 2018, the observation can only lead to a feeling of disappointment with the scheme across the board. The number of subscribers fell between 2016 and 2017, refocusing on the wealthiest clients. The outstanding amount of the PEA PME thus stood at €1 billion in mid-2017, far from the growth forecasts made in 2014 (see graph, « PEA-PME kick-off, Entrepreneurs’ Observation Report, March 18, 2014).

Chart: PEA-PME inflows and forecasts 204[1](in € billion)

Sources: Banque De France, PME Finance, BSI Economics

· BSI Economics’ point of view:

§ The complexity of the scheme, both in terms of defining eligible targets and the lack of clarity regarding its fiscal future, has hampered its widespread adoption. Less experienced asset managers lack the capacity to absorb uncertainties and have been too passive in making the solution available to savers.

§ The lack of communication and the continued virtual absence of digitalization have limited access to the scheme to the best-supported savers, and therefore the wealthiest, whose priority remains taxation.

#4 Private equity: a diversification tool for savers

· Context: Private equity has been experiencing dynamic growth since 2014. We have seen growth in the amounts raised by private equity funds from individuals and family offices (or private banks)[2], driven by the momentum of fundraising by tax funds in 2016 (local investment funds (FIP) / mutual funds for investment in innovation (FCPI)).

· Observation: This growth in amounts is also reflected in a significant increase in the number of subscribers in a market undergoing consolidation. Since 2012, we have seen a decline in the number of tax funds and a significant increase in the number of subscribers. Coupled with the stability of the average subscription amount (around €8,000 since 2012), this confirms the attractiveness and sustainability of the scheme.

· BSI Economics’ view: The scheme’s growth driver remains limited, as the development of these funds depends primarily on the ability to attract savers to products that are attractive from a tax perspective but risky, illiquid, and opaque.

§ The ability to attract savings from the general public depends above all on the ability to encourage financial intermediaries (insurance companies, banks, BPIfrance) to devote part of the French people’s abundant savings to more mature schemes such as FPCIs. Here again, the low level of digitization of private equity funds and the complexity of the business are a barrier to investment by the general public.

§ Redirecting savings held in savings accounts or life insurance requires a strong commitment to diversifying the assets financed by these instruments. In an environment of low returns on investment tools aimed at the general public, diversifying these portfolios could guarantee the attractiveness of these investments while allowing these funds to be allocated to the French productive fabric, particularly SMEs.

#5 Crowdfunding in France, a validated Proof of Concept (POC): clear regulations and widespread digitization

· Crowdfunding, and in particular the financing of companies via appropriate financing tools (shares, bonds, credit), has grown exponentially since 2011. In 2016, the crowdfunding market attracted €68.2 million in equity investments, €45 million in bonds, and €40.2 million in interest-bearing loans (source: 2016 crowdfunding barometer in France, FPF).

This growth in France has been facilitated by clear regulations since 2012, promoting the emergence of a thriving ecosystem. Accompanied by effective communication aimed at the general public, no fewer than 2.5 million people (47% of funders are over 50, 35% are between 35 and 49, and 18% are under 34 and are present throughout the country) have chosen to invest part of their savings in crowdfunding platforms.

Digitalization and communication are central to the success of this market. Market consolidation and the emergence of major crowdfunding players will enable further growth.